The latest REA Insights report shows that property buyer demand is surging, which is fueling the rapid price appreciation being experienced across Australia.

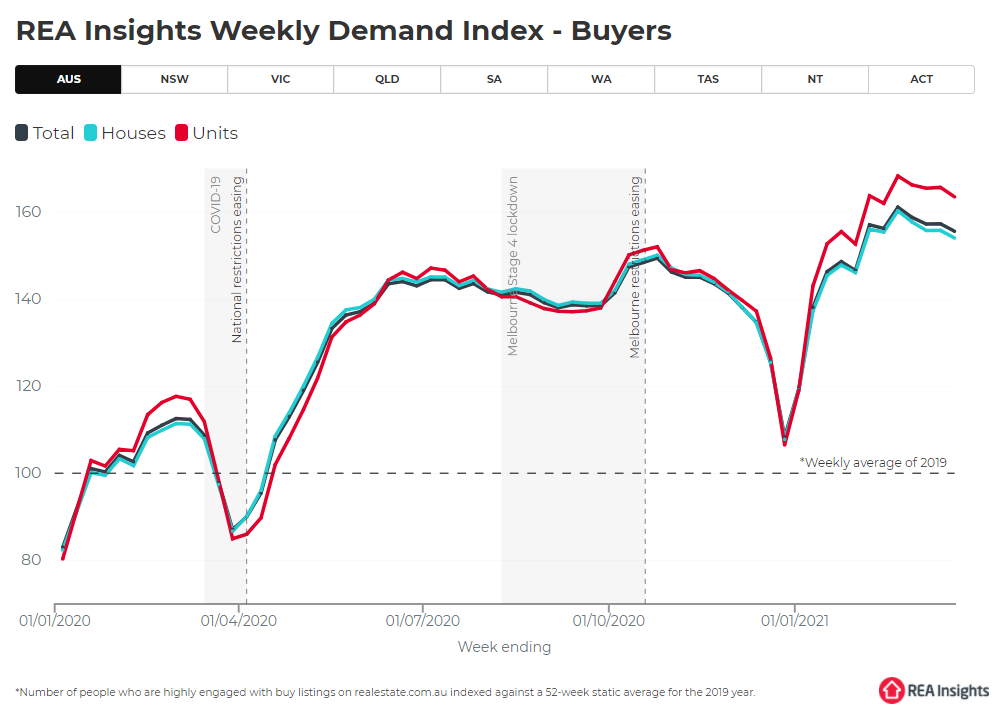

First, REA’s weekly demand index, which “measures the change in the number of people that are highly-engaged with properties listed for sale on realestate.com.au”, is running near historic high levels, up 58.6% relative to the same time a year ago:

REA’s weekly demand index is running way above the same time last year.

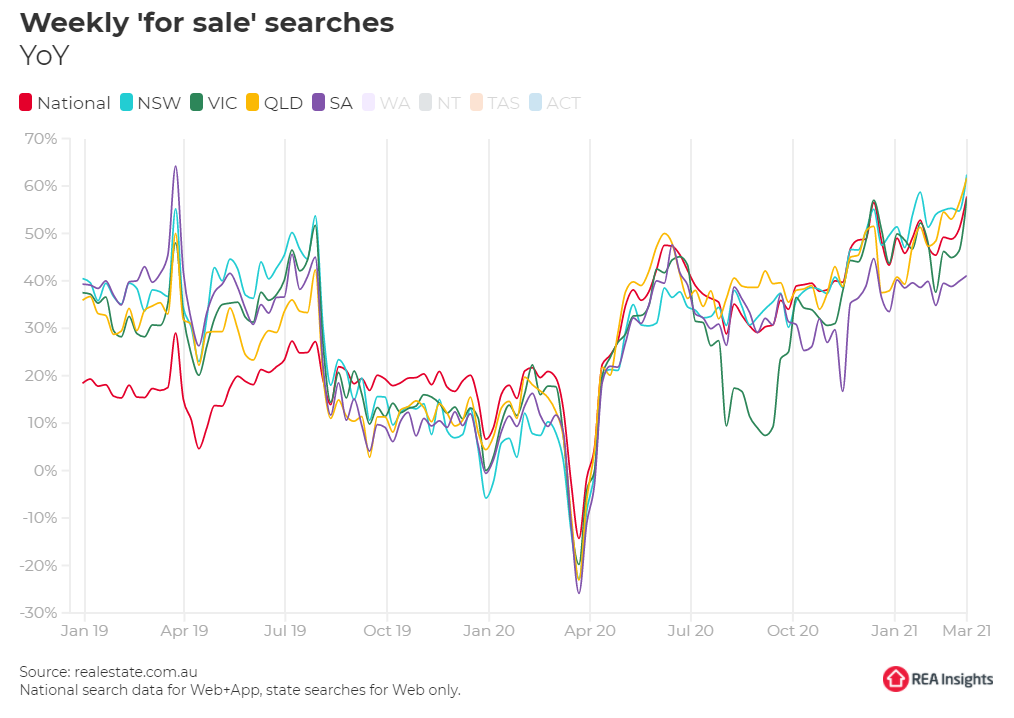

Second, weekly ‘for sale’ searches are way above the same time last year across every market:

Weekly for sale searches are up massively on the same time last year.

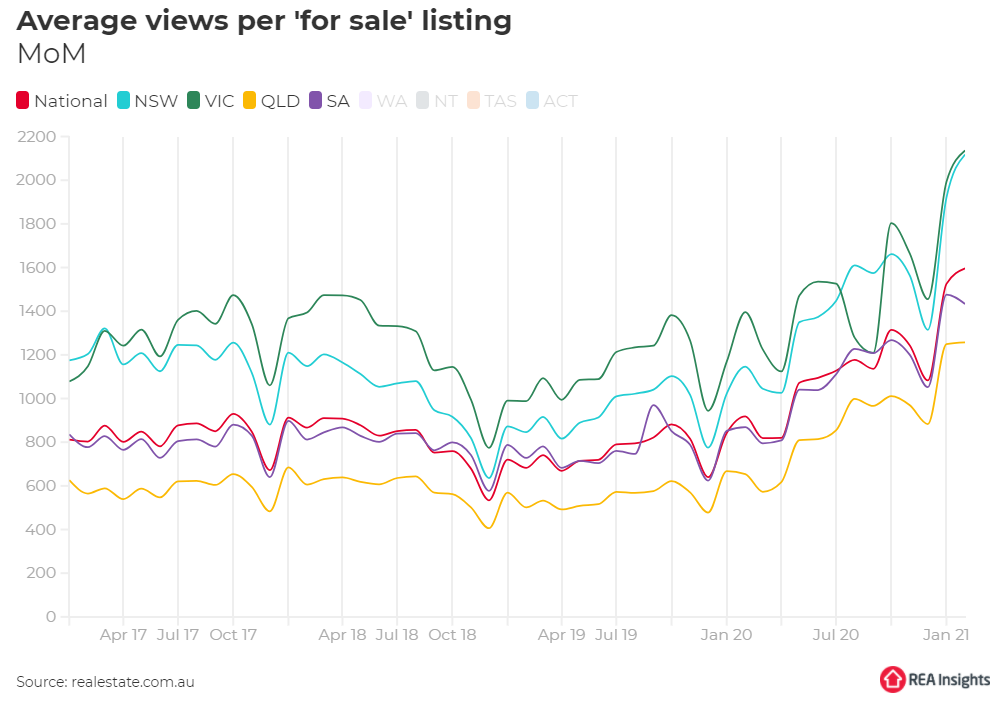

Third, the average view per ‘for sale’ listing on realestate.com.au is running way above the prior three years:

Average views per ‘for sale’ listing are running at three-year highs.

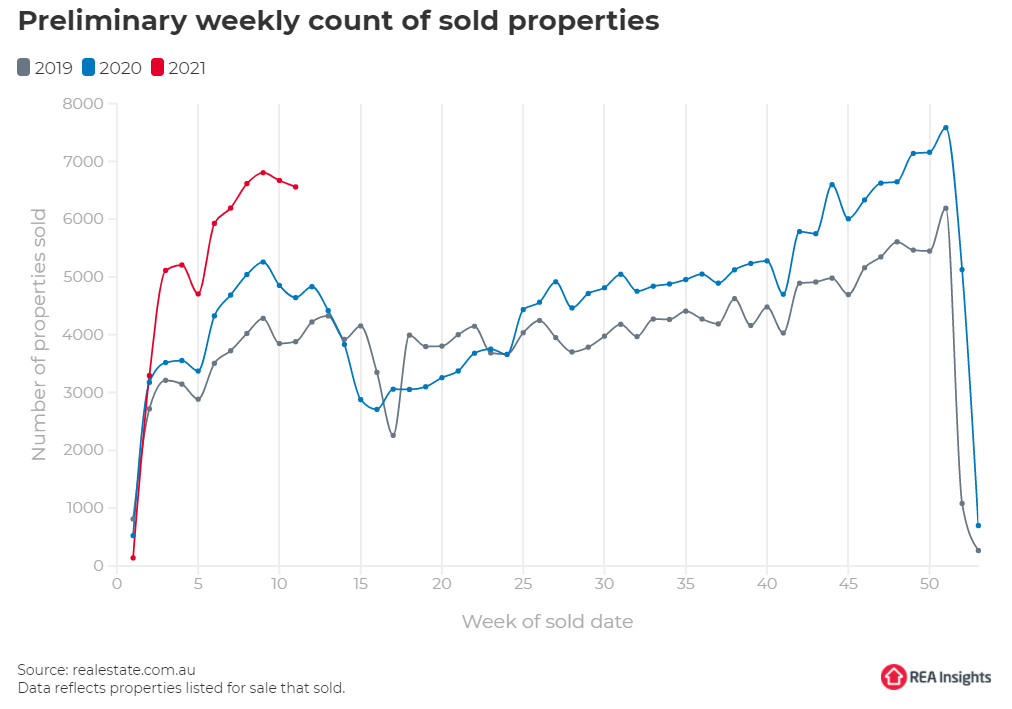

Finally, actual sold properties on realestate.com.au in 2021 is running well above the prior two years:

Sold properties on realestate.com.au are running way above the prior two years.

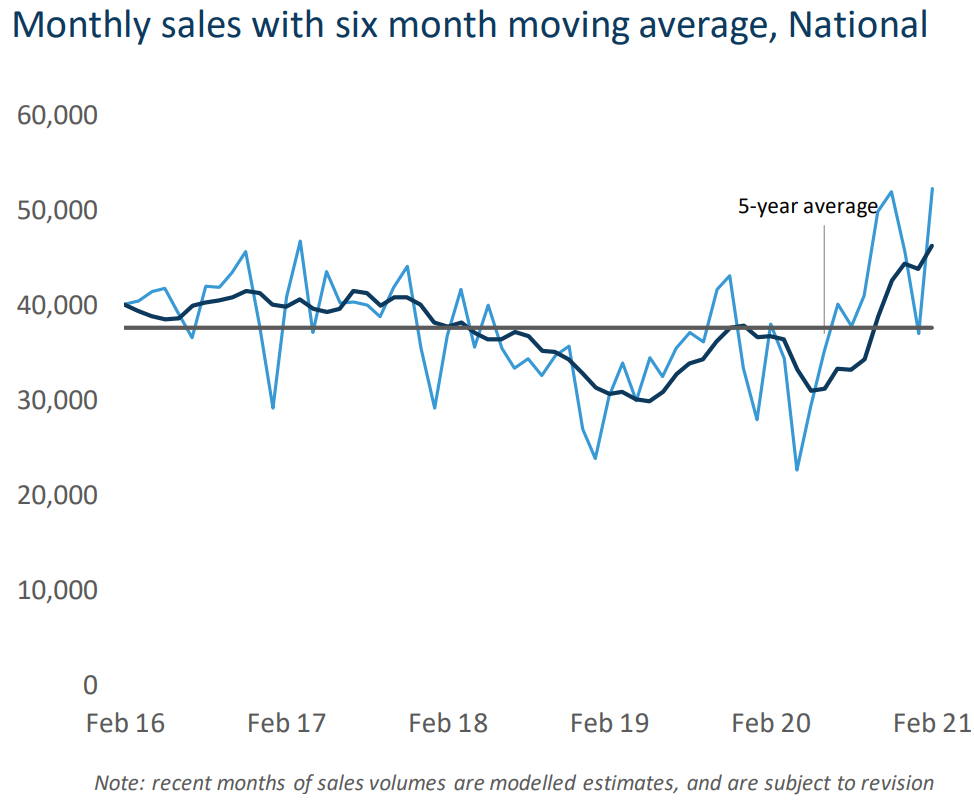

CoreLogic’s data shows similar strong demand amid constrained supply.

In particular, CoreLogic estimates sales volumes increased 12.6% nationally in the year to February, with sales tracking way above the five-year average:

Property sales volumes are booming, according to CoreLogic.

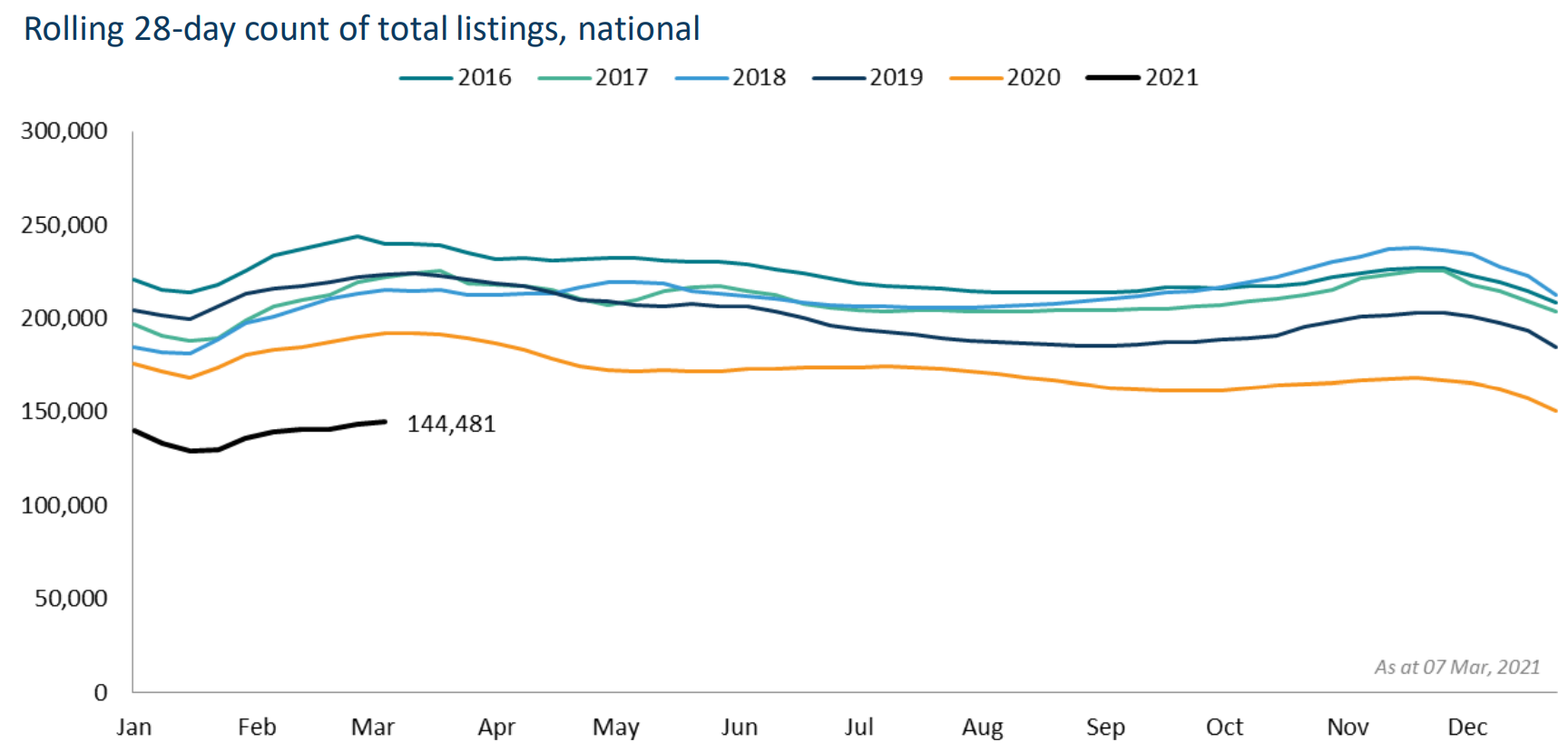

At the same time, total listings are running at historical low levels, down around 28% from the 2016 to 2020 average:

Property listings are running 27.5% below the five-year average, according to CoreLogic.

The insatiable demand is also reflected in record new mortgage demand and strong auction clearance rates. When combined with the limited stock on market, the inevitable outcome is turbo-charged price appreciation.