Digital Finance Analytics (DFA) has released mortgage stress data for February, which ratcheted back up to 41.8% of households, up from 39% in January.

DFA’s survey is based on a survey of 52,000 people and measures free cash flow. It attributes the lift in mortgage stress to three main factors:

- people are spending more and draining their savings; and

- the number of people on principal and interest rate holidays has fallen as mortgage repayment holidays end; and

- stimulus payments from JobKeeper and the JobSeeker Coronavirus supplement have been cut.

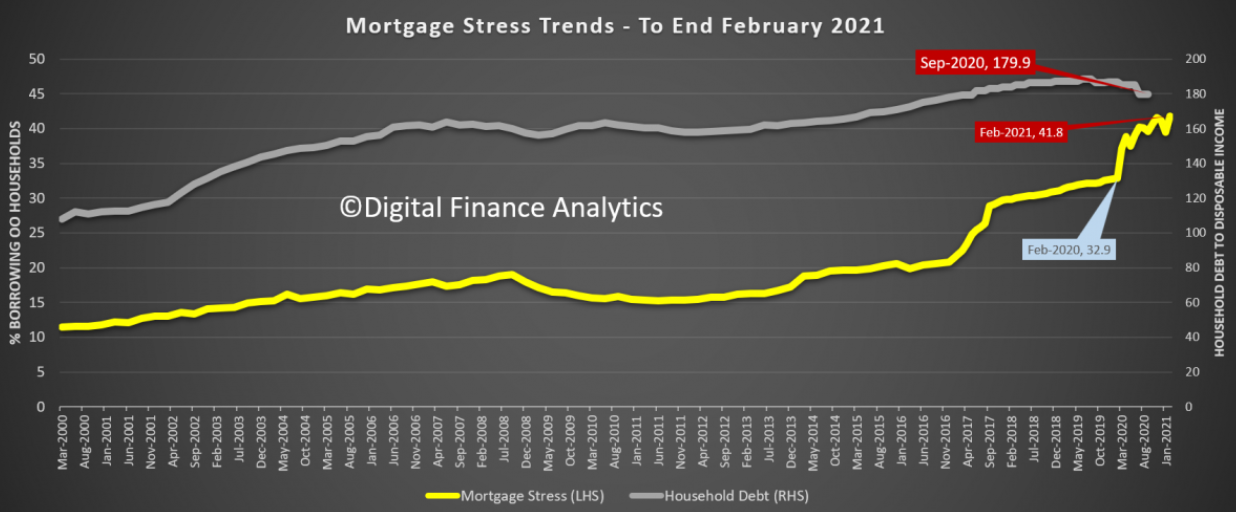

The next chart shows that mortgage stress is once again hovering near record high levels despite record low mortgage rates:

Mortgage stress rocketed back up in February towards all-time highs.

In actual numbers terms, “more than 1.5 million mortgage holders have cash flow issues” across the nation, accounting for 41.8% of borrowers. Rental stress is also running at 34.9%.

“Young growing families, and those on the urban fringe are most exposed” followed by affluent households with multiple investment properties.

I do not consider the rise in mortgage stress a material risk to the property boom. Money is cheap, the cost of buying versus renting is favourable across most markets, there is an acute market shortage of stock available to buy, and economic conditions are favourable.

All key indicators are pointing up for Australian property prices.