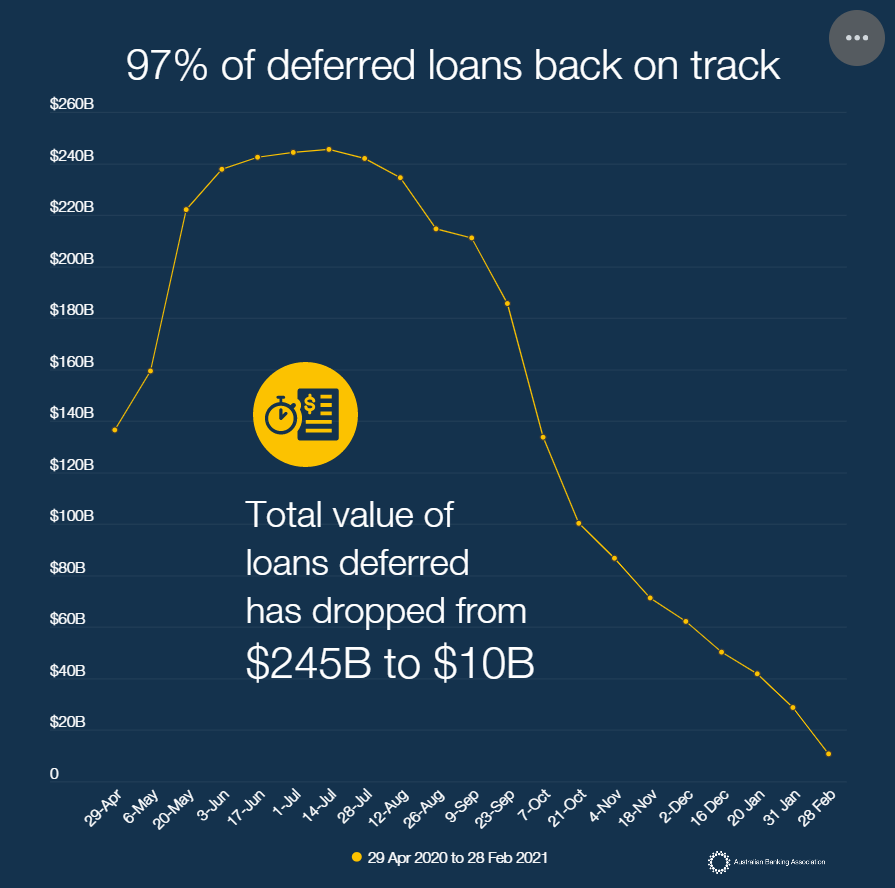

The Australian Bankers Association (ABA) yesterday released data on its members’ deferred loans, which shows the mortgage cliff that was towering over Australia’s property market last year has shrunk into a molehill, down 97% from its peak at the end of February:

Mortgage cliff gone.

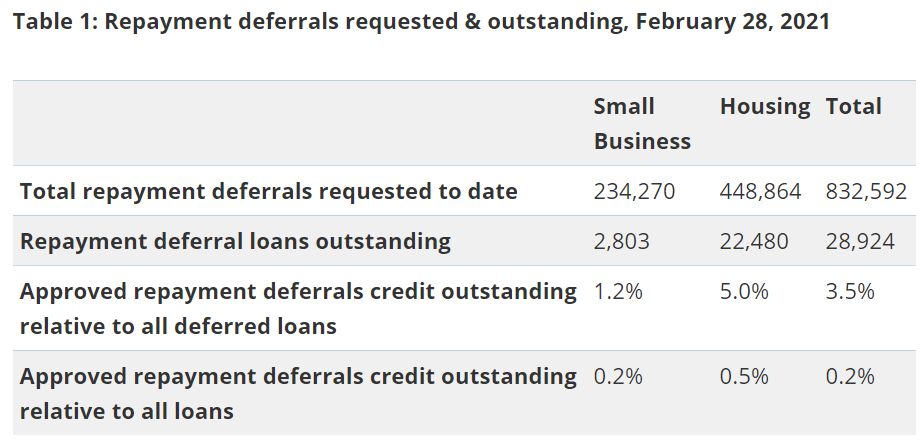

In raw numbers, there are now only 22,480 mortgages still under deferral, down 95% from the peak of 448,864 deferrals in April 2020: