The Australian dollar was soft again Friday night as DXY rallied. Some sting was taken out of the market by the Fed’s SLR decision and Treasury yields kept marching higher indicating further pressures to risk assets ahead. To the charts!

DXY is consolidating following its recent move off the lows. I see it moving higher from here:

US dollar to rise

The Australian dollar was weak again:

Advertisement

Head and shoulders top forming?

Oil rebounded. Gold is trying to rally in the belief that the Fed will ease again:

Oil and gold invert

Base metals did better:

Advertisement

Base metals

Big miners look increasingly like they are forming a new downtrend with another possible head and shoulders top:

Big miners into the pit?

EM stocks look like they could be blown over by a puff of wind:

Advertisement

Junk spreads were OK:

Junkyard dogs

US yields climbed again though the 30-year is definitely slowing as earlier duration steepens. The first sign of a top for the back-up:

Advertisement

Curve steepening slows at the long end

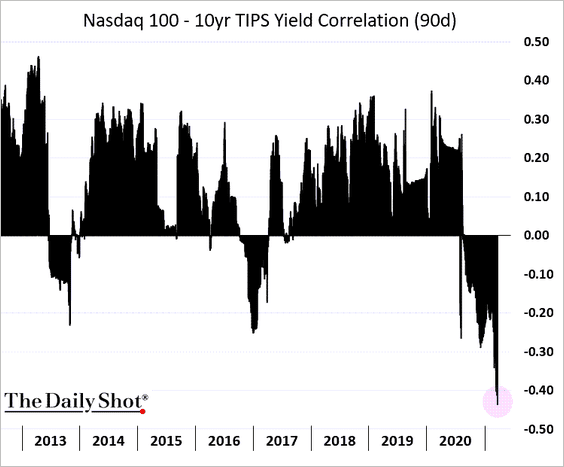

Stocks were odd. Tech lifted with yields and value fell as the Fed upset banking stocks with the SLR lapsing. A blip:

Stonks whacko

Advertisement

So, why do I see five reasons for further Australian dollar weakness? The first reason is the Fed is not going to intervene in the steepening bond curve so US yields can rise materially further:

Yield spike ahead not behind!

Why would the Fed intervene when it has:

Advertisement

Huge fiscal support.

The rising inflation it wants being signaled by yields.

No incentive to throw itself under asset price bus(t) when the market can do it by itself.

A curve steepening that should be more precipitous than any that came before it given the vaccine triggered catch-up growth and the speed of rebound.

And, a thirty-year yield that is already beginning to slow as markets continue to price structural deflation headwinds, meaning the back-up will be contained for US mortgages.

I can see the US 10-year yield jumping another 100bps and, as the chart shows, it generally happens fast.

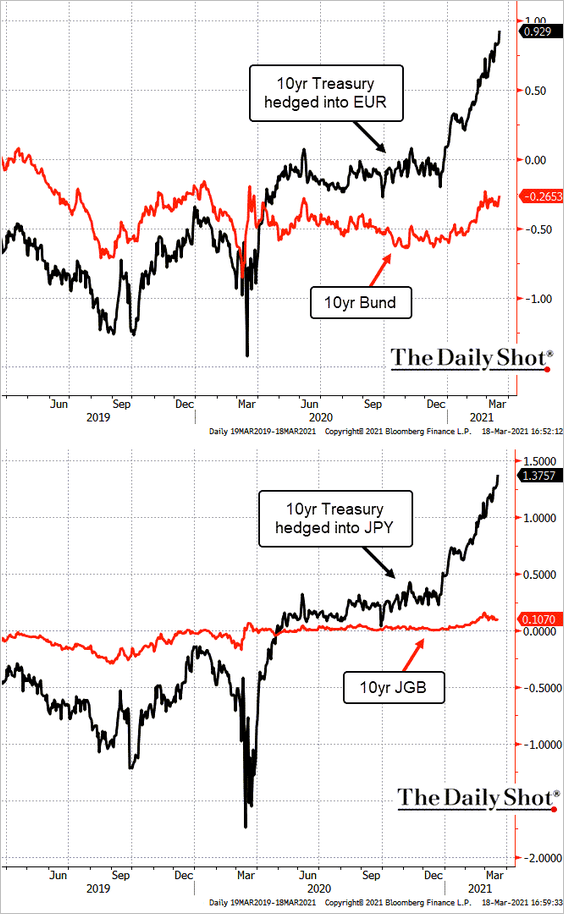

This brings me to the second reason why the Australian dollar will fall. US yields are blasting away from other developed economies, most notably Europe but also Japan meaning the carry trades of the last year will reverse:

The carry trades of the past year will reverse

Advertisement

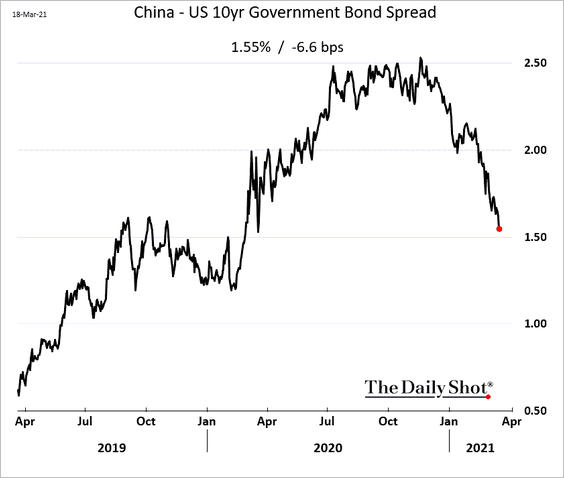

My third reason for a falling AUD ahead is that blasting off US growth gives China the chance to revert to its rebalancing project as it constrains credit. Thus the yield spread there is also reversing in the US favour:

No more China capital flows!

Soon to follow will be a falling CNY as growth slows:

Advertisement

CNY to break down

That’s my fourth reason for a weakening AUD. Any environment in which the USD is rising as it develops yield, inflation, growth advantages and CNY is falling is bad for emerging markets and commodity capital flows. That’s because the strong USD sucks capital out of EMs just as China sucks away fundamental demand for EM exports.

These were the conditions of the commodity and EM busts of 2015 and 2018. This time around there will be some offset in the US infrastructure package but not enough. Expect both to deflate in the months ahead.

Advertisement

This brings us the fifth and final reason to be AUD bearish. The same dynamic is bad for growth stocks and good for value which, in today’s unwinding tech bubble circumstances, means heavy price falls and some safe-haven flows into the USD as a result:

These five reasons all point to being short tech, short commodities (which perhaps the exception of manipulated oil) and short the AUD unless or until markets break with enough force to move the Fed to attack the long end of the curve or the US growth advantage passes. Neither of those is the base case.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.