CoreLogic’s head of research, Eliza Owen, agrees that Australia’s financial regulators are unlikely to act quickly to rein-in ‘risky’ mortgage lending via macroprudential tightening.

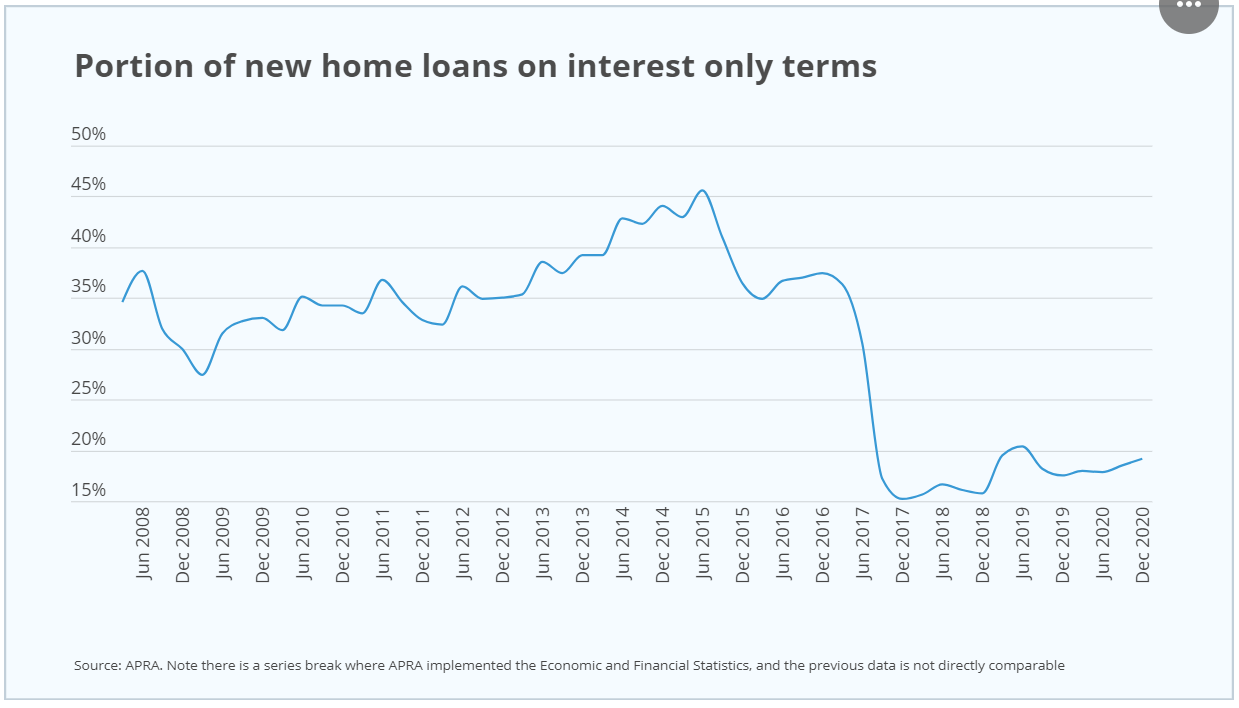

First, Owen notes that the proportion of interest-only lending remains at low levels (19.2% in December 2020), less than half the mid-2015 peak (45.6%):

Interest-only mortgage lending is running way below pre-2017 levels.

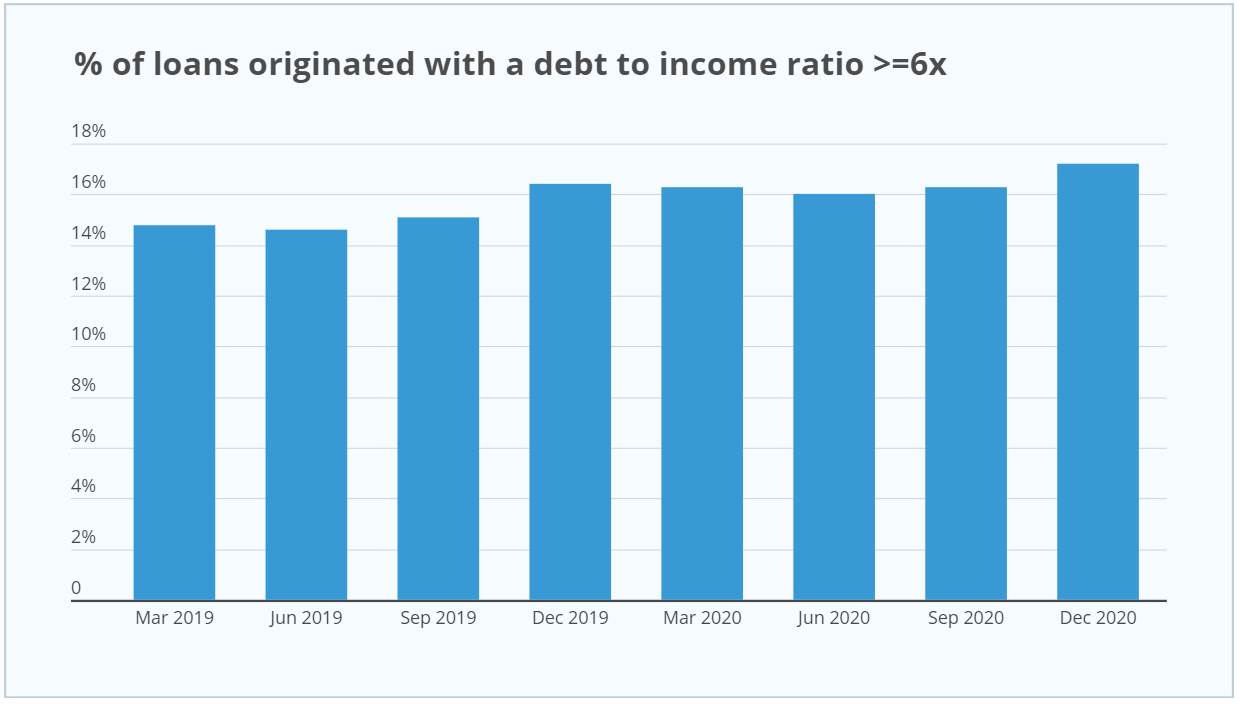

Second, while the proportion of mortgages made with debt to income (DTI) ratios above 6-times has hit a two-year high, the Australian Prudential Regulatory Authority (APRA) argues the share of debt to income lending was “within its historical average”:

Australian mortgage debt-to-income ratios hit a series high in Q4 2020.

However, Owen notes that continued price appreciation across Sydney and Melbourne could push the DTI ratio higher, given how expensive these markets already are:

This is because the house price to income ratio across Sydney has averaged around 8.5 since 2013, and has averaged 7.5 across Melbourne since 2015.

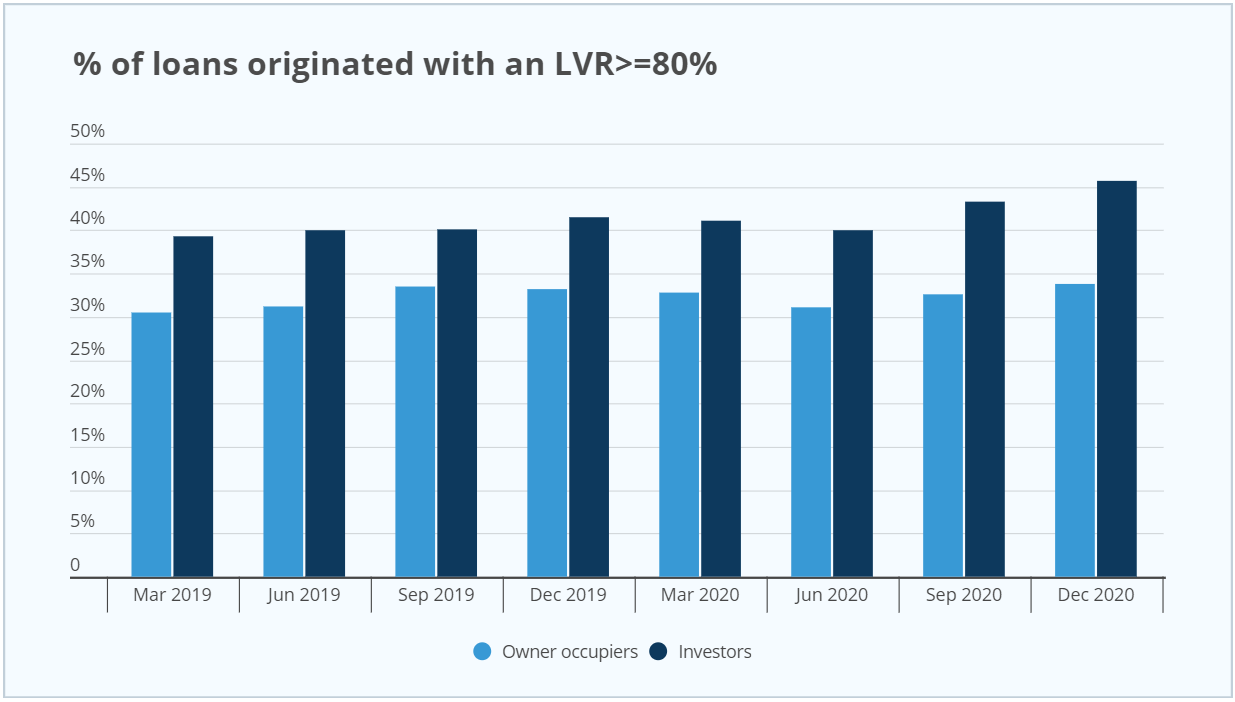

Third, the percentage of mortgages originated with a loan-to-value ratio (LVR) above 80% has risen across both owner-occupiers and investors:

The share of mortgages originated above 80% LVR has risen.

Nevertheless, Elisa Owen does not believe that regulators will take action to curb riskier mortgage lending:

The latest data from APRA indicates there is no blow out of risk in mortgage lending… The publication follows a recent address from RBA governor Phillip Lowe, who reiterated the strategy of maintaining a low cash rate for years to come, which is likely to continue supporting housing demand…

While APRA’s December quarter statistics show a trend towards ‘riskier’ styles of lending, the magnitude is not likely to be large enough to trigger a regulatory response; but if this trend continues, or indeed accelerates, it becomes more likely we will see a regulatory intervention aimed at curbing financial stability risks related to the housing sector.

My view is that the regulators are unlikely to act anytime soon because the mortgage/property boom is being driven by owner-occupiers (including first home buyers), which makes macro-prudential intervention inherently more difficult than clamping down on speculative investors.

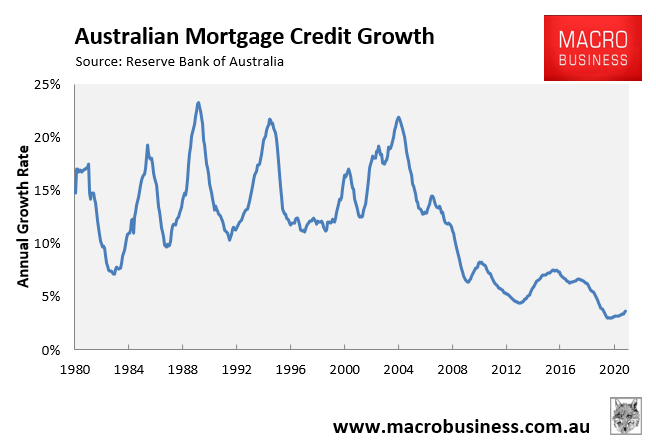

Australian mortgage credit growth also remains near historical lows, because owners of existing mortgages are repaying their loans quickly, offsetting the uptake of new mortgages:

Australian mortgage credit growth is near record lows, making macro-prudential intervention more difficult.

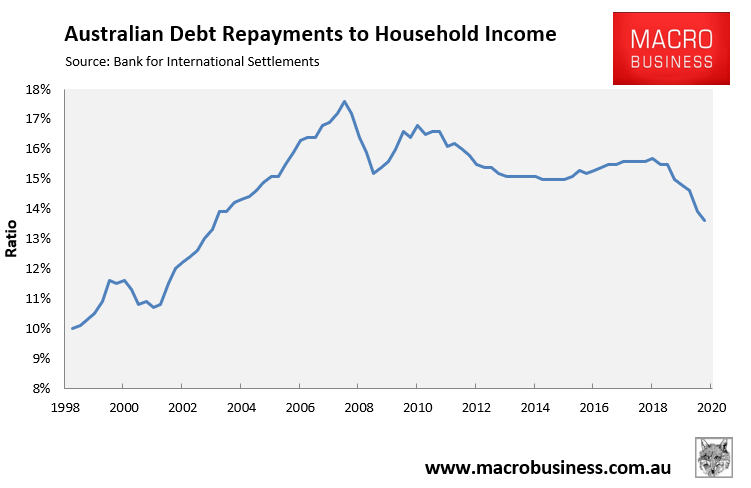

Moreover, actual loan repayments (both principal and interest) are tracking at their lowest level in 18 years, according to the Bank for International Settlements:

The proportion of household disposable income used for debt repayments is the lowest since 2003.

In short, financial stability risks have not increased sufficiently to push Australia’s financial regulators to imposing macroprudential tightening.