By Gareth Aird, head of Australian economics at CBA:

Key Points

- The sharp drop in net overseas migration due to international border closures raises the likelihood that wages growth lifts as the labour market tightens.

- Skill shortages have more chance of manifesting themselves while net overseas migration is low.

- We expect the unemployment rate to fall faster than the RBA anticipates and wage outcomes could surprise to the upside.

Overview

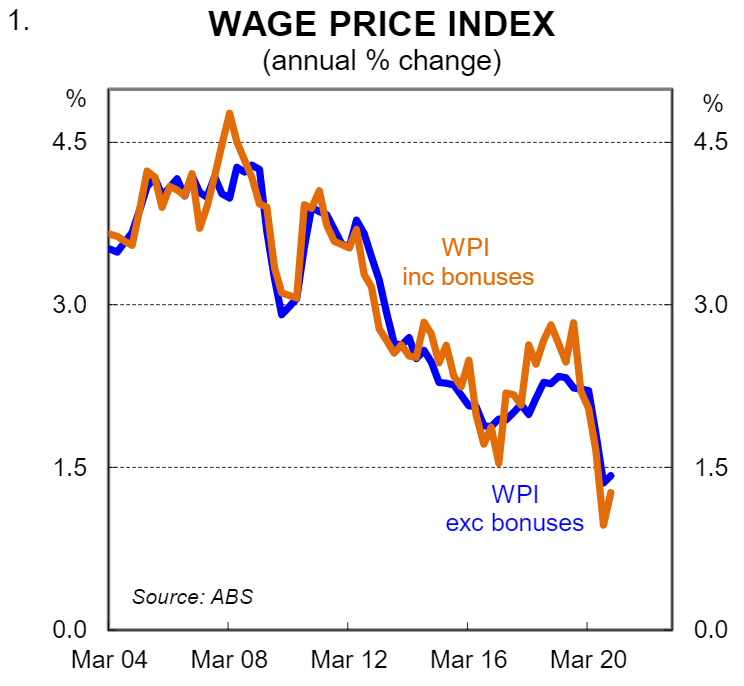

Wages growth is very soft. But the labour market is tightening. And as the unemployment rate moves lower, wages growth should gradually rise. The level of unemployment below which wages growth will materially rise, however, remains an unanswered question.

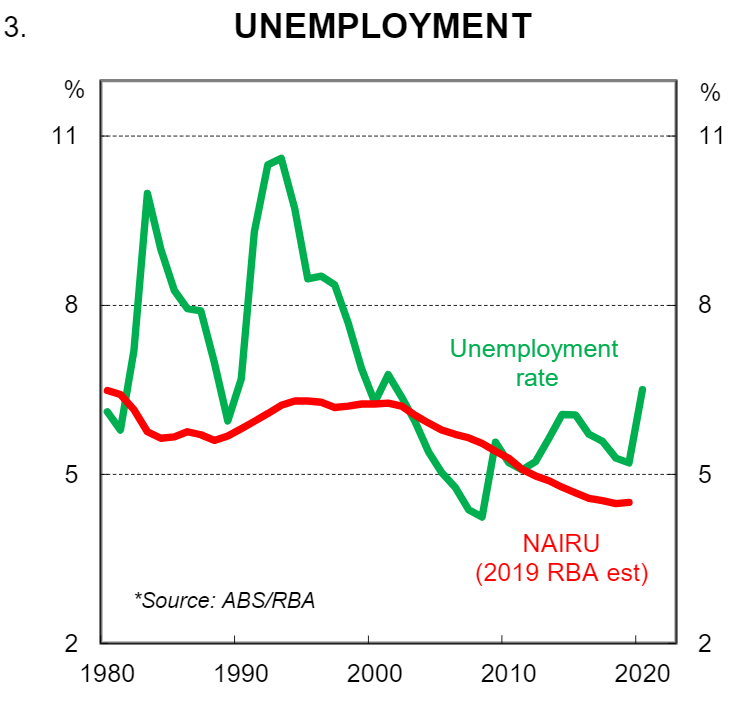

The NAIRU –or non-accelerating inflation rate of unemployment –is broadly speaking, that level. It is the benchmark for assessing the degree of spare capacity and inflationary pressures in the labour market.

The latest official RBA estimate from a speech in mid-2019 puts the NAIRU at 4½% in Australia (chart 3). But as RBA Governor Lowe stated on 10 March 2021, “it’s entirely possible (that’s it’s lower than 4½%), none of us know”.

The Governor’s assessment that “none of us know” is correct because pre-COVID the unemployment rate was around 5%, but wages growth was stuck at a historically low~2¼%. We didn’t achieve a 4½% unemployment rate and were therefore unable to confirm if the RBA’s revised estimate of the NAIRU was correct.

However, whilst it is entirely possible that the NAIRU is below 4½%,it is also entirely possible that with the international borders closed the NAIRU is higher than 4½%. If firms are not able to recruit from abroad then as the labour market tightens skill shortages will manifest themselves faster than otherwise and this will allow some workers to push for higher pay.

We expect the labour market to tighten at a decent rate from here and forecast the unemployment rate to be 5.0% by end-2022 (RBA (f) 5.5% end-2022). Whilst we have high conviction that the unemployment rate will drop faster than the RBA anticipates, there is a lot of uncertainty around when the international borders will reopen, what that means for net overseas migration (NOM)and how that will impact wage outcomes.

We do not have all the answers. But we want readers to take an open mind to the prospect that wages growth lifts at a higher level of unemployment than the pre-COVID relationship between unemployment and wages would suggest. This note explains why. And we also outline why underemployment matters for wage outcomes.

Employee bargaining power is higher with lower net overseas migration

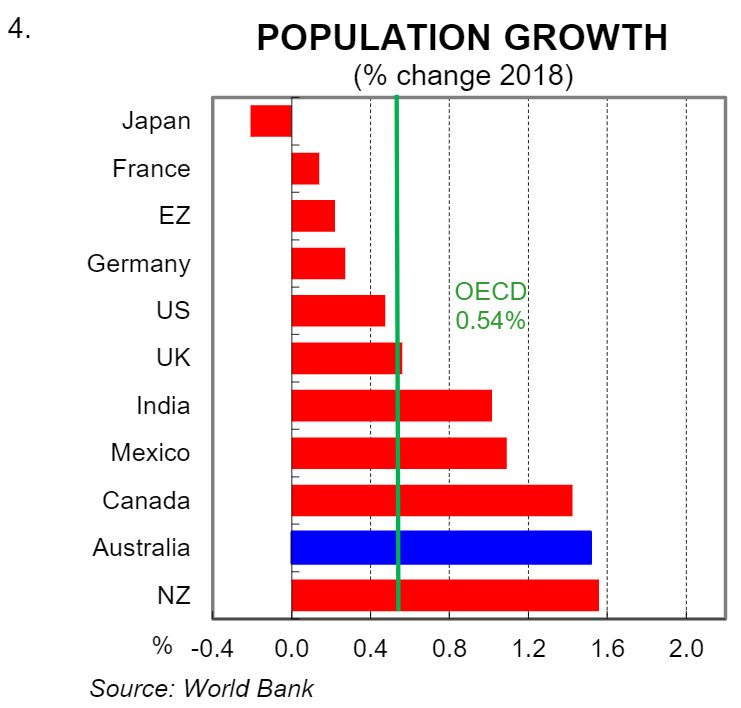

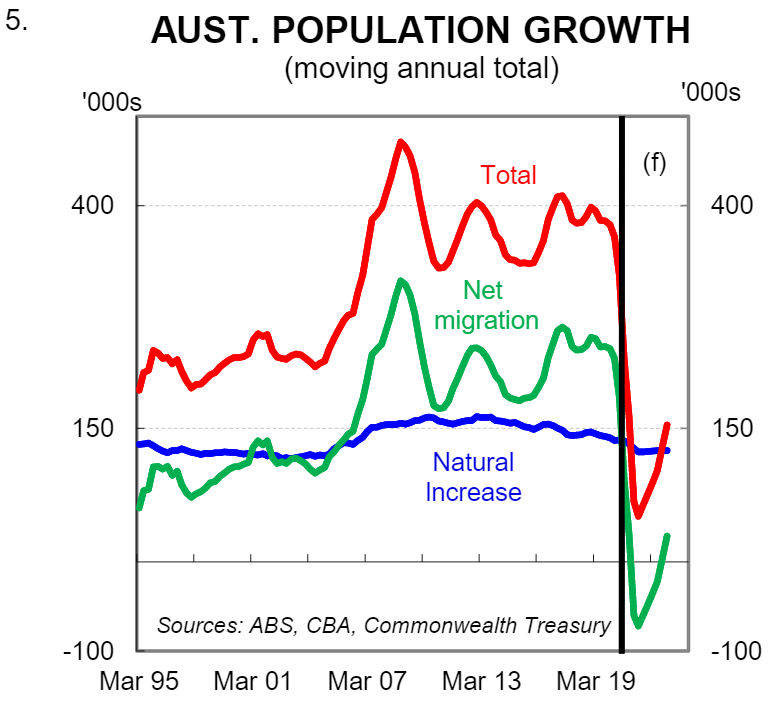

The capacity of employees to negotiate pay rises is impacted by the level of slack in the economy. But it is also influenced by the rate of growth in labour market supply. Pre-COVID Australia had for many years run a very high immigration intake by OECD standards and this meant strong population growth (chart 4). The level of slack in the labour market seemed to make very little difference to the level of immigration in the economy. More specifically, Australia had a high level of immigration despite low wages growth and a relatively high level of underutilisation (the broadest measure of labour market slack).

From a wages perspective, immigration augments the supply of labour beyond what would have naturally occurred. That intensifies the competition for existing jobs while of course also adding to the demand for labour. The bigger the supply side shock, the more that the competition for existing jobs intensifies. This puts downward pressure on wages initially, but its effect should only be temporary. However, if the supply side shock continues the temporary impact may not prove to be so short lived.

“Skilled” migration was worth around~70% of the total migration programme outcome pre-COVID. From the perspective of an employee, working in an industry that has a skills shortage means that the labour market in that profession should be tight. In industries with skills shortages, bargaining power between the employee and employer should move more favourably in the direction of the employee and higher wages should be forthcoming.

But in Australia’s case pre-COVID there was no evidence of widespread skills shortages based on the broad-based weakness in wages growth. The relatively high intake of skilled workers looked to be a pre-emptive strike on the expectation that there would be skills shortages in the future.

Things are very different right now with the international borders closed. In the October 2020 Budget the Government forecast NOM to turn negative in 2020/21 and 2021/22 (chart 5). This means that as the labour market tightens, “skills shortages” will manifest themselves because employees will not able to hire from abroad like was previously the case. As a result, employees in many industries have had a lift in their bargaining power that is independent of the level of slack in the local labour market. Essentially talent is scarce because firms can’t hire from a global pool of labour.

That situation of course will not remain indefinitely. But it is entirely possible that over 2021 and 2022 pockets of wages growth will start to emerge if the labour market tightens at a sufficient pace. Indeed the high level of job vacancies in the economy right now suggests that in some industries wages pressures could surface over the coming two years.

To be clear, at this stage we are not forecasting any material lift in wages growth over our forecast horizon. We forecast the wage price index at 2.0%/yr end-2022 (RBA (f) 1.75%/yr end-2022).

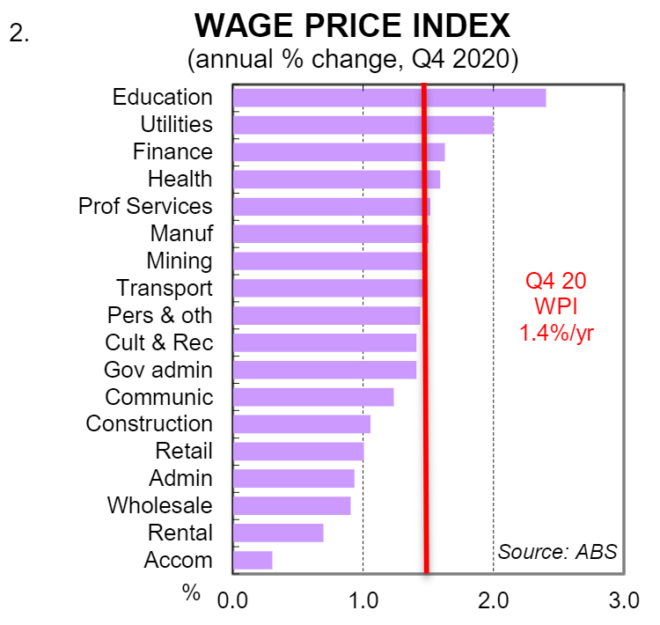

But if the rate of NOM remains low next year and the labour market tightens as we expect then the risk is that wages growth accelerates a little quicker than the RBA and most other forecasters expect. We will be watching the industry composition of the wage price index very closely over 2021 for any evidence that skill shortages are translating into higher wages. If wages outcomes surprise to the upside it will make it a lot harder for the RBA to convince the markets that the cash rate will not be raised until 2024 “at the earliest”.

Underemployment also matters

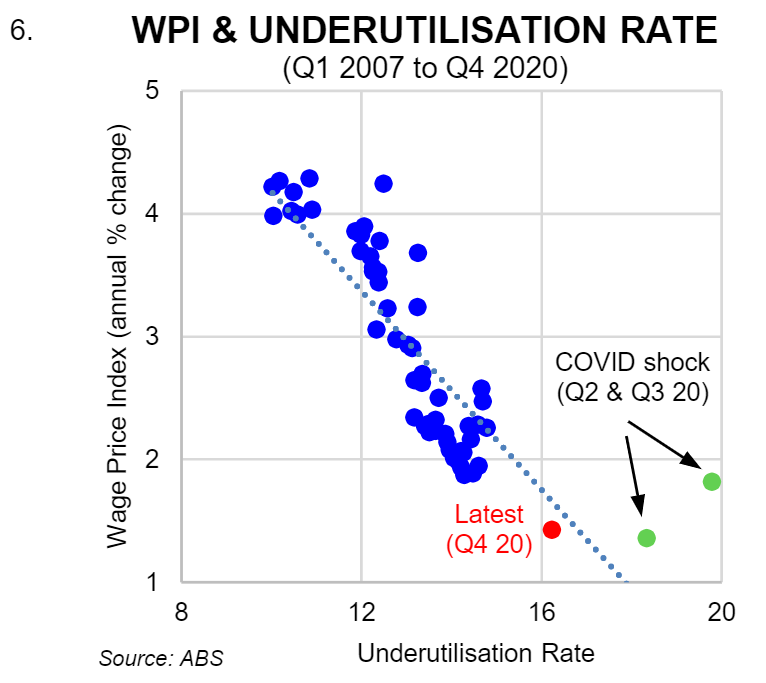

There is a strong relationship between the underutilisation rate, which is the sum of the underemployment and underemployment rates, and the wage price index (chart 6). That means that the level of underemployment in the economy also has an impact on the NAIRU.

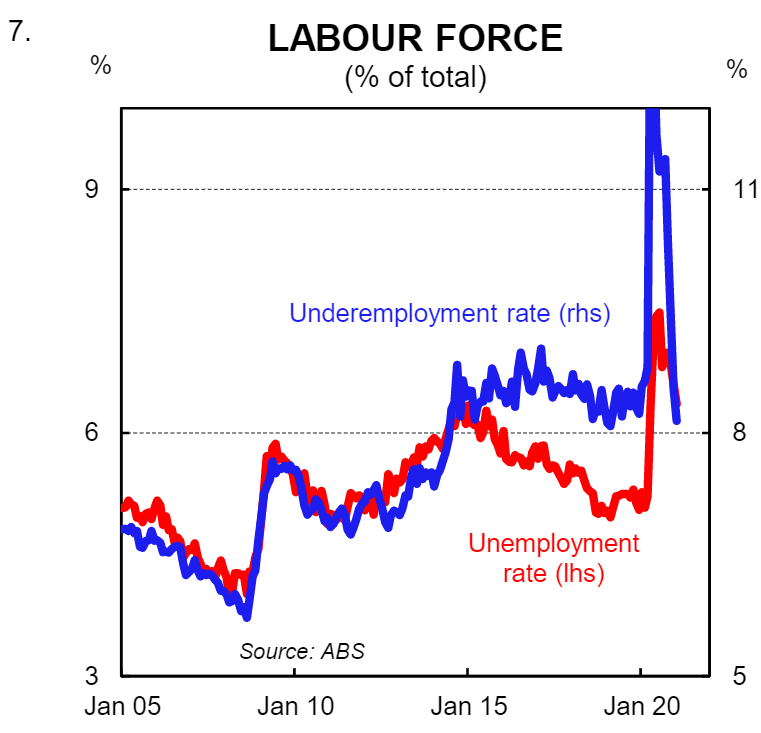

Pre-COVID the spread between the unemployment and underemployment rates had increased. But post-COVID that spread has decreased (chart 7). The upshot is that changes in the unemployment rate alone are no longer a sufficient proxy for changes in labour market slack if the spread between the unemployment and underemployment rates is moving.

Put simply, the NAIRU is likely to be higher than whatever it was pre-COVID if the spread between the unemployment and underemployment rates remains tighter than the pre-COVID spread.

Things are different now –keep an open mind

The COVID-19 induced economic shock means that the economic fraternity should look at issues from a more holistic perspective. The phrase “this time is different” is very much true right now. Models are generally an economists’ best friend, but qualitative judgements need to be made if the broader dynamics have changed which challenge the previously assumed relationships between economic variables.

Right now there is a lot of discussion in Australia around how low the NAIRU may be. Indeed the RBA appears more open to the idea that it may be even lower than their pre-COVID downwardly revised estimate of 4.5%. But the sudden halt to net overseas migration and the potential for the migrant intake to be a lot lower next year than pre-COVID levels means that the NAIRU is more likely to have gone up rather than down.

We will continue to retain an open mind to how the economy may evolve over the next few years. And we would not be surprised to see some skills shortages manifest themselves as the labour market tightens in the form of pockets of wages growth.