DXY faded its opening gap yesterday as markets ran out of inflation news to trade upon. As a result, the Australian dollar clung to the mid-77s. More trouble is ahead. The charts begin with DXY which eased:

The Australian dollar has now traced out a perfect head and shoulders top. Any drop below 0.76 will break the neckline and open big downside:

Oil is still struggling and also has a head and shoulders pattern developing. If this were to fall then it might short-circuit the rates back-up and save growth stocks:

Base metals did better:

Miners not so much:

EMs still look like a house of cards:

Junk was fine:

US yields flamed out, the key to the night’s action:

As stocks rebounded led by tech:

Westpac has the wrap:

US existing home sales in February fell more than expected to 6.2m (est. 6.5mn, prior 6.7m). The National Association of Realtors Chief Economist Yun said that the data reflected a shortage of supply and that demand remains high. He cautioned that rising mortgage rates will affect affordability and slow growth in sales in coming months. The median house price is now up 15.8%y/y (all regions had double digit gains) and inventory is at a record low of 1.03m units, with properties selling in 20 days (also a record low). Chicago Fed national activity survey index in February fell to -1.09 (prior +0.75), led by declines in personal consumption and housing. The Chicago Fed cited weather as a continuing factor in the decline (the polar vortex hit in February).

FOMC member Barkin did not give any time frame for the removal of accommodation, favouring an outcome-based policy stance rather than a calendar-based one. He said that the conditions for tapering have not yet been me, and that the Fed would start conversations on slowing asset purchases well before any action. On labour market measures, the best indicator was thought to be the employment to population ratio. He expected the Fed to look through rising inflation over the next six months, base effects at play.

ECB President Lagarde said in a blog post that the ECB remains ready to adjust all measures if necessary, retaining the option to adjust bond purchases at any time.

The US, EU and UK applied sanctions on Chinese individuals with respect to human rights. The UK also stated that the chances of gaining a trade agreement with China were slim. China retaliated with sanctions on several individuals and entities.

Germany extended its current lockdown restrictions until 18 April. Germany also increased its borrowing projections by EUR240bn in 2021, and will present another high-debt budget proposal for 2022 this week (again waving Maastricht restrictions and the German fiscal brake).

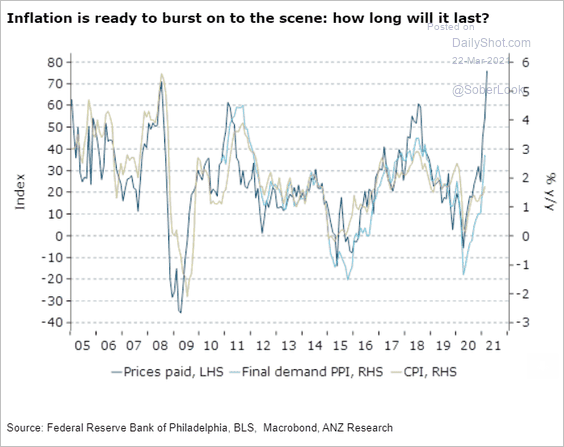

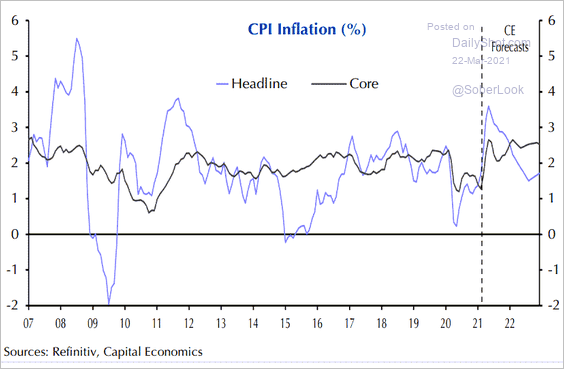

So, an evening of counter-trend action as yields eased. Could it continue? Not likely. Inflation is coming:

Though the spike will be temporary but with a higher base:

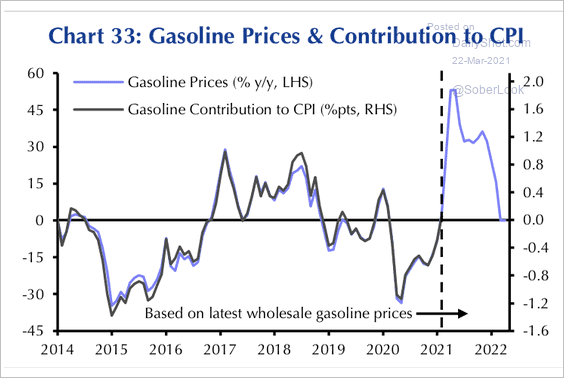

Led by oil:

But still unable to generate a sustainable pulse:

Then there is this, at WaPo:

- The Biden Administration is preparing a $3tr infrastructure package.

- $1tr will focus on hard infrastructure in roads, rail and green energy rollouts.

- The other $2tr is focused on social infrastructure which includes universal prekindergarten, child care and free community college.

All productivity-enhancing stuff and in that sense self-funding but tax hikes on the rich will pay for it as well.

More to the point for this discussion, such a mix of spending, more oriented to human infrastructure, would be particularly bad for the Australian dollar. Given it would still result in US growth, inflation and yield leadership but without material commodity price offsets from hard infrastructure demand.

I still see trouble ahead for commodities, EMs and tech on this. But watch oil, if it breaks then the heat will come out of the bond back-up earlier than expected, though that would also hit the Australian dollar as commodities more widely deflate.