The developing trend of higher US yields, a stronger DXY, lower emerging markets and commodities and busting tech continued last night. Forex followed suit. DXY is pinning its ears back as EUR pukes:

DXY powers as EUR swoons

The Australian dollar was pulverised against the US dollar and held against EUR:

Australian dollar smashed versus DXY

Advertisement

AUD was still mostly stronger versus emerging market forex:

AUD versus EMs

Brent and oil both fell:

Gold and oil both weak

Base metals did better but this won’t last as DXY slams them:

Advertisement

Base metals on a DXY hiding to nothing

Miners were soft:

Big miners OK so far…

Emerging market stocks have a fugly chart:

Advertisement

EM stocks falling down the mountain

Junk bonds are rolling, This is key to how far the tech bust gets. If this turns unruly then the Fed will be forced to act:

Critical: Junk spreads widening. Watch for Fed pressure

US yields climbed again however the 30-year fell and the 2-30 curve flattened. If this continues then the Fed will not move:

Advertisement

Curve flattens

The Nasdaq has only clear air below it. The S&P was strong. Europe too as the value elephant tramples growth:

Tech Wreck 2.0

Advertisement

Nordea has some great charts that clearly illustrate this is NOT over. The DXY wrecking ball is swinging against everything:

DXY smashes all

US growth is stronger versus all:

Advertisement

US boom

Especially a half-arsed Europe:

Weak Europe

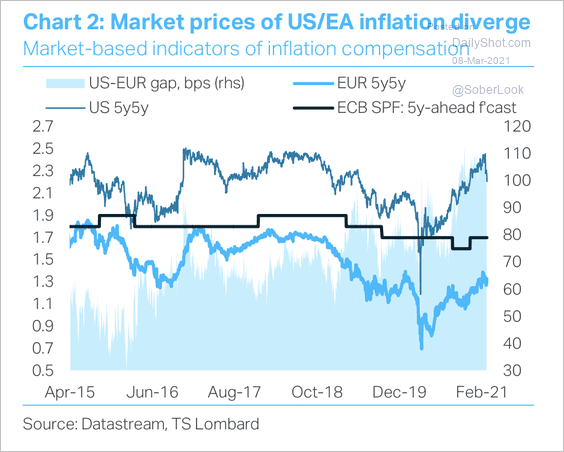

The US has much stronger inflation too:

US inflation warming up

And, higher yields as well:

Advertisement

In short, the US recovery is so strong that everything is paling by comparison and capital is flowing into it instead of out of it, the opposite of what would usually be the case in a global recovery. The rising yields are also killing growth stocks which is spawning a safe haven DXY trade to boot. Finally, the market is entirely on the wrong side of the DXY boat being heavily short.

The only thing that can stop this now is the Fed redoubling on easing. But so long as the 30-year bond is contained it won’t. Indeed, it’s still busy tightening at the margin, at the FT:

The Federal Reserve is ending the bulk of the remaining emergency facilities it rolled out last year to support financial markets through the coronavirus crisis, in the latest sign that the economic recovery is gathering momentum.

The US central bank announced on Monday that it will allow three lending programmes to expire as scheduled at the end of the month, citing low usage. The Commercial Paper Funding Facility, the Money Market Mutual Fund Liquidity Facility, and the Primary Dealer Credit Facility were launched in March last year to combat turbulent trading conditions that engulfed markets when investors scrambled to hold cash.

Goodbye Fed facilities

Advertisement

We haven’t even seen Chinese slowing yet, the next shoe to drop. And Europe still needs more easing with possible further big downside for EUR.

Unless or until there is enough market stress to get the Fed off its butt, DXY is free to run higher and reflation is off everywhere else.

The Australian dollar has well and truly topped out here.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.