The Australian dollar took off last night after the FOMC meeting concluded with a dovish statement. Yet, under the bonnet, the Fed did shift to a more hawkish outlook and the long-end of the bond curve barely shrugged as yields marched higher. In short, the meeting delivered exactly what I expected, a passive shift in a hawkish direction within a still dovish context. To the charts.

DXY was whacked:

Enough to punch DXY lower

The Australian dollar took off:

AUD has a head and shoulders topping pattern developing

Oil fell and gold lifted:

Gold beats oil for once!

Base metals did little:

Yawning metals

Miners were weak in context:

Yawning miners

EM stocks still look perilously poised:

EM stocks on a hiding to nothing?

But junk lapped it up. No need for Fed to ease here:

Junkyard easy

Crucially, though, US yields were squashed as the short-end and climbed at the long, the exact opposite of what a dovish Fed would want given the latter determines mortgage rates:

Fed stoopid?

Stonks were bid but forgive me if I say it was a little half-hearted:

Stonks fakin’ it?

So, it was a dovish statement:

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation running persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer‑term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved. The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time. In addition, the Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee’s maximum employment and price stability goals. These asset purchases help foster smooth market functioning and accommodative financial conditions, thereby supporting the flow of credit to households and businesses.

But, the outlook was raised materially for growth and inflation short term, less so long:

Recovery intact before MOAR

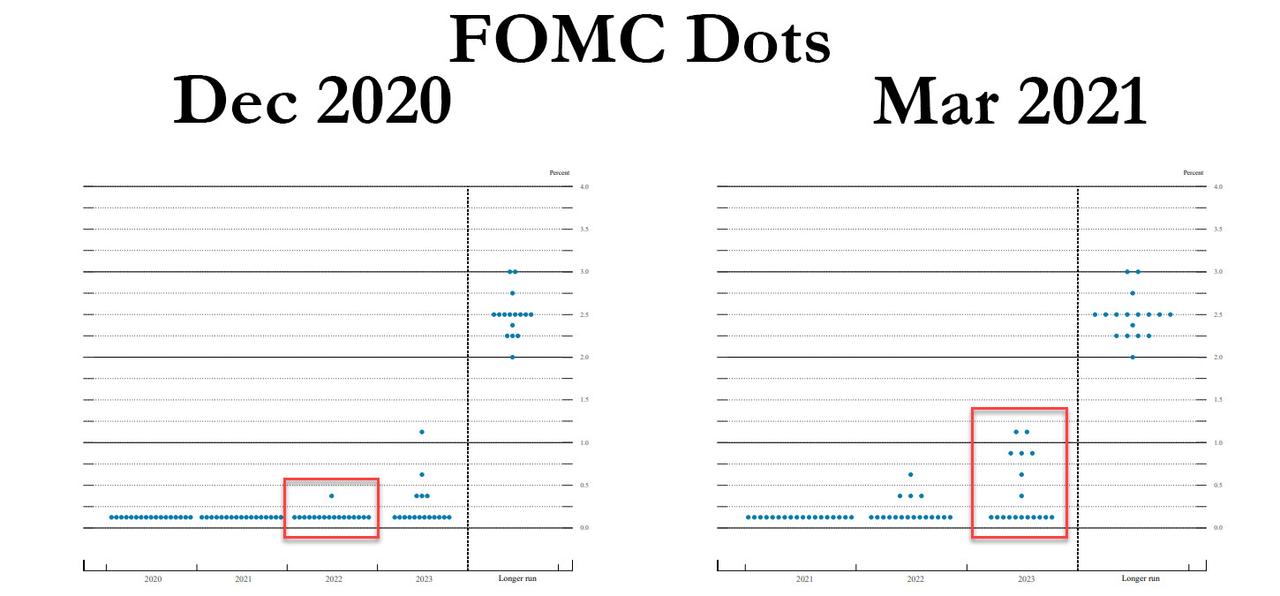

As expected, the dots shifted a little hawkish:

Join the dots

So, we have a situation now where the Fed is sitting on the short-end to juice growth until it will suddenly deliver 10-12 rate hikes in 2024. On top of that, its outlook already meets 2% inflation yet it still has to incorporate forthcoming mandatory low wage rises plus another $2-4tr in infrastructure spending that adds 1-2% to GDP per annum out past 2023.

Why would anyone buy the ten-year bond in this situation? They won’t. The one thing that the Fed has not done is to choke off the yield shock as we all now know that yields will have to lift by another 1% before 2024. This, as the months ahead include the base effect inflation spike, the debate and delivery of massive new fiscal, and, before long, rumour will grow of tapering asset purchases early next year.

There is nothing here that changes my mind about US growth, inflation and yield leadership meaning the bottom is in for DXY, the top is in for AUD and there’s trouble ahead for tech, EM and commodities:

US leadership on all fronts