The Australian dollar was absolutely smashed again Friday night as the great yield reversal continues. It did manage to bounce back by the close but the headwinds are building.

First up, the charts. DXY tore higher as EUR wilted with a dovish ECB on the horizon plus vaccine, yield and inflation advantages swinging to DXY:

DXY is basing and building a new uptrend as EUR crumbles

The Australian dollar was flushed then rebounded though it was more firm against other DM forex:

Advertisement

AUD breached 76.20

Brent oil surged as OPEC grasps at its share of the recovery. Gold is going lower as yields rise:

Brent oil versus gold

Advertisement

Base metals held on but they are buggered as DXY takes off and China slows into H2:

Base metals are in trouble

Big miners held on too, aided by oil:

Advertisement

Big miners still high

To put it bluntly, EM stocks are fooked. There is nothing that they hate more than a strong US and weakening China:

EM stocks killed by DXY

Junk appears to be rolling as well. If this were to gather pace much then I’d expect the Fed to act on Operation Twist and give risk another run:

Advertisement

Junk bonds rolling over?

US yields up with oil:

US yields still climbing

Stocks rebounded on strong jobs. In the case of tech, it’s the proverbial dead cat bounce:

Total nonfarm payroll employment rose by 379,000 in February, and the unemployment rate was little changed at 6.2 percent, the U.S. Bureau of Labor Statistics reported today. The labor market continued to reflect the impact of the coronavirus (COVID-19) pandemic. In February, most of the job gains occurred in leisure and hospitality, with smaller gains in temporary help services, health care and social assistance, retail trade, and manufacturing. Employment declined in state and local government education, construction, and mining.

…The change in total nonfarm payroll employment for December was revised down by 79,000, from -227,000 to -306,000, and the change for January was revised up by 117,000, from +49,000 to +166,000. With these revisions, employment in December and January combined was 38,000 higher than previously reported.

Advertisement

So, more inflationary pressures, if you’re worried about inflation, and the market is. Yields can go higher yet:

US Treasury selling not overdone

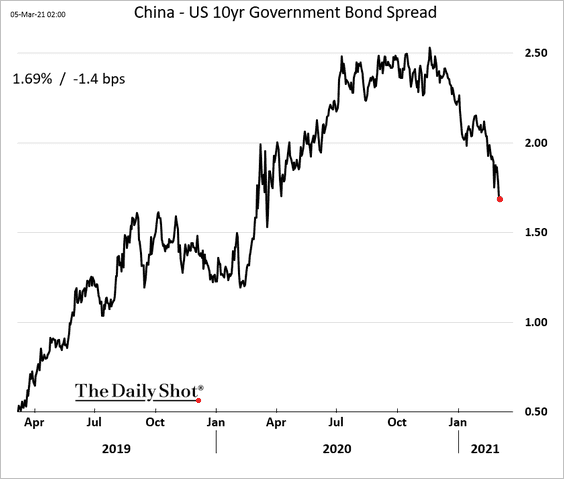

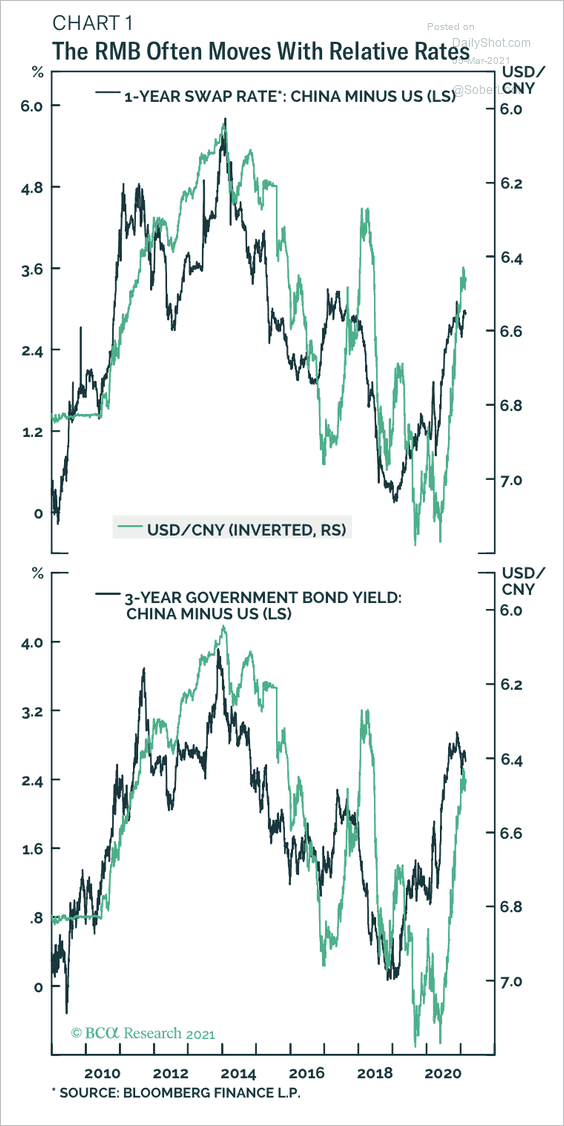

And that’s not the end of it. Another shoe is beginning to drop for yield spreads and forex: a slowing China:

Advertisement

CNY and EUR are both rolling as the US develops its growth, yield and inflationary advantage. The market is still on the wrong side of the boat big time:

Net US dollar positioning

Advertisement

What can I say? There are still very powerful AUD tailwinds, in particular in the amazing global steel price blowoff which is keeping iron ore buoyant.

But the financial reflation that had everybody and the kitchen sink buying commodities and the AUD is reversing. Even more quickly than I have discussed for the past few months.

The Fed could still intervene and restore the AUD financial bid but why would it until or unless market action turns unruly and threatens 30-year mortgages?

Advertisement

With a more dovish RBA, the Australian dollar may have already peaked.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.