Friday night saw a weaker DXY which helped drive a pop in the Australian dollar and risk assets generally:

DXY pause that refreshes

Brent jumped out of its swoon. Gold is hanging on:

Oil hiccup over?

Base metals all partied:

Base metals the pause that depresses?

Miners went along for the ride:

Same goes, big nose

EMs stocks too though they still dangerously caught in a downdraft:

A nasty chart!

Junk is fine. No Fed coming here:

Junk thumbs its nose at Fed put

US yields lifted too suggesting the entire night was growth party:

Yields resume uptrend

S&P well and truly outdid the Nasdaq. The latter is clinging to the broken neckline of its head and shoulders top:

Value, value, value! Oi, oi, oi!

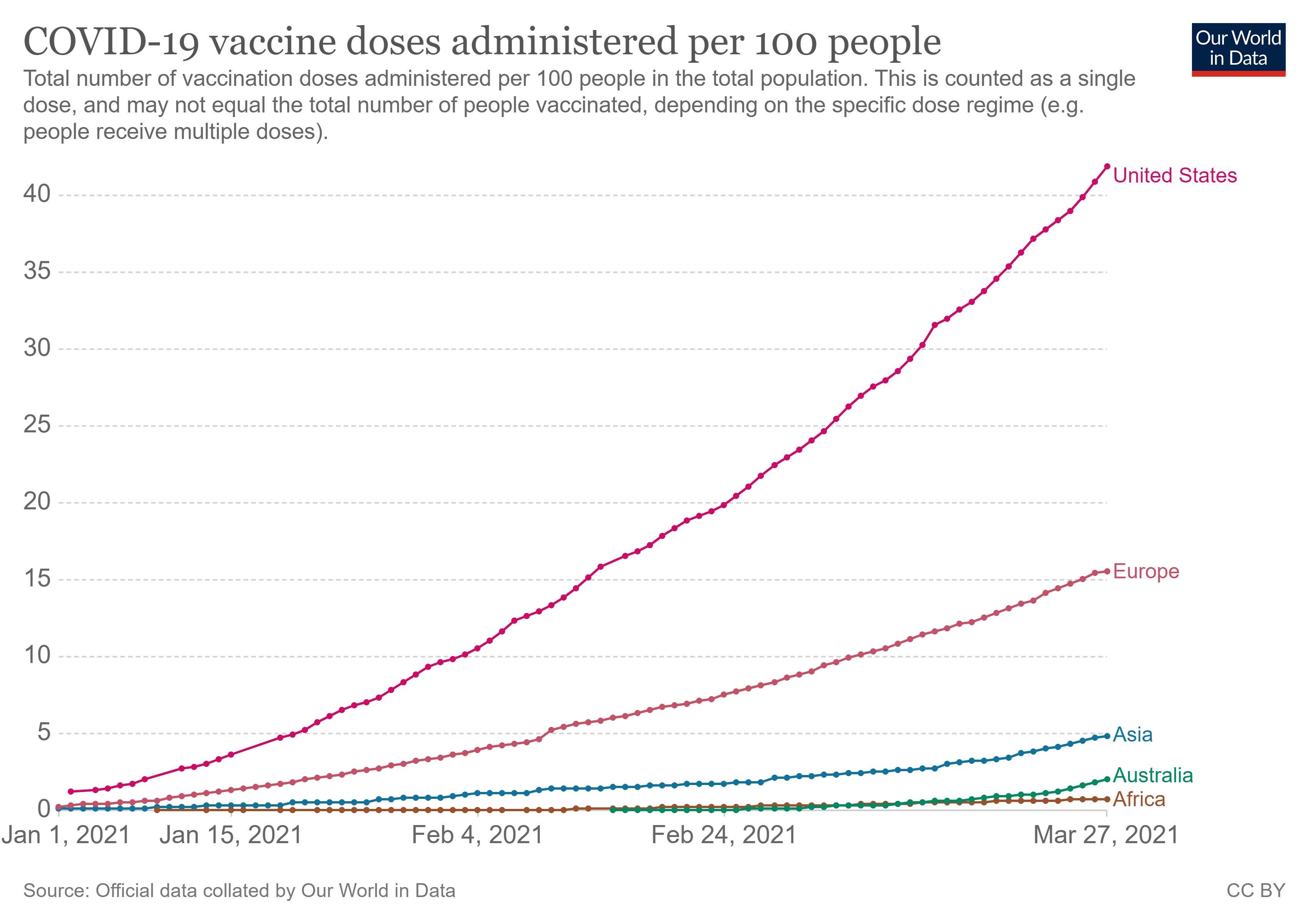

There is a reason to party about growth. The US vaccination drive is thumping along. Indeed, the Biden Administration has upped its 100 day vaccine target from 100m to 200m doses:

US exceptionalism accelerates

It is in a race with rebounding infections as lockdowns lift but nothing like Europe.

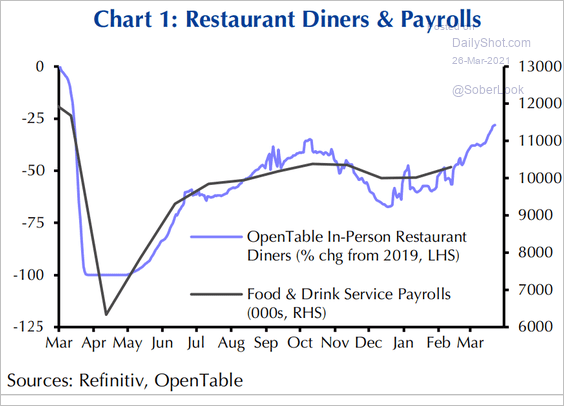

And virus sensitive areas of the economy are surging back:

Have vaccine, buy a fat steak.

Dragging up wider growth:

US growth up and away

The question remains, where will DXY go as this vaccine leadership stretches ahead? Europe is also accelerating its rollout but has a lot more hesitancy in the wake of its Astra Zeneca struggles (not to mention Australia and its new virus outbreak). Also, in the coming week, the Biden Administration infrastructure push will begin in earnest. Plus Friday brings the next US jobs report which ought to be a thumper.

I remain of the view that the path of least resistance for yields and DXY is a pain trade higher. This will likely continue to challenge growth stocks, EM flows, commodities and therefore the Australian dollar.