The Australian dollar is clinging grimly to the clifftop as last night the DXY rallied on and EUR fell:

The Australian dollar has backed away from the neckline of its monstrous head-and-shoulders top:

Yields kept piling higher:

Stocks are going exactly as expected with Nasdaq still deflating while value trades hold up wider bourses.

Expect more of the same as yields grind higher.

Credit Agricole has a decent wrap of where we are for forex:

The Australian economy has had a bit of a rough run the past week with floods hitting much of the East Coast and now a lockdown. These events will weigh no the March economic data due to out early April and potential muddy the water on the impact of the ending of the government’s JobKeeper program at the end of March. We note a few things, however. First, the floods have led to a rush on supermarkets for stockpiling, which will give retail sales data a bump in March. Second, Brisbane’s lockdown is for 3 days in a hope that the Easter tourism season will be able to be salvaged. Indeed, there are newswire reports of a rush on cancellations by tourists from Australia’s southern states. Queensland’s tourism-dependent economy was hoping for a bumper Easter to help repair some of the damage done over the past year and to help smooth the end of the government’s JobKeeper program, which had kept many people in the tourism industry in work. So, Wednesday and when the Queensland Premier will decide whether or not to extend the lockdown will be an important day for Queensland tourism. It is also worth noting that so far only Brisbane has been locked down and stronger magnates for tourism such as the Gold and Sunshine Coasts remain open.

Weekend residential property auctions broke records and Australian house prices were up by over 2% in February. But when APRA Chair, Wayne Byres, appeared before a parliamentary committee on Monday and was asked about what APRA could do about rising house prices, he said targeting house prices was not APRA’s job. Indeed, Byres pointed out that APRA’s job was to ensure financial system stability and so it was on the lookout for lackadaisical or imprudent lending by banks, which would lead APRA to re-introduce lending restrictions. But,Byers said there were no signs of such lending yet. Importantly,there has been an implicit assumption in the market that, like NZ, Australia would introduce some measures to curb strong house prices inflation and that this would give more room to the RBA to hold rates low for longer. No such help appears to be coming from APRA at the moment and so there will likely be some upward pressure on Australian rates and the AUD/NZD cross, especially if Brisbane’s lockdown is not extended.

Two key lessons from the recent FX market price action

Last week’s price action in the FX markets taught us two important lessons about the present and future FX impact of UST yields. The first is that the aggressiveness of the recent moves of UST yields is a more important market driver than their current levels. Indeed, we note that risk sentiment has recovered

and the USD rally has faded once the rebound in UST yields has lost its impetus in recent days. The observation further highlights a broader point that the reason for higher USD yields – the improving US and global growth outlook –is also an important support for the global stocks and commodity prices. We conclude that, so long as UST yields remain in a range or are not surging higher, risk assets could regain some ground. In turn, this could help commodity and risk-correlated G10 currencies consolidate in the near-term. The USD could hold up better versus low-yielding safe havens like the JPY, the CHF and the EUR, however.The second key lesson is that the UST yield levels will matter much more when investors start fretting about unwarranted tightening of the US and global financial conditions. We believe that this point could come at levels of 10Y UST yield closer to 2% where it will exceed significantly the current US stock market dividend yield. Indeed, recent history suggests that UST yield moves of such magnitude have tended to fuel stockmarket outflows and triggered spikes in risk aversion. We expect that the rise of UST yields will continue in Q2 with the risk of a more lasting and damaging surge in risk aversion growing as a result. We therefore remain in favour of buying USD dips over the more medium-term, expecting a renewed rebound in both UST yields and the currency incoming weeks.

Yep, a few points:

- A corrupt APRA will come in eventually and long before the RBA moves. Just not yet.

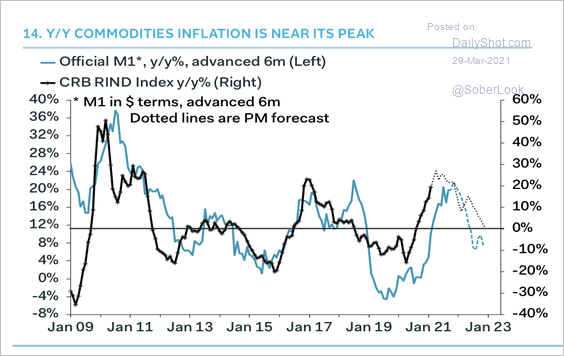

- The stalemate described for a strong DXY and strong AUD is about right but only for now. Ahead is the China slowing which will sink commodities:

Farewell supercycle. It was a good time not long time.

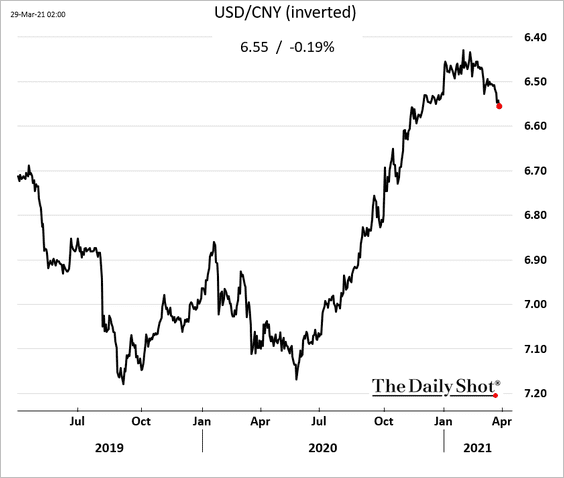

Which is already being signalled by a falling CNY:

CNY sagging

So, the stalemate won’t last long and means the next material move in forex is up for DXY and down for AUD.

The big question is, when it starts to come apart, will it be enough to trigger Fed easing as it was in 2015 and 2018? I still don’t think so given the powerful US fiscal tailwind will support growth and profits.

But, either way, the Australian dollar is in for more pain before the Fed is tested.