It was a good time but not a long time for tearaway tech stock Afterpay and its various clones. All of them boomed over the last year as COVID-19 launched anything tech-related to the moon.

But rising yields and the associated swing away from growth stocks and towards value has ended the party at a cliff. Yesterday it was a new closing low. Today it is new absolute lows, if only by a tick before a little rebound:

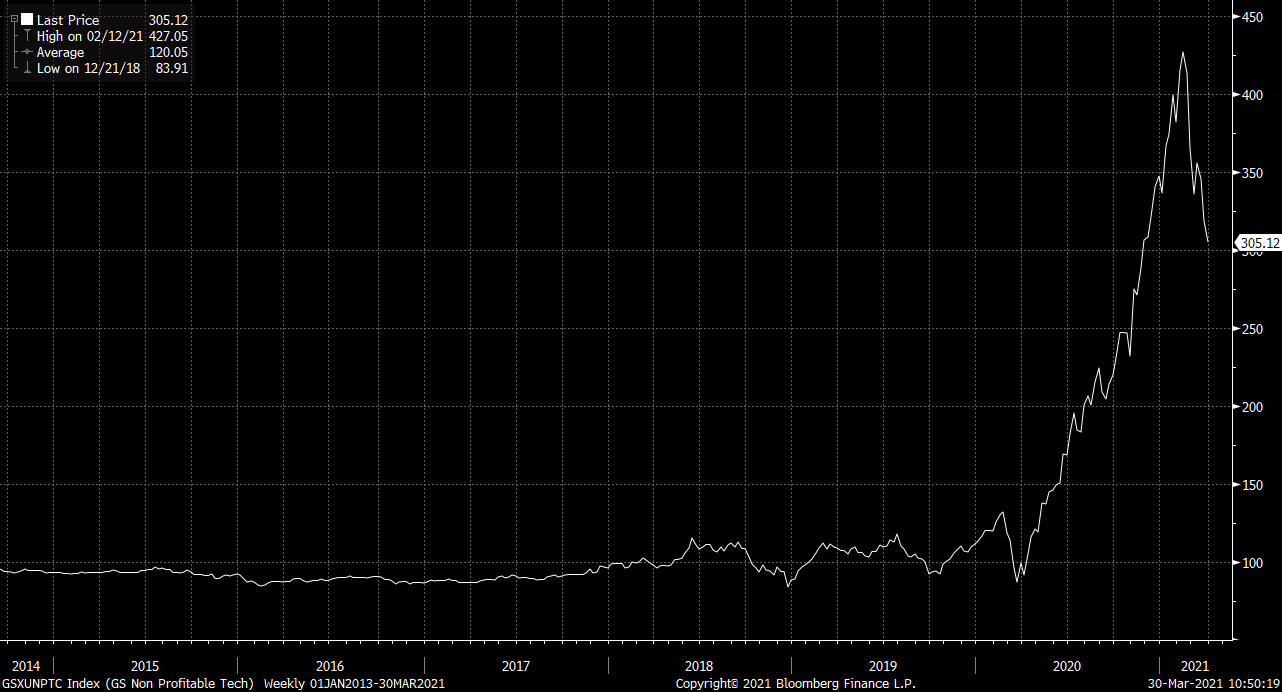

Bubble now, crash later

Given yields very likely have further to rise, growth stocks equally likely have further to fall. The path of “no earnings tech” stocks from Goldman is the worst bubble I have ever seen:

Millennial dills bubble

For those taking losses on BNPL, it is perhaps some small comfort that serious hedge funds and banks have also lost their shirts in the tech rout. The apparent losses of Archegos Capital, which have riled markets for a few days, are related given large holdings in Chinese tech giants. JPM has more:

With Nomura yesterday indicating a $2bn potential claim and Mitsubishi UFJ Securities Holdings announcement today of potential $300mn loss which for a likely non-material PB player is surprising to us – we now expect losses well beyond normal unwinding scenario for the industry: we see the losses as very material in relation to lending exposure for a business that is mark-to-market and holds liquid collateral. It makes Nomura indication of potentially losing $2bn and press speculation of CSG $3-4bn losses as not an unlikely outcome. In normal circumstances as we discussed in our note, we would have suspected industry losses of $2.5-5bn. We now suspect losses in the range of $5-10bn.

Archegoswas highly leveraged at5-8x (i.e. $50-80bnE of exposure for $10bn of equity) and the use of equity-swaps increased the inability of PBs to see the concentration risk in holdings within the hedge fund in question, in our view. We are still puzzled why CSG and Nomura have been unable to unwind all their positions at this point – as we would expect to get announcement as soon as this is the case, on the scale of potential losses (especially in the case of CSG which hasn’t provided numerical impact). We expect full disclosure by the end of the week at the latest from CSG and would keep an eye on credit agencies statements as well. We suspect potentially poor risk mgmt being an issue here considering i) late unwinding, and ii) possibly significant more leverage than for GS/MS similar exposures.

The driver of tech stock deflation likely has months to run. The margin call has begun. Tread very carefully.