The Australian property market is clearly on a tear, growing at a double-digit annualised pace on the back of rock-bottom mortgage rates and unprecedented government stimulus.

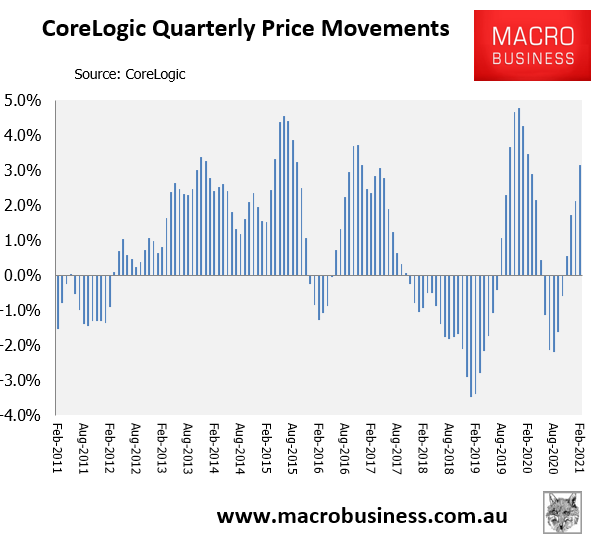

On the one hand, a property price boom in Australia is nothing unusual, given Australia has experienced several similar episodes over the past decade, as illustrated clearly in the next chart:

However, according to Fairfax’s Clancy Yates, there are some major differences this time around compared to previous property booms, namely:

- the price boom is being driven by owner-occupiers, rather than investors; and

- the boom is occurring amidst negative net overseas migration (NOM) and the slowest rate of population growth since World War 1.

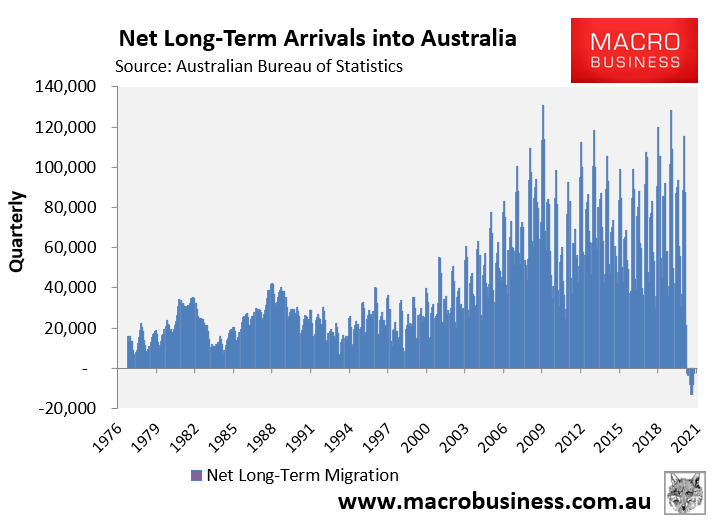

On both counts, Yates is correct. Net long-term arrivals into Australia – a proxy for NOM – has turned negative for the first time in data dating back to 1976:

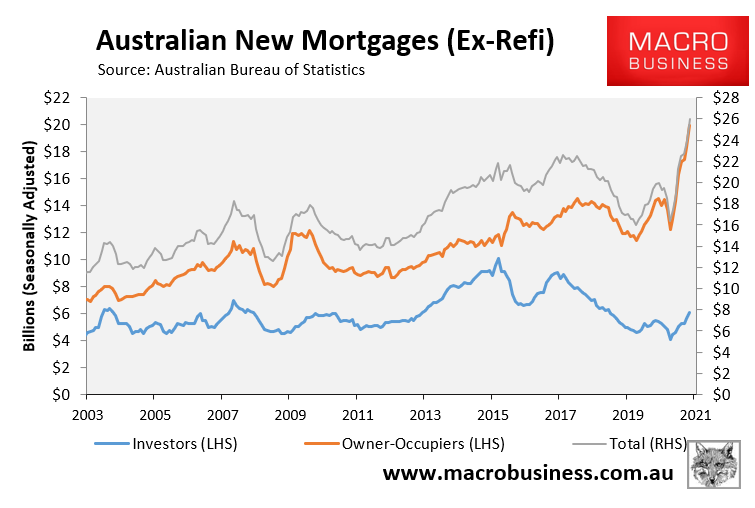

The Australian Bureau of Statistics’ lending data also shows that new owner-occupier mortgage commitments have surged to record high levels, whereas new investor mortgage commitments remain well below their 2015 highs:

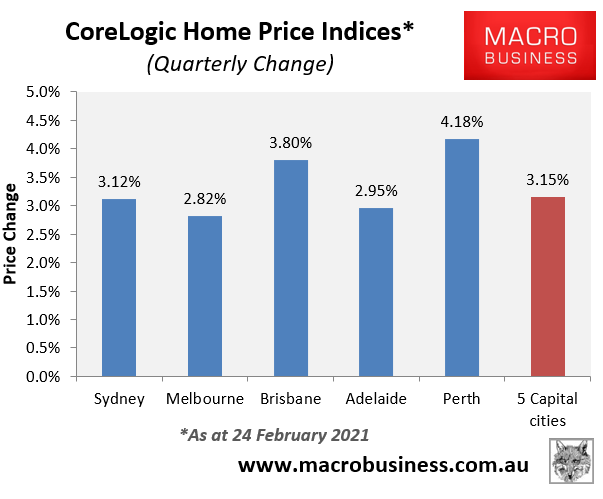

Another difference this time around is that the boom in dwelling prices is being led by the smaller major capital cities of Perth and Brisbane. This is a stark contrast from recent booms, which were driven overwhelmingly by Sydney and Melbourne:

Obviously, Sydney and Melbourne are far more reliant on mass immigration, especially with respect to the inner-city apartments, which is likely weighing on their growth.

Regardless, this current property price boom has a different flavour to past episodes, due to the factors outlined above.