Real estate parasites demand tax deductible mortgages

For the rent-seekers in the property industry, no amount of taxpayer subsidies or interest rate cuts are ever enough.

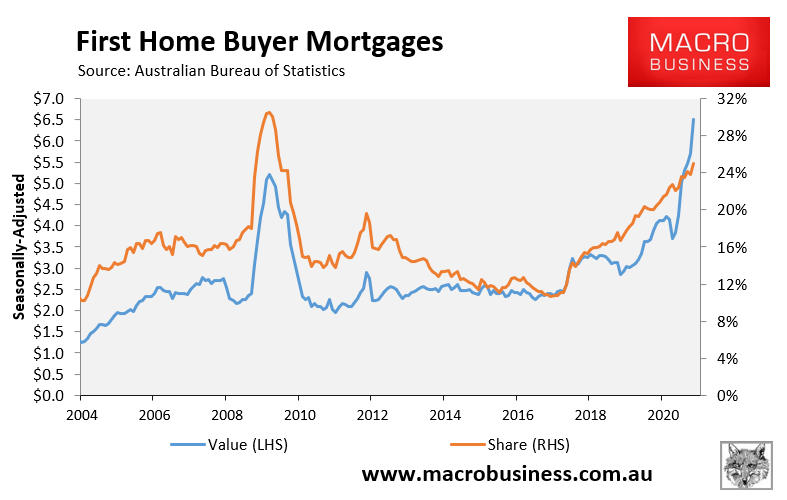

Despite the Australian property market defying the COVID-19 downturn thanks to massive taxpayer stimulus and RBA intervention in the mortgage market, which has driven first home buyer (FHB) demand to new highs:

The Real Estate Institute of Australia (REIA) has used its pre-Budget submission to call for interest payments on mortgages to be made tax-deductible for first-time buyers:

REIA President Adrian Kelly said there was a need for policies and investments that would continue to drive growth in the property market, and help property market players as Australia emerges from the pandemic.

“Wherever you are in the housing market, an agent, tenant, buyer, investor or vendor, there should be support for you in the next federal budget to have confidence to succeed in a COVID-normal Australia.”

“REIA estimates (making the interest portion of mortgage payments tax-deductible) would provide a benefit of around $4000 per annum to Australia’s first home buyers, which NHFIC places at around 15 per cent of the housing spectrum,” Mr Kelly said.

“At least six other OECD nations have a similar incentive.”

When a similar scheme was proposed four years ago, the Grattan Institute warned that it would cost the Budget $19 billion a year:

The Grattan Institute’s chief executive, John Daley, told Guardian Australia the deduction would cost the budget $19bn a year and do little to improve housing affordability…

A University of New South Wales economist, Nigel Stapledon, told Guardian Australia the cost to the budget would be “pretty substantial”.

Any demand-side stimulus like this would also be entirely self-defeating from a housing affordability perspective. Past experience has shown us unequivocally that such measures do not work.

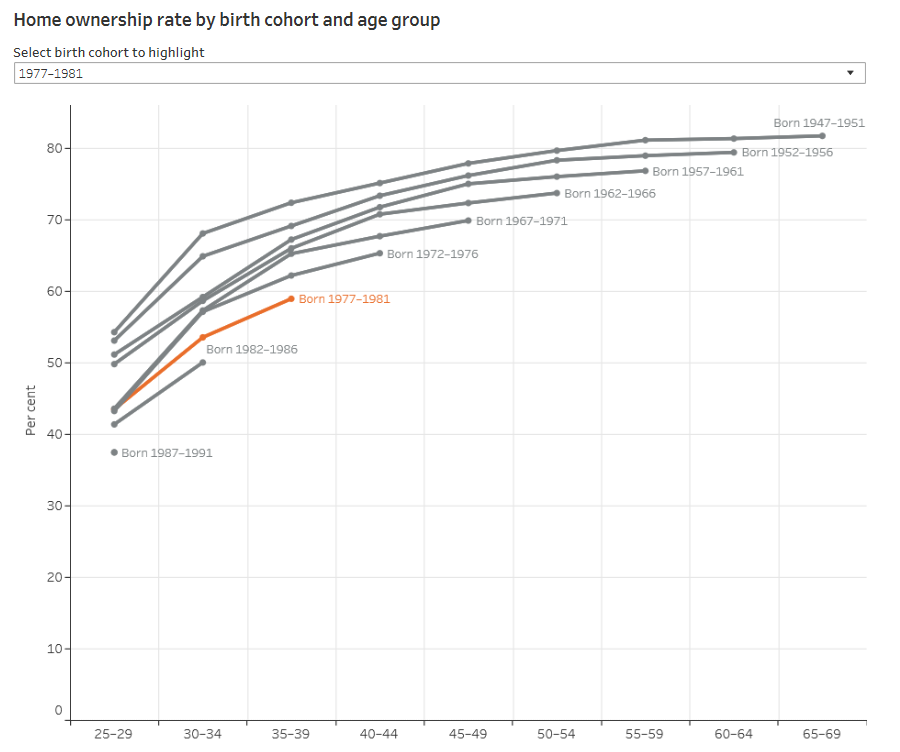

Despite the massive decline in mortgage rates and the myriad of subsidies provided to home buyers over the years, the home ownership rate has decreased, particularly for younger Australians (see next chart).

Allowing buyers to claim a tax deduction on their owner-occupied mortgage would simply increase their capacity to pay and would soon be capitalised into higher home prices. At the same time, the Budget deficit would be expanded considerably for no benefit.

If you said to me five years ago that the Coalition Government would consider making owner-occupied mortgages tax deductible, I would have laughed at you. But after witnessing their antics over recent years – defending negative gearing and the capital gains tax discount, axing responsible mortgage lending rules, and implementing massive buyer subsidies – I certainly would not rule-out the Coalition introducing such a measure. They could try anything to support the housing bubble.

We are the property equivalent of a narco state, after all, where the property and banking industries pull the strings.