The RBA has been very explicit about why it has renovated its entire monetary policy framework. Its inflation goals have fallen short for a decade. One major reason why was monetary policy was too tight leading to an overly high Australian dollar. Yesterday at Bloomberg, Westpac’s Sean Callow declared:

“The conversation around the Aussie changes when you leave the 70s. The RBA might be dismayed by the break of 0.80 but given the commodity price backing is so strong, they should take some comfort that the A$ doesn’t seem overvalued. It’s a headwind, but they saw worse in 2011-12.

This is the wrong way to think about it. The RBA will not take comfort from a failed past. An Australian dollar above 80 cents today bears no relation to it doing so in 2011/12.

High commodity prices typically lift Australian activity via three channels: higher wages from investment, lower taxes from bigger budget receipts, and stock market gains. All three were going gangbusters in 2011/12. Only the last is intact now.

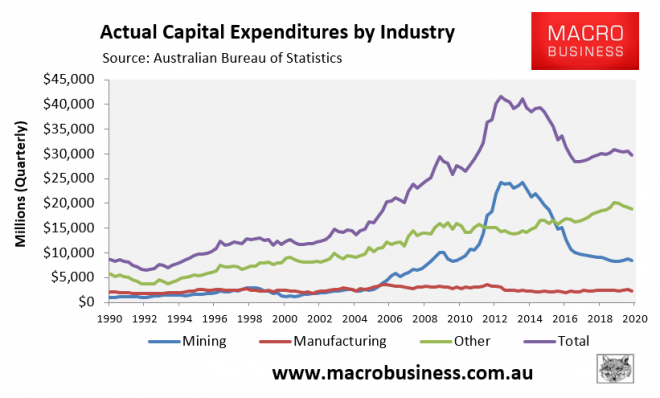

The mining investment boom is bust and is not coming back so there is no transmission to wages and demand:

In 2011/12, tax rates were much lower. Today they are rising with further fiscal consolidation ahead. Via Minack and Associates:

The stock market returns are still looking good but the growth over a decade is pretty lousy and it was always the smallest of the three channels:

As well, in 2010/11, the RBA had numerous drivers running in the economy with house prices also hot. Today, that is all that it has. And it has macroprudential policy tools today that it did not have in 2011/12 so it will be very comfortable that it can tighten on that sector without rate hikes if need be.

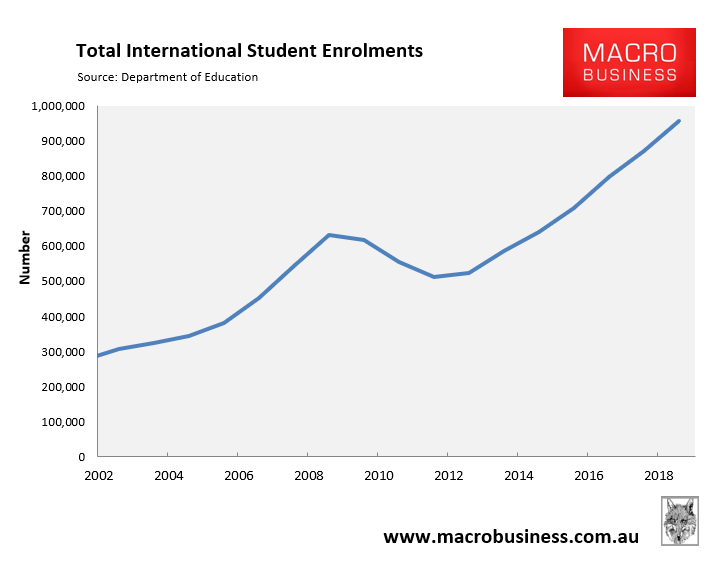

Finally, in 2011/12, Australia was still hell-bent on selling everything not tied down to a developing China. Today we confront some degree of decoupling from the Chinese economy, including very probably the international student trade which played a key role in delivering growth after 2011/12. 80 cents is the killer point for that sector’s competitiveness:

In short, the RBA will be very unhappy with an Australian dollar above 80 cents regardless of the high terms of trade. The bank has renovated its reaction function for all of the above reasons and it will be triggered if it needs to be. There is still oodles of scope for the RBA to expand QE:

In short, regardless of high terms of trade, the Australian dollar above 80 cents will smash Australian inflation and the RBA won’t get angry with AUD bulls, it will get even.