Superannuation Minister Jane Hume has recently stated that super funds should be forced to offer new retirement income products so that retirees use more of their super rather than save it.

According to The AFR, Treasurer Josh Frydenberg will echo these comments when he speaks to a retirement income forum today, saying that people should be encouraged to use their super more effectively.

Such comments by Hume and Frydenberg are seen as backing the push by backbench government MPs and the business community to revoke the legislated increase in the superannuation guarantee (SG) from 9.5% to 12% by 2025.

The Australian Treasury’s Retirement Income Review noted that superannuants have been reluctant to draw down their savings, instead relying solely on their investment returns to fund their retirements. This, in turn, has turned Australia’s superannuation system into a wealth accumulation and transfer scheme that has increased inequality:

Advertisement

Inheritances are significant, representing the transfer of wealth from one generation to another. They are not distributed equally and increase inequity within the generation that receives the bequests. Most people die with the majority of wealth they had when they retired. If this does not change, as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances. Superannuation is intended to fund living standards of retirees, not to accumulate wealth to pass to future generations…

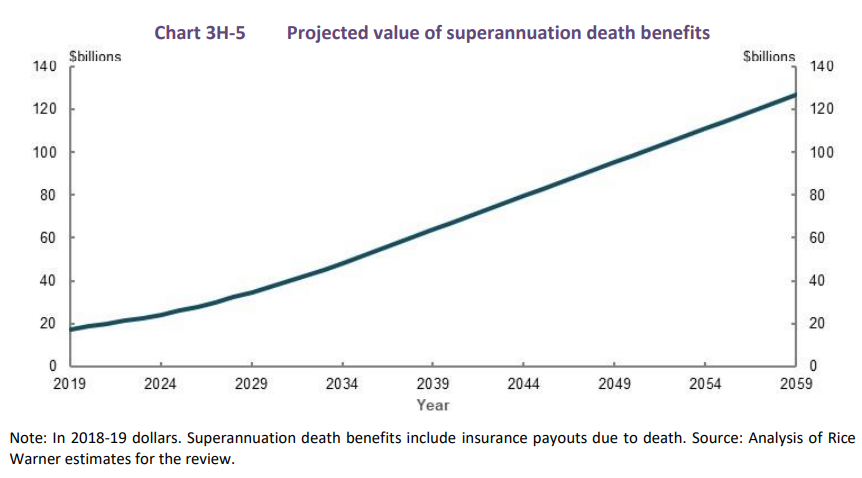

For example, assuming no change in how retirees draw down their superannuation balances, superannuation death benefits are projected to increase from around $17 billion in 2019 to just under $130 billion in 2059 (Chart 3H-5)…

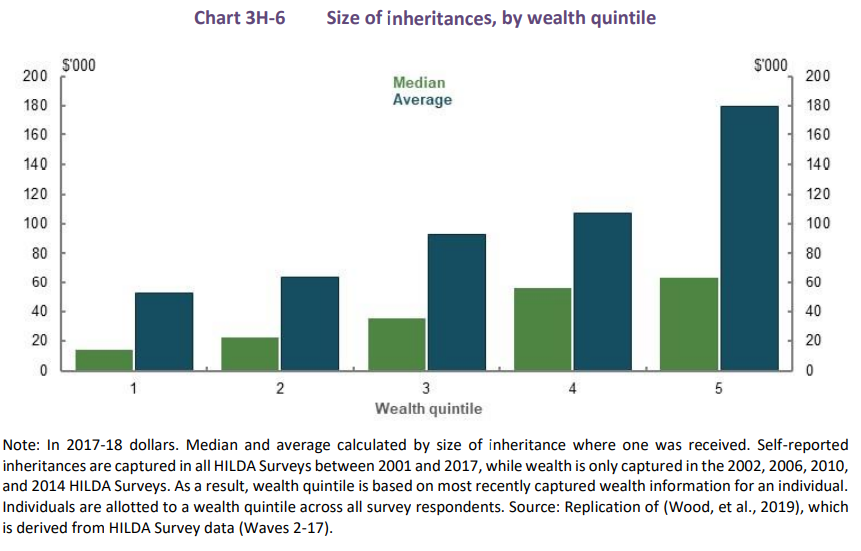

Although inheritances can help people to prepare for retirement, they are distributed unequally, with wealthier people tending to receive larger inheritances than those with lower wealth (Chart 3H6). Inheritances therefore increase intragenerational inequity…

Super nest eggs were never meant to be preserved in order to pass onto one’s heirs after death. They are supposed to be drawn-down to fund one’s retirement.

Consider, for example, a new retiree with superannuation savings of $500,000 earning a return of 5% annually (i.e. a combination of interest and dividends).

Advertisement

If this retiree relies only on investment returns to fund their retirement, they would receive $25,000 a year in income (i.e. 5% times $500,000). However, if principal is also drawn down, then $38,200 would be available over 20 years to fund their retirement.

Put simply, retirees must be made to draw-down their superannuation savings. This is a far more equitable and cheaper option than lifting the SG from its current level of 9.5%.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.