CoreLogic has released its Housing Market Update Report for February, which provides a bunch of key data pertaining to Australia’s property market.

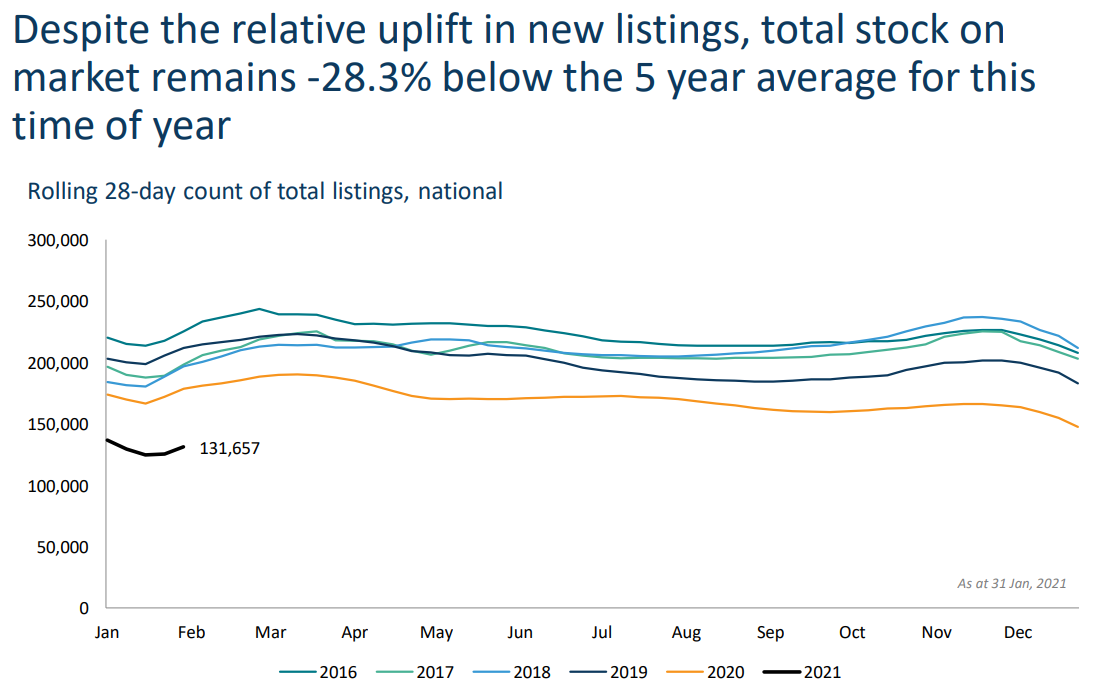

What sticks out most in this month’s report is the lack of homes listed for sale, which is tracking around 28% below the five year average:

As shown above, there were only 131,657 home available for sale across Australia in February 2021, way down on an average of around 200,000 homes for sale during the same month between 2016 and 2020.

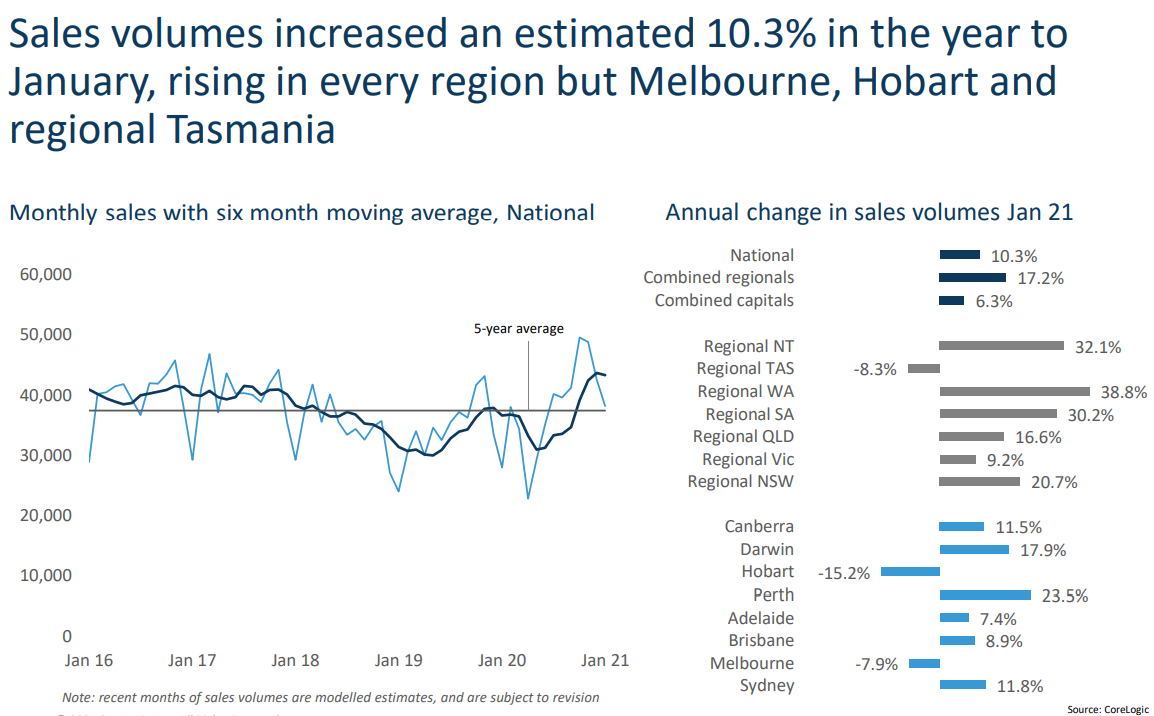

At the same time as stock levels have cratered, actual demand as measured by sales is tracking around 10% higher than January 2020 and well above the five-year average in trend terms:

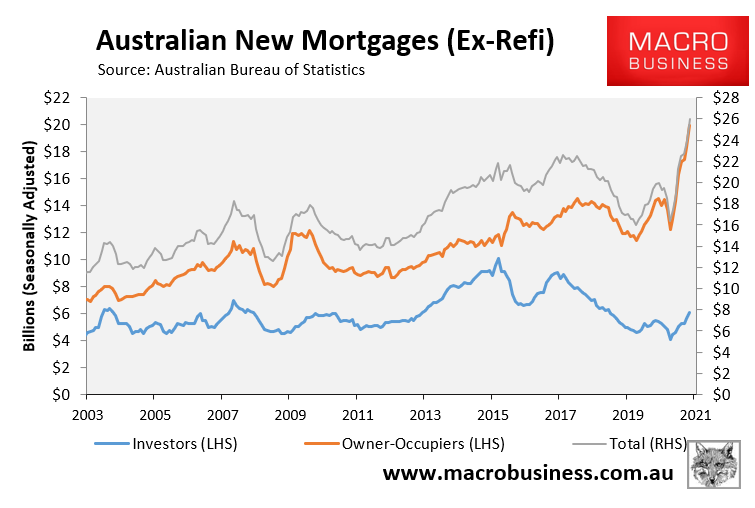

This surge in demand is also reflected in new mortgage growth, which has soared to unprecedented levels:

Clearly, strong buyer demand coupled with the dearth of available supply is behind the rapid property price growth being experienced across Australia.