Here’s a measure of just how dovish Australia’s interest rate circumstances are right now. The perpetually hawkish Shadow RBA is also dovish:

Signs of improvement but Shadow Board confident rates need to stay low

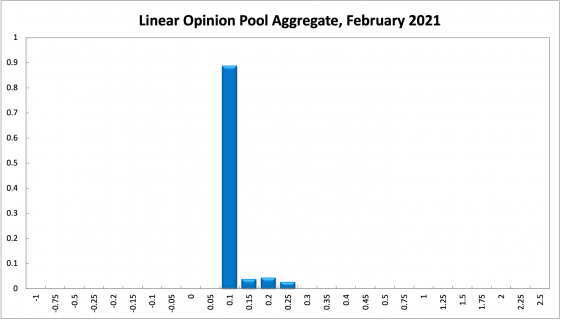

Apart from some isolated hotspots, Australia’s policy of containing the coronavirus remains very successful, certainly by international comparison, and the economy should continue to reap the benefits of this normalisation. The inflation rate ticked up in the December quarter, from 0.7% year-on-year to 0.9%, based on the latest ABS CPI estimate, but remains well below the RBA’s official target band of 2-3%. In spite of recent improvements in economic data, the RBA Shadow Board’s conviction that the cash rate should remain at the historically low rate of 0.1% is strengthening further. The Board attaches an 89% probability that this is the appropriate interest rate setting, while it attaches an 11% probability that a rate hike is appropriate and a 0% probability that a rate cut to below 0.1% is appropriate.

Labour market data since the end of Victoria’s 100-day Covid-19 lockdown has been positive. The official ABS unemployment rate peaked in October at 7% and has fallen in the two subsequent months to 6.6%. Overall employment rose by 50,000 in December, the majority of which is full-time. Youth unemployment also fell, from 15.6% to 13.9%, job advertisements are up and the labour force participation rate edged up to 66.2%. So far, the unwinding of Jobkeeper assistance has not appeared to hurt the labour market, a reflection of the relative strength of the Australian economy and the success in containing the Covid-19 pandemic.