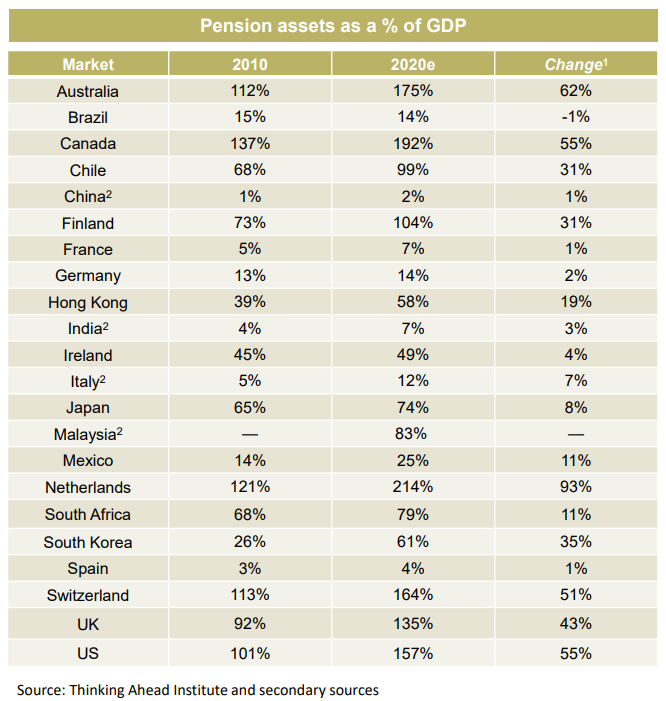

A new study by the global Thinking Ahead Institute has ranked Australia’s compulsory superannuation system the world’s most successful following 11.3% compound growth in assets under management over the 20 years to 2020:

The most successful pensions market can be found in Australia, featuring 20-year pension asset growth of 11.3% per annum, in USD terms. The critical features in this success have been government-mandated pension contributions, a competitive institutional model and the dominance of DC [Defined Constribution].

This strong growth has lifted the value of Australia’s assets under management from 112% of GDP in 2010 to an estimated 175% of GDP in 2020:

I don’t put much weight in this “most successful” claim. The primary reason why Australia’s superannuation assets have grown so strongly is that the federal government mandates that workers must put 9.5% of their wages/salaries into superannuation.

If the federal government mandated that workers purchase a massage every week, then Australia would very likely have the “most successful” massage industry in the world as well.

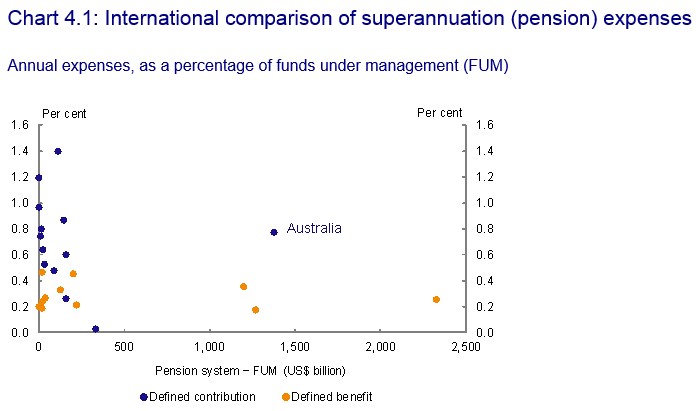

A better way to examine the efficiency of Australia’s superannuation system is to look at fees. Here, Australia’s compulsory superannuation system compares poorly against other nations with management fees among the very highest in the world despite having one of the biggest pools of assets under management:

Hence, Australia’s superannuation system defies the notion of ‘economies of scale’. As superannuation assets have grown, management fees should shrunken proportionately.

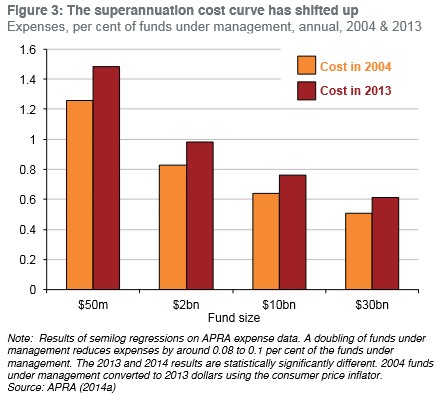

To add further insult to injury, the Grattan Institute has illustrated that Australia’s compulsory superannuation system has become less efficient as it has ballooned in size:

The end result is that Australian households are being gouged with fees, paying twice as much in super management fees than they spend on electricity every year.

In short, the ever-growing honey pot of fees available under Australia’s compulsory super system has created a giant parasitic industry.

If there’s one thing Australia’s superannuation system is world’s “most successful” at, it is milking workers for fees.