While the Australian property market as whole is on a tear, reporting strong growth across all major markets and regional areas, there are pockets where rents are going backwards and present great risks to budding property investors.

In particular, high-rise apartments across Sydney and Melbourne are suffering from a strong supply response that has run head long into collapsing student and migrant demand arising from Australia’s international border closure.

The latest Domain data is a case in point, recording heavy falls in apartment rents in these two cities, driven by their respective CBDs:

Unit prices in the harbour city edged up 0.2 per cent while asking unit rents fell 5.1 per cent.

The trend is pronounced among the high-rise apartments of the Sydney CBD, where unit prices are 6.5 per cent higher than a year ago while unit rents dropped some 20 per cent…

Melbourne showed a similar pattern, with quarterly house price growth (up 5.3 per cent) outstripping house rents (unchanged), and unit price growth (up 4.4 per cent) outpacing unit rents (down 3 per cent).

Melbourne CBD unit prices held steady over the past year despite unit rents falling 27.3 per cent.

Indeed, James Kirby believes that poor apartment rents across Sydney and Melbourne are “the new risk for property investors”:

The major issue is the weakness in apartments markets which are traditionally the “entry point” for many investors…

The hollowing out of the student accommodation market is plain to see. Scape, the country’s biggest student accommodation provider, is reporting occupancy rates of just 15 per cent in its key buildings.

Similarly, prices in the suburbs that neighbour student hubs are facing a very tough road ahead…

As Shane Oliver, chief economist at AMP Capital, put it: “Demand for housing is likely to be around 300,000 dwellings lower than otherwise would have been the case out to mid-2022.”

Rental income is now the outstanding risk for investors returning to the property market.

To be fair, rental income is only “the outstanding risk for investors” with regards to Sydney’s and Melbourne’s apartment market. As shown in the next chart from CoreLogic, the rental yields on offer in both of these markets is well below the national average and apartment rents are falling fast:

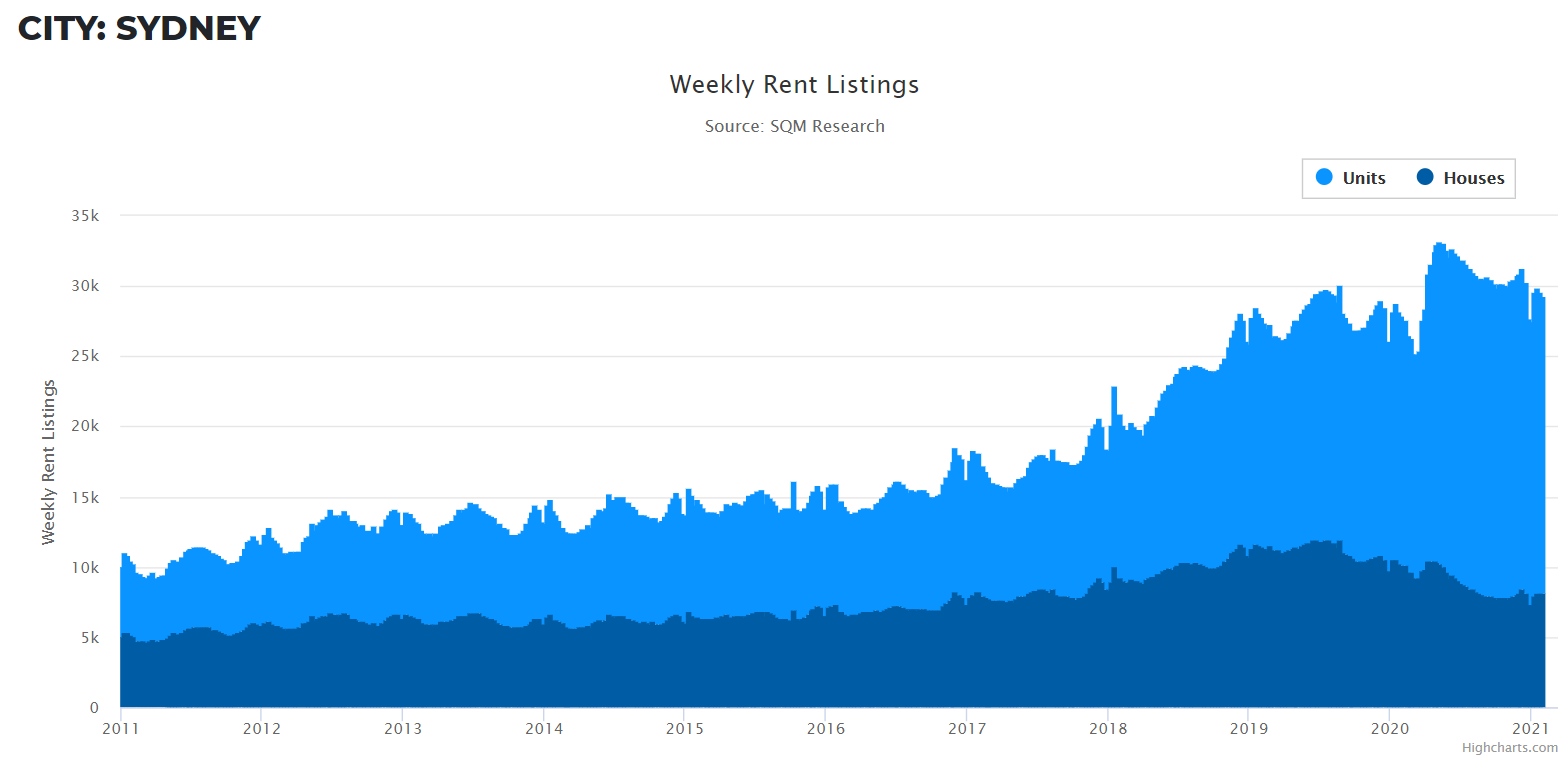

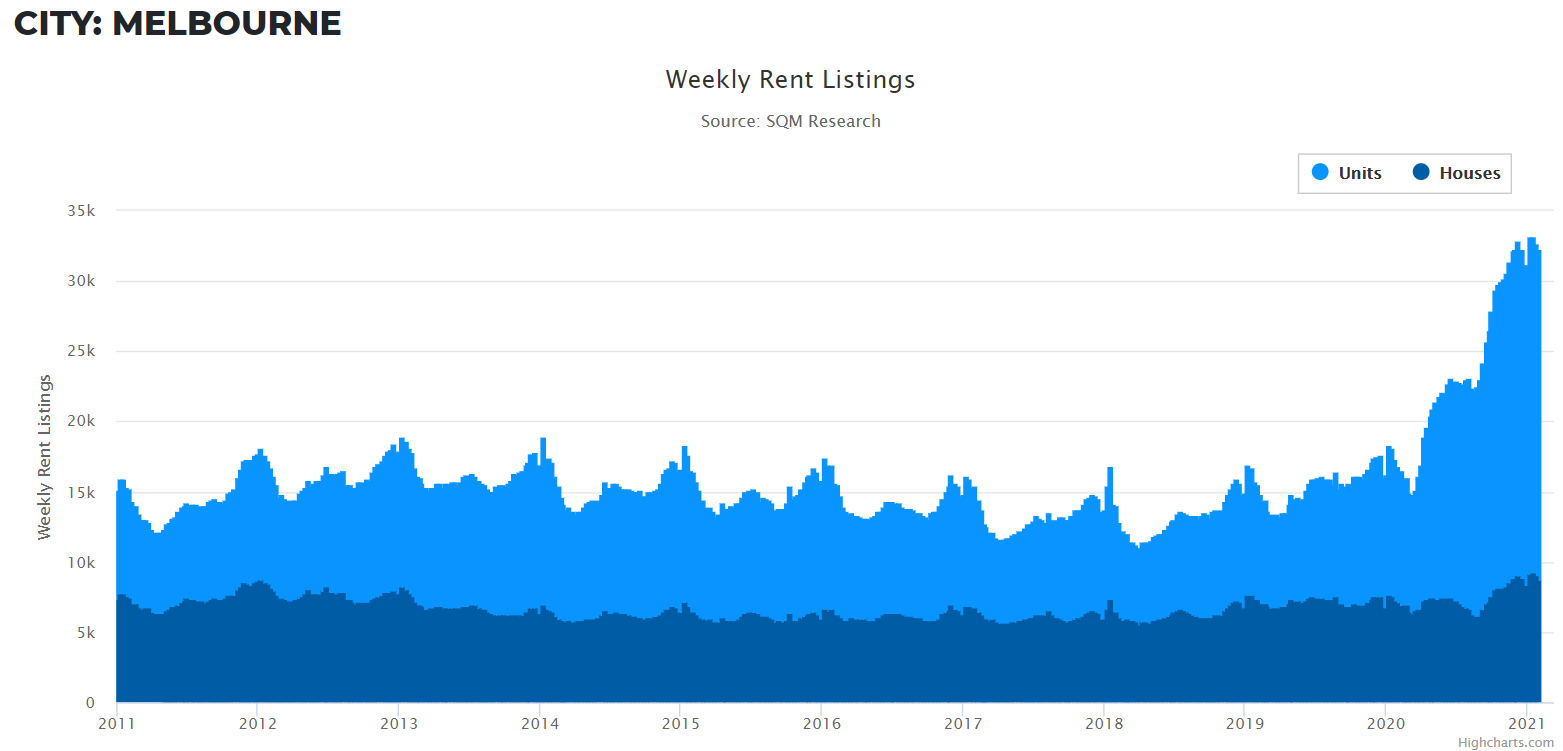

This decline in rents across Sydney and Melbourne apartments reflects the massive oversupply of stock, as illustrated in the below data from SQM Research.

According to SQM, Sydney had 21,142 units (apartments) available for rent on 1 February, more than double the number of houses available for rent (8,193):

The situation in Melbourne is even worse, with 23,505 units (apartments) available for rent on 1 February, nearly triple the number of houses available for rent (8,794):

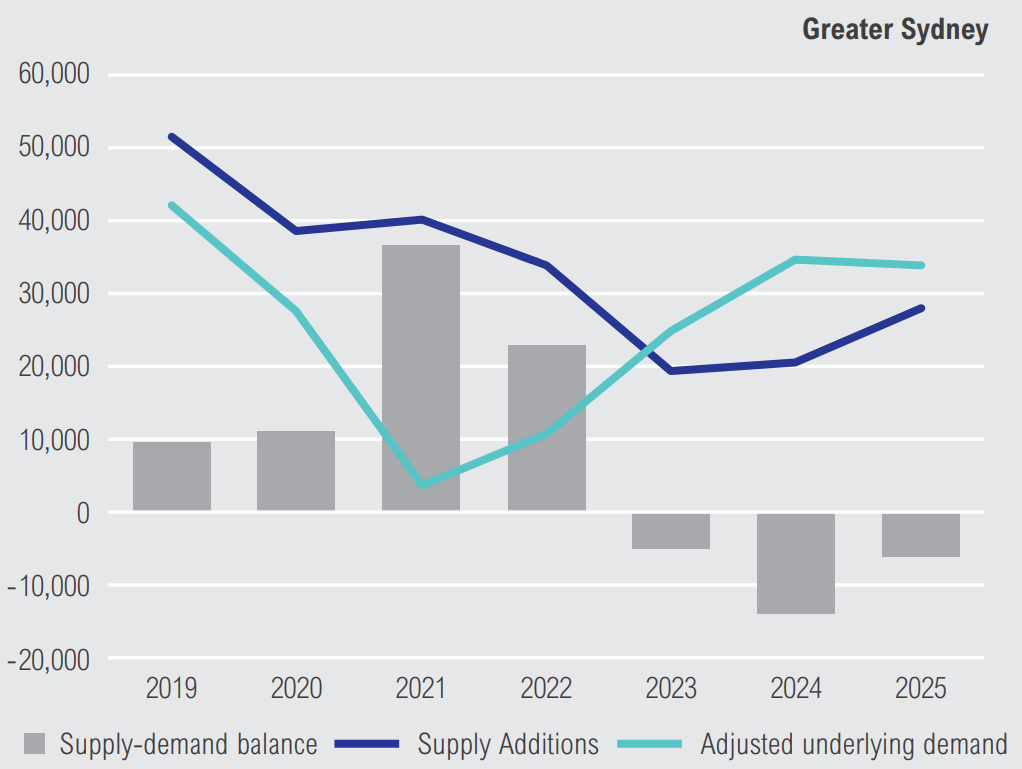

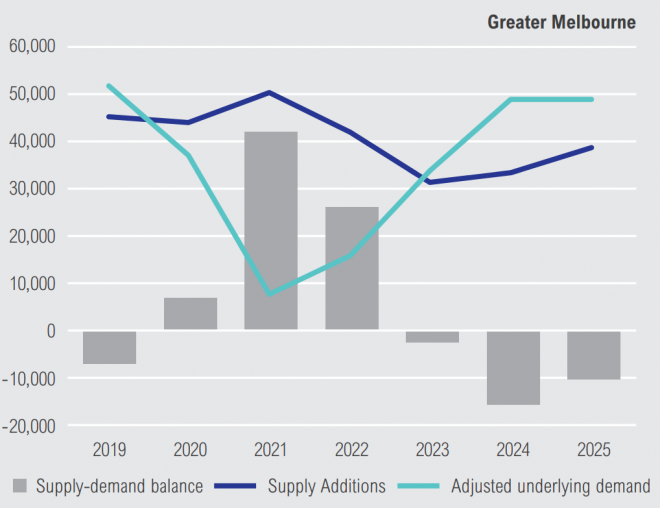

The oversupply of apartments is forecast to worsen in the next two years across Sydney and Melbourne, according to projections from the National Housing Finance Investment Corporation (NHFIC):

Again, this projection is mainly the result of the expected collapse in immigration, which will hit Sydney and Melbourne the hardest.

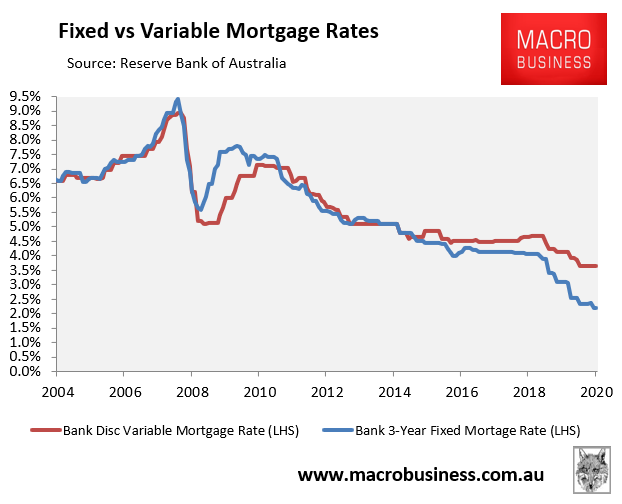

So while the cratering of mortgage rates (especially fixed) has made Australian property a good bet overall from an investment perspective:

Sydney and Melbourne apartments are obviously the exception, given they are being hit hardest by the collapse in immigration, as well as suffering from years of strong apartment construction.