By Gareth Aird, head of Australian economics at CBA:

Key Points

- Momentum in the Australian property market has surged and leading indicators point to strong price rises.

- We expect national dwelling prices to rise by 8% in 2021 and 6% in 2022 – the risks are tilted towards stronger outcomes.

- Price rises are expected to be greater for houses than units.

Overview

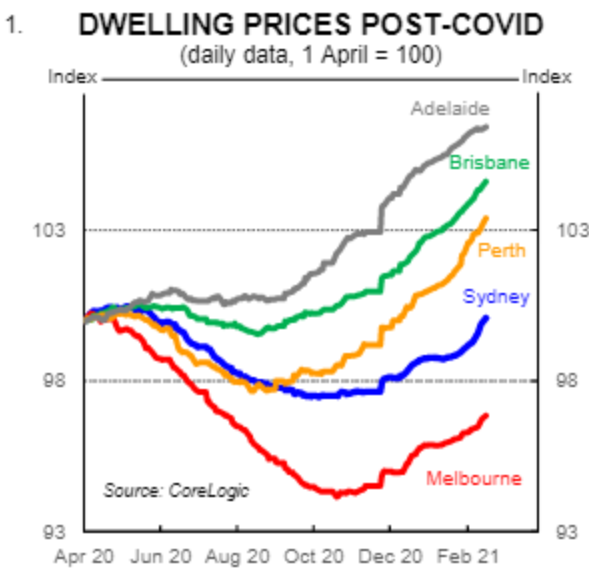

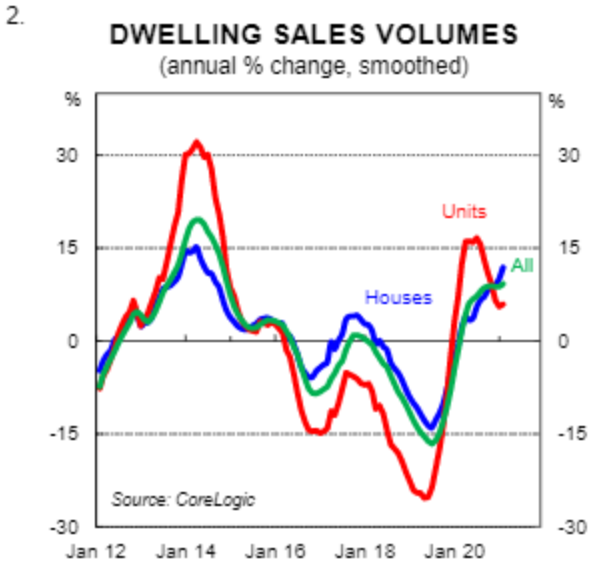

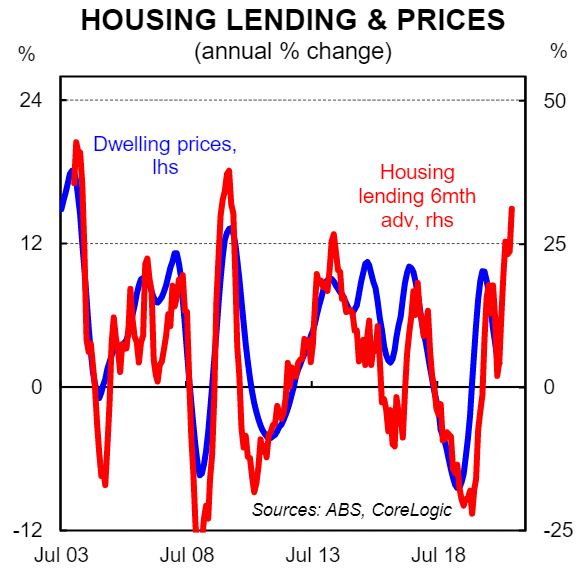

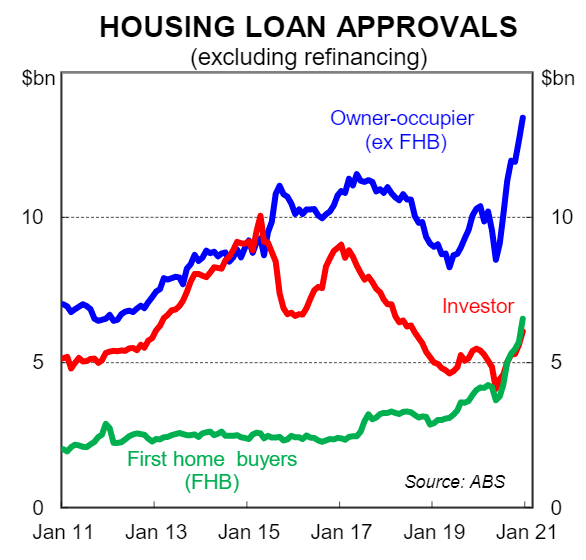

The Australian housing market is on the cusp of a boom. New lending has lifted sharply. Dwelling prices are rising briskly in most capital cities. And turnover is up significantly on year ago levels (charts 1 & 2).

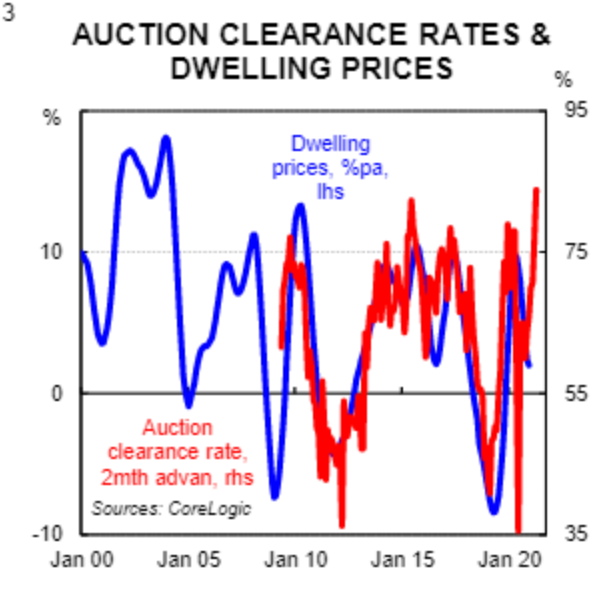

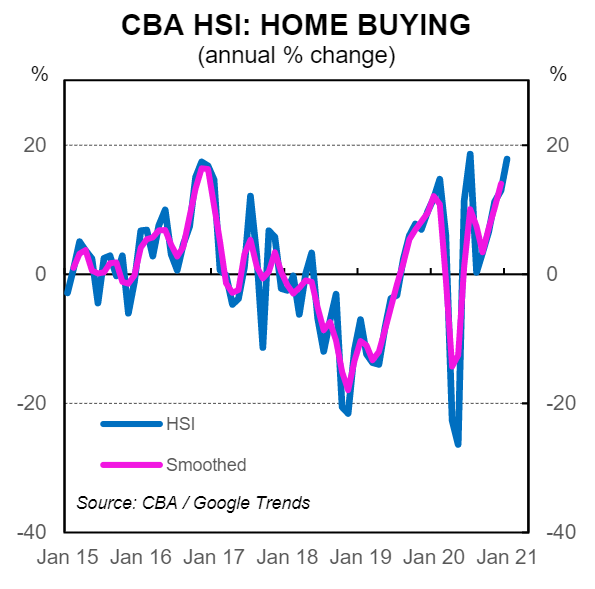

Near term indicators of momentum suggest conditions will further strengthen. Auction clearance rates are sitting at levels consistent with double-digit dwelling price growth (chart 3). And both the CBA home buying measure in our Household Spending Intentions series and the house price expectations index from the WBC/MI Consumer Sentiment survey have surged.

In many respects it’s a simple story. The boom is being driven by record low mortgage rates coupled with a V-shaped recovery in the labour market. Borrowing rates, which are the single biggest driver of prices in the short run, remain below the rental yield in most markets across Australia. This is an unusual situation and means that property markets across the country need to find an equilibrium. For the bulk of Australia, equilibrium will be achieved via further dwelling price rises.

We expect strong growth in national dwelling prices of ~14% over the next two years (8 capital city basis). A critical assumption underpinning our forecasts is the cash rate remaining at its record low of 0.1%,which is in line with RBA forward guidance. We do, however, factor in a modest increase in fixed rate mortgages, which will rise if the RBA removes or raises its target yield on the 3yr Australian Government bond, as we expect in the second half of 2021.

Our forecast profile is centred on prices growth of 8% in 2021 and 6% in 2022. The risks are skewed towards stronger outcomes given the strength of the demand impulse from the reduction in mortgage rates over 2020 (note that is it the percentage change in interest rates that has the greater impact on dwelling prices as opposed to the percentage point change in interest rates). There will be significant variation across the capital cities, as is always the case.

In a less common occurrence, we expect a disparity between prices growth for houses compared to apartments. We forecast national house prices to rise by ~16% over the next two years and unit prices to rise by ~9%. This note outlines our views on dwelling prices, our underpinning assumptions and the risks to our forecasts.

Recent story

The negative impact that COVID-19 had on Australian property prices turned out to be much more muted than almost any forecaster expected, us included. We were earlier than most, however, to recognise this and revised our call in September 2020 to look for a smaller peak-to-trough fall and a decent lift in prices over 2021. But even then, the rapid growth in new lending over the second half of 2020 was stronger than we anticipated. The increase in new lending is now feeding into higher prices for bricks and mortar.

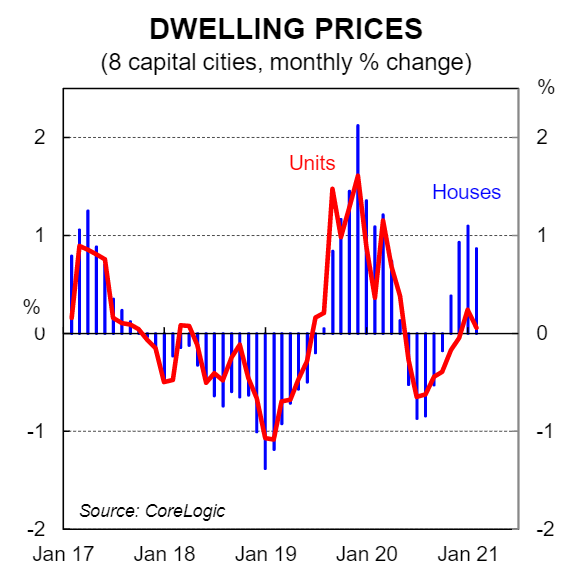

Dwelling prices have risen across all capital cities over the past three months (November 2020 to January 2021). And house prices have risen a lot faster than unit prices over that period (chart 4). The early data so far in February indicates prices growth has accelerated. At the time of publication the CoreLogic 5 capital city aggregate daily index has risen by 0.8% over the first two weeks of February. This points to monthly growth in dwelling prices of ~1.6% in February. It is clear that a firm uptrend in prices is underway and the factors which drive price outcomes over the short run are all pulling in the same direction.

New lending has surged

The flow of credit (i.e. new lending) has a clear impact on dwelling prices. More specifically, the annual change in the flow of credit has a close leading relationship with the annual change in dwelling prices by around six months (chart 5).

New lending is driven by the supply and demand for credit. And the price of credit is defined by mortgage rates, which sit at record lows. The latest official ABS lending data indicates that new lending has rocketed higher over the past six months (chart6). Our internal data paints a similar picture. Initially the lift in new lending was driven by owner-occupiers, including a big lift in lending to first home buyers. But more recently lending to investors has also accelerated (chart 7).

The effect of lower interest rates on the housing market is three-fold: (i) lower interest rates essentially mean that for a given level of income a borrower can service a bigger mortgage, all else equal; (ii) lower interest rates mean that the rental yield an investor is willing to accept is lowered; and (iii) lower interest rates shift the relative attractiveness of renting versus home ownership, all else equal. It is reasonable to assume that the RBA’s forward based guidance on the cash rate is having a stimulatory impact on the demand for credit. Over the latter part of 2020 the RBA regularly stated that, “the Board is not expecting to increase the cash rate for at least three years”. At the February 2021 Board meeting “at least three years” had shifted to “2024 at the earliest”.

Momentum is strong

Like all asset markets, there is clearly a momentum to the property market. It is often the case that both owner-occupiers and investors wait until they see a positive momentum in the market before they transact. This of course creates a self-fulfilling dynamic – as the market firms, would-be buyers are more confident to purchase and this brings other buyers into the market. Price rises are the inevitable outcome and this creates a positive feedback loop that can continue for an extended period, particularly in an RBA easing cycle, until there is a circuit breaker (e.g. interest rate hikes, macro-prudential tightening, a negative economic shock) or general fatigue.

And over the past four months the key indicators of momentum that we monitor have all strengthened. Our CBA home buying measure in our Household Spending Intentions series, for example, has powered higher in recent months. The strength in momentum will manifest itself in higher price outcomes and it is now simply a question of how fast prices rise and over what period.

How far and fast will prices rise?

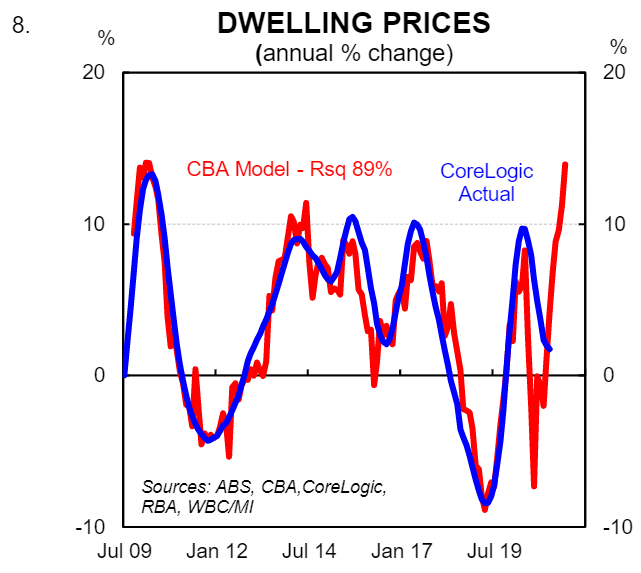

As a starting point for price outcomes in the near term we have input the latest leading indicators of the property market into our proprietary model. Our model puts the annual change in national dwelling prices as a function of the annual change in mortgage rates, the annual change in the flow of credit, auction clearance rates and the house price expectations index from the WBC/MI Consumer Sentiment survey, with varied lags. A literal read of our model implies that prices will rocket higher(chart 8). But all models have limitations and we believe that falling rents due to rising vacancy rates in some markets -notably the Sydney and Melbourne apartment markets – will temper the price outcomes that our model is signalling.

Notwithstanding, price outcomes are still forecast to be strong. Our quantitative assessment of the residential market, overlaid with our qualitative views, means that we expect national property prices to rise by around 8% in 2021 (9% for houses and 5% for apartments). We forecast dwelling prices to rise by a further 6% in 2022 (7% for houses and 4% for apartments) taking the combined price rises over the next two years to a little over 14%.

The effect of record low mortgage rates on dwelling prices is expected to wane a little in 2022 – it is the change in rates that provides the impulse on the housing market rather than the level of rates (chart 9). But working the other way will be an expected lift in population growth as the international borders are reopened which will boost the underlying demand for housing.

Our base case for property prices in Sydney and Melbourne sees them rise by 7.5% and 7% respectively over 2021. Stronger price rises are forecast for all other capital cities. We do not produce point forecasts for regional Australia, but note that price gains in 2020 were stronger in regional Australia than in the capital cities. This trend looks likely to continue in 2021.

Table 1 details our point forecasts by capital city. There are both upside and downside risks to our forecasts, as discussed below, but overall the risks are skewed to the upside.

Risks

Downside: In our view there are three key downside risks to our property price forecasts.

First, the reintroduction of macro-prudential measures to slow the rate of growth in lending. Measures introduced a number of years ago to slow both the rate of growth in lending to investors and the rate of growth in interest-only lending were successful in slowing dwelling price appreciation. At this stage we consider the reintroduction of macro-prudential measures to be a relatively low risk in 2021. That is because we expect only a modest lift in the outstanding stock of household debt (new lending is rising but lower interest rates accelerate debt repayment). However, if new lending accelerated too quickly, particularly to investors, there is a risk that the Australian Prudential Regulatory Authority (APRA) could reintroduce macro-prudential measures to slow things as they did in 2017.

Second, a lift in the RBA cash rate resulting in higher standard variable rates. That appears highly unlikely given the RBA has stated that it does not expect to increase the cash rate until, “2024 at the earliest”. But it is a risk nonetheless and must be considered given the single biggest driver of property prices in the short run is changes in interest rates.

Third, a significant outbreak/s of COVID-19 that resulted in large-scale extended lockdowns as was the case in Melbourne last year between July and October.

Upside: The key upside risk to our forecasts is sustained exuberance combined with FOMO (’fear of missing out’) which could generate a turbo-charged rise in prices. Indeed we consider this to be the biggest risk to our forecasts given the demand impulse from interest rate cuts, the level of interest rates relative to the rental yield and the recent spike in momentum indicators. History shows that prices can rise very quickly when the housing market is on a roll. Indeed it may turn out to be the case that the growth profile for price outcomes over the next two years ends up more front loaded than our current projections.

A second upside risk is any further policy changes to boost housing demand such as first-home-owner grants or lower stamp duty (to domestic or foreign buyers). This looks unlikely, however, given the current state of the market.

Finally, if the RBA do not remove or increase the target yield on the 3yr Australian Government bond that would mean that fixed rates are unlikely to drift higher in H2 2021 and 2022 as we expect. However, the risk overall of interest rates being lower than we expect is small given the cash rate is at the effective lower bound, the economy is on an entrenched recovery path and negative interest rates remain, “extraordinary unlikely”. Normally we would consider lower than expected mortgage rates to be an upside risk. But with the cash rate target, the target yield on the 3-year Australian Government bond and the interest rate on Term Funding Facility all at 0.1%,that risk is small.

Concluding thoughts

Monetary policy and more specifically the cost of money impacts all asset markets, including housing. The reason that asset prices, including dwelling prices, can seemingly decouple from the economy comes down to largely one thing – central bank policy and changes in the cost of money.

The COVID-19 economic shock has resulted in the RBA taking the policy rate down to the effective lower bound. But it is easy to forget that interest rates were incredibly low before the pandemic. The RBA delivered three 25bp cuts to the cash rate in 2019 that took the policy rate to just 0.75%. As a result, dwelling prices were rising strongly when the COVID-19 shock hit.

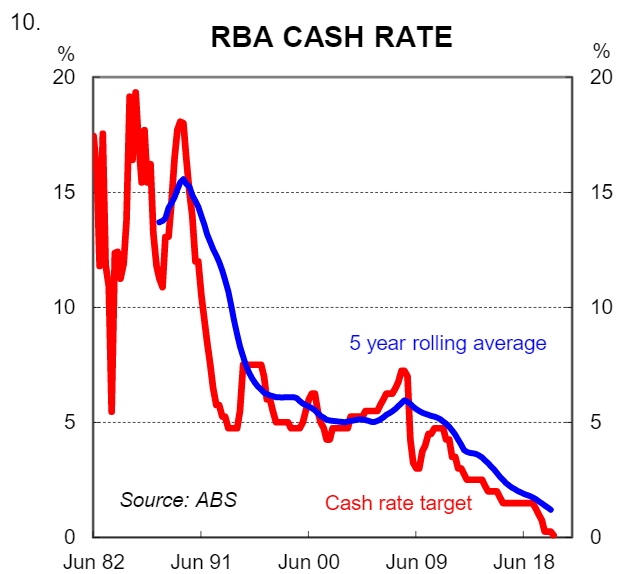

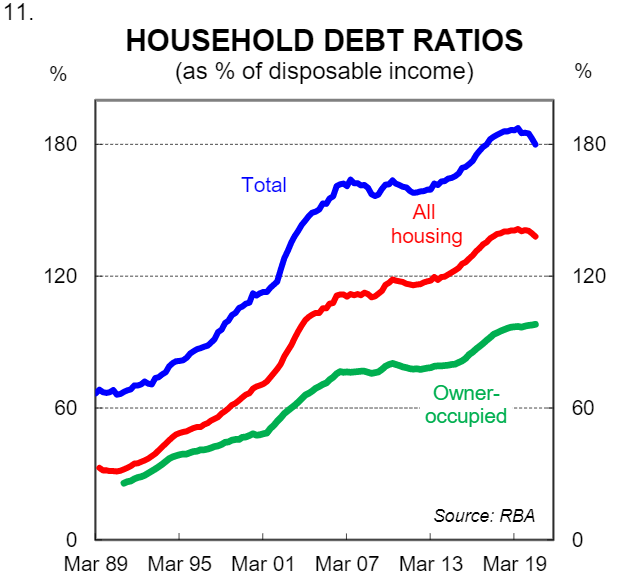

As American economist Herbert Stein so eloquently stated, “if something cannot go on forever, it will stop.” The process of cutting interest rates to stimulate economic activity over the past 30 years has resulted in the policy rate now sitting at 0.1% (chart 10). Over that period, the increase indwelling prices has massively outstripped income growth and the ratio of household debt to income has climbed (chart 11).

It will be incredibly hard for the RBA to raise the cash rate in any material sense from here given the level of household indebtedness. Indeed we estimate the neutral rate has fallen to around 1.0%. This means that when the next negative economic shock arrives we are unlikely to have the interest rate lever available to give households debt relief. In addition, we won’t be able to stimulate the interest rate sensitive parts of the economy with more rate cuts. This leads us to believe that we are inching towards a new paradigm that will involve some form of monetary financing in the future (i.e. a direct transfer of money from the central bank for government to spend). It may still be a long time away, but the bottom line is that the system as we know it will need to be reset and the printing press will be part of that reset.