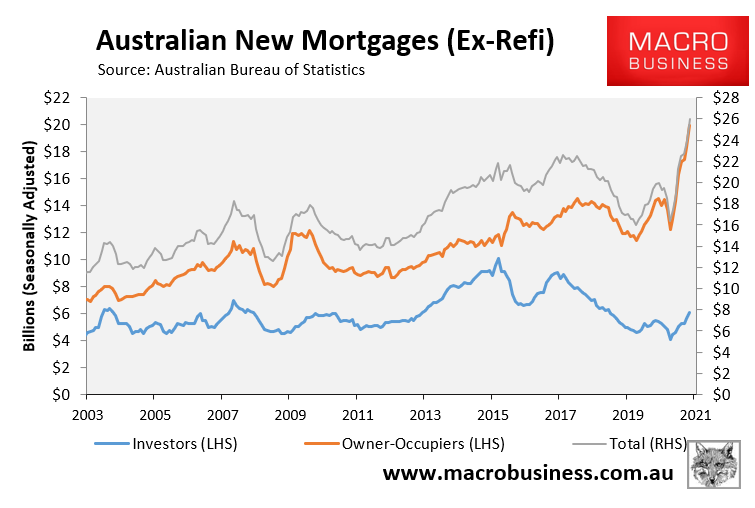

December’s housing finance data from the Australian Bureau of Statistics (ABS) revealed that mortgage demand has rocketed to unprecedented levels after experiencing 31% growth year-on-year:

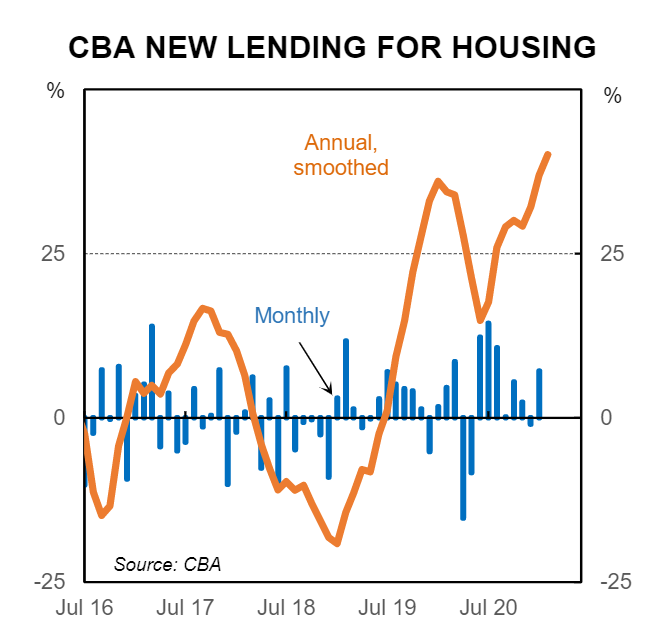

CBA’s economics team has released new internal mortgage data showing that the strong momentum continued in January, with new lending for housing soaring to new highs:

New lending for housing continues to grow at a strong pace. Lending growth is a good leading indicator of movements in dwelling prices. We expect dwelling prices to rise by around 14% over the next two years…

Advertisement

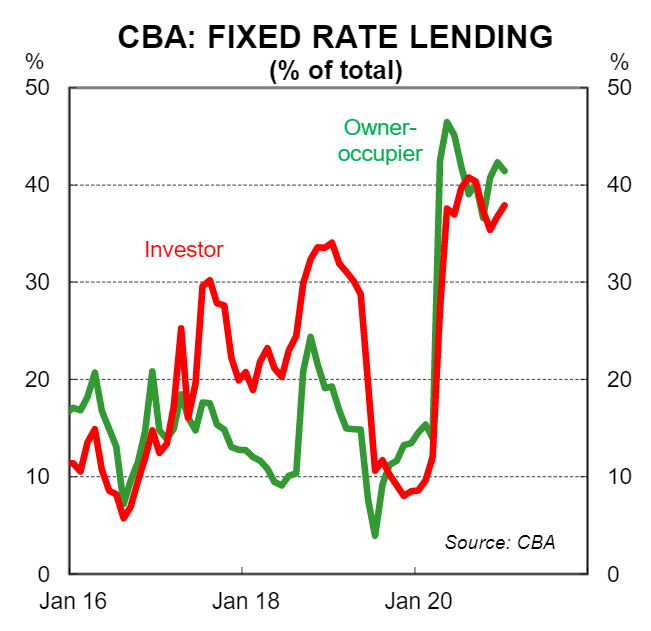

The share of fixed rate mortgages remains near all-time highs (circa 40%), reflecting the rock-bottom borrowing rates on offer:

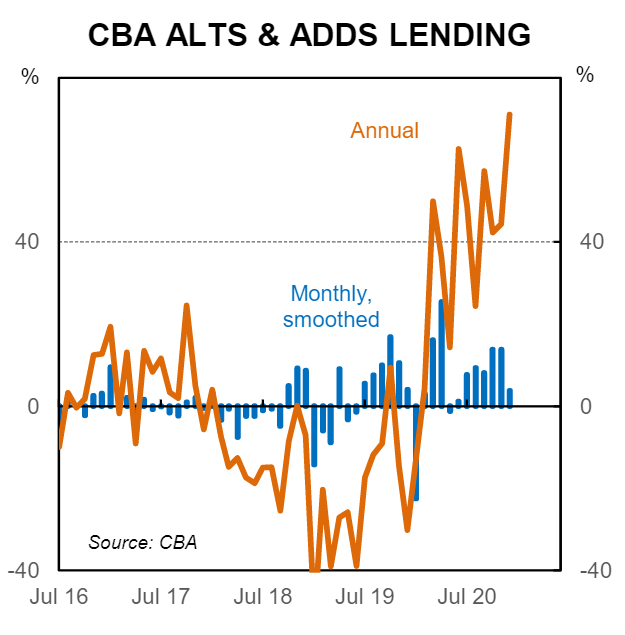

Aussies are also borrowing large for renovations, with lending growing at a very strong pace:

Advertisement

Given CBA is the nation’s biggest bank, we can be confident that its loan book reflects the broader market.

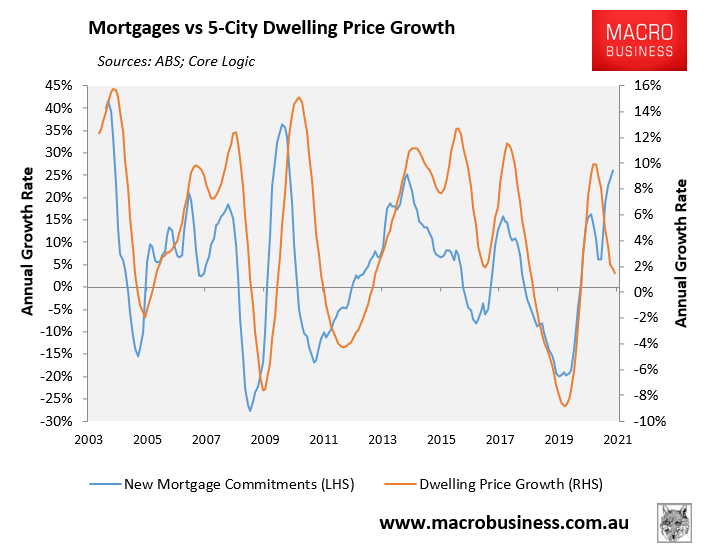

As we know, mortgage growth is the best single short-term indicator for property prices, typically leading prices by about six months:

Advertisement

Thus, the fuse is lit and Australian property prices are set to boom!

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.