DXY was up and away last night:

That was enough to sit on the Australian dollar:

The AUD is much stronger than EMFX:

Gold is breaking down as oil surges:

DXY alos sat on base metals:

Big miners eased:

Runaway EM stocks too:

Happy days in high risk ville:

US yields eased:

But stocks still don’t like the bond back-up:

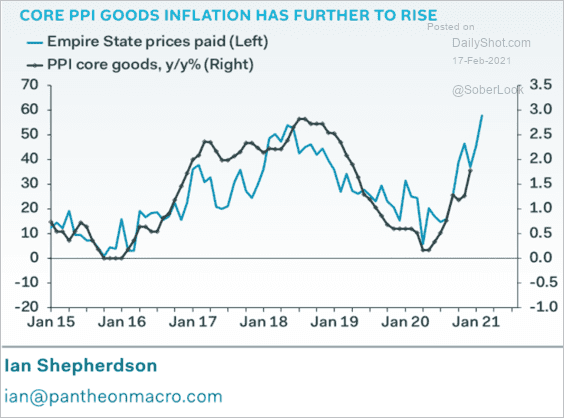

It is looking increasingly possible that the US dollar has put in a medium-term bottom. US stimulus is much more powerful than elsewhere. Its vaccine rollout is better as well. And its recovery is set to be very powerful. Its inflation pulse is also much stronger and headed for a spike

A lot of this inflation is temporary. Virus-related supply-side blockages, the orientation of spending to goods plus the inventory restocking cycle is driving it. All will begin to come off in H2 as economies reopen and China moves to tighten. I will add that the Biden Administration shows no sign of lifting the Chinese tariffs, a key driver of the last DXY bull market.

But, for now, we need to add rising US yields to the picture and this no longer adds up to a weak DXY.

For the Australian dollar this is mixed news. The inflation pulse will probably keep markets interested in commodity hedges, that is if the BTC bubble doesn’t steal the lot, as it appears to have done to gold.

But a rising DXY takes care of a lot of that US inflation anyway and it is always a headwind for both EMs and commodities so we may be near a peak there as well, especially in iron ore.

I can see a scenario here in which the Australian dollar is effectively topped out:

- US growth, inflation and yields are all materially higher than Europe and EUR rolls.

- China’s export boom continues on the back of developed economy recovery and it keeps tightening and slowing sharply into 2022.

- Both monetary and fundamental demand drivers for commodities go bust despite inflation hedging.

- Australian yields are still rising with the US but a softening China means the RBA moves to an Operation Twist and sits on the long end before the Fed does.

Don’t get me wrong. I still think inflation will fade in H2, and that might provide the AUD with another round of reflation, but not if China tightens and slows into 2022.