The superannuation industry has displayed a rare glimpse of honestly, with the Association of Superannuation Funds of Australia (ASFA) – the peak policy, research and advocacy group for superannuation funds – admitting that Australia’s superannuation system is grossly unfair in that it provides the greatest concessions to those that need it least: high income earners.

In its pre-Budget submission, ASFA has called for lower superannuation tax rate for people who earn between $37,000 and $45,000, and higher tax for those at the top of the income scale. It also says superannuation accounts with more than $5 million should be moved out of the super system:

ASFA accordingly recommends that the low-income superannuation tax offset should apply to individuals with taxable income of up to $45,000…

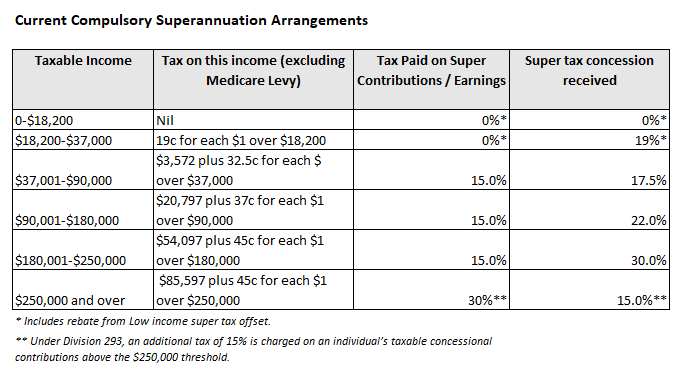

The RIR [Retirement Income Review] Report observed that high-income earners enjoy a greater share of the tax concession in relation to concessional contributions. Because tax on concessional contributions is levied on the superannuation fund at a flat rate of

15 per cent, those members on higher marginal tax rates enjoy a greater tax concession than those members on lower marginal tax rates.

Division 293 tax is an additional 15 per cent tax on concessional contributions that effectively reduces the tax concession on contributions for high income earners…

There are equity grounds, identified by the RIR, for adjusting settings applicable to those with higher incomes and/or high account balances. In this regard, ASFA considers that equity across the system can be improved through a modest reduction in the Division 293 threshold from $250,000, removing indexation of the transfer balance cap and removing balances above $5 million from the concessionally taxed superannuation system.

Superannuation is about ensuring people are comfortable in retirement, it is not about facilitating excessive wealth transfers.

However, ASFA still maintains that the superannuation guarantee (SG) should be lifted to 12% from 9.5% currently:

Advertisement

For many Australians the increase to 12 per cent SG is essential to offset the financial loss from super withdrawn under the COVID-19 early release scheme…

ASFA considers the legislated change in SG needs to go ahead as scheduled on 1 July 2021 with full implementation by 1 July 2025.

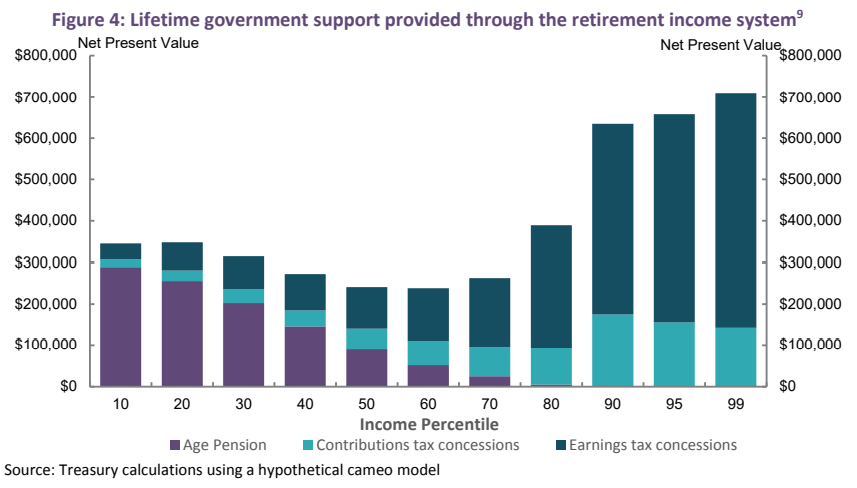

It is good to see ASFA acknowledge that the superannuation system is grossly unfair. This is illustrated clearly by the below Treasury chart showing that high income earners receive the lion’s share of concessions and more taxpayer support than low income earners on the full aged pension:

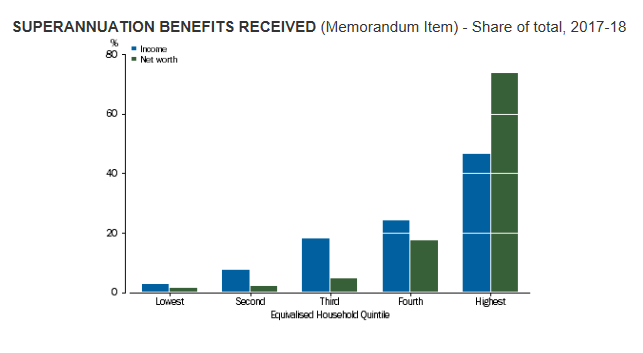

In 2017-18, total household superannuation benefits received was $112,009m. Households in the highest income and net worth quintile received 47% and 74% of total household superannuation benefits, by comparison households in the lowest income and net worth quintile received 3% and 2% of total household superannuation benefits.

Lifting the SG to 12% would obviously make the above inequity even worse alongside increasing the cost to the federal budget.

Advertisement

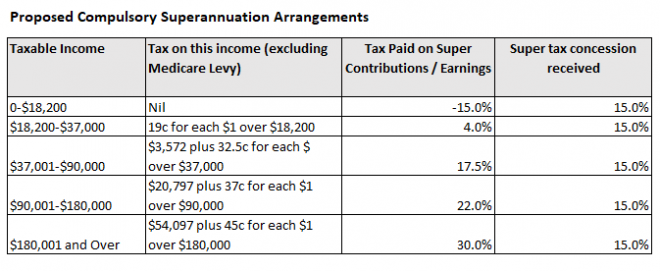

An simpler solution to improve equity and budget sustainability would be to scrap the planned increase in the SG and instead replace the 15% flat tax on contributions/earnings with a flat-rate refundable tax offset (e.g. 15%):

This way, everybody that contributes to superannuation would receive the same tax concession, the system would be made progressive, and lower income earners would get a better deal.

Advertisement

However, implementing the above reforms would also deprive the super industry of additional funds under management and the opportunity to earn fatter fees.

Therefore, the industry continues to lobby for an increase in the SG to 12%, despite its adverse impacts on wage growth, the federal budget and inequality.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.