As we know, the superannuation industry has been lobbying ferociously for the federal government to proceed with the legislated increase in the superannuation guarantee (SG) to 12% from 9.5% currently.

The industry argues that failure to lift the SG would lower the living standards of Australian workers by lowering their retirement nest eggs. The industry also maintains that lifting the SG would not threaten wage growth.

Regular readers know that MB does not support the industry’s contention (despite us offering the MB Super Fund). We believe that lifting the SG to 12% represents unambiguously poor policy because it would:

- Lower workers’ take-home pay, hitting lower income earners especially hard;

- Increase inequality, since the bulk of superannuation concessions go to where they are not needed – i.e. higher income earners; and

- Reduce the long-term sustainability of the federal budget, since the cost of superannuation concessions is greater than the Aged Pension savings.

Our view is supported by Australia’s peak welfare agency, the Australian Council of Social Services (ACOSS), which opposes lifting the SG.

Like MB, ACOSS has previously argued that lifting the SG to 12% would hurt low-income earners, and demanded that the “flawed system” of tax breaks for super concessions be fixed before there are any further increases in the SG:

ACOSS chief executive Cassandra Goldie said the $3 trillion system of “forced saving” under superannuation “paid too little heed to the needs of people struggling on low incomes during working life” and must better consider people on low wages when they are younger.

“The flawed system of tax concessions for super contributions should be fixed before compulsory contributions are lifted to 12 per cent”…

“For people on lower incomes, who often struggle to meet the basics of life now, the benefits are not so clear.

In its latest pre-Budget submission, ACOSS has again questioned the efficacy of lifting the SG to 12%, instead calling for reform to super concessions to make them more equitable:

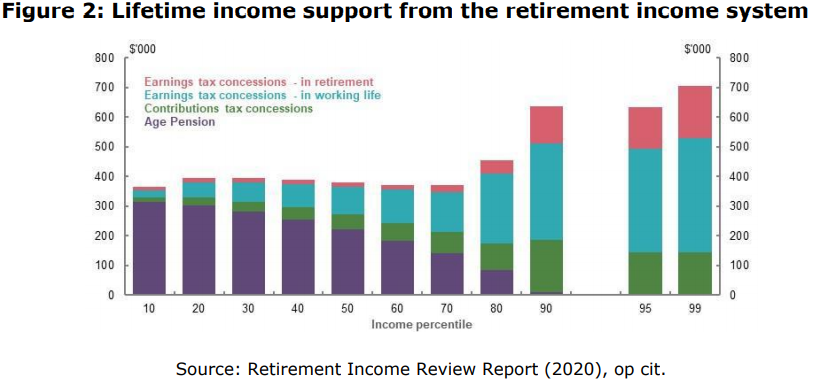

The Retirement Income Review Report convincingly shows that superannuation tax concessions are highly inequitable, skewing lifetime public support for retirement incomes towards those in the highest 20% of income-earners (Figure 2)…

The Superannuation Guarantee (SG) is legislated to increase from 9.5% currently to 12% by 2026.

ACOSS has consistently raised concerns that contributions at this level or higher may force people with low lifetime incomes to save when they are under the greatest financial pressure to fund a living standard in retirement that is higher than that which

they had through working life.The next increase in the SG from 9.5% to 10% of wages in July 2021 should proceed, since collective pay agreements may have already taken this increase into account when setting wages.

Before the SG is lifted above 10%, the benefits of higher compulsory contributions for the median wage-earner and those with lower incomes should be demonstrated, and tax concessions for contributions should be reformed…

People on low and modest incomes presently receive little or no support from $25 billion a year in foregone public revenue…

Tax concessions for contributions should first be reformed so that they receive at least the same subsidy, per dollar contributed, as people with higher incomes.

This could be achieved at no extra fiscal cost by replacing existing tax breaks for contributions with a uniform annual rebate up to a (lower) annual cap.

Tax concessions for superannuation cost $42 billion a year, almost the same as the Age Pension, and disproportionately benefit high income-earners…

This flat superannuation tax should be replaced with a rebate (for example, 20% of contributions from all sources) that provides the same or greater support for each dollar of contributions for people with low incomes as that provided to middle and high income-earners…

Only 16% of people over 64 years pays income tax, though many have the capacity to do so. In addition, once their super fund pays them a pension it pays no tax on its investment income. This is not sustainable if future governments are to guarantee decent health and aged care services for an ageing population.

Superannuation fund earnings post-retirement should be taxed at the same 15% rate as they are in the accumulation phase…

ACOSS is right. There is no way that the SG should be lifted 12% until the concessions structure is overhauled and made equitable.

Raising the SG without first fixing the concessions structure would simply heighten the current inequities and inefficiencies, rob workers of disposable income, and blow a bigger hole in the federal budget.

The only winners would be the rent-seeking superannuation funds, which would earn fatter fees from the extra funds under management.