Demographer Mark McCrindle has called for a new baby bonus to arrest the nation’s falling birth rate:

When introducing the baby bonus scheme in 2002, then federal treasurer Peter Costello famously encouraged Australians to “have one for mum, one for dad and one for the country”.

“Even if there was just one for mum and dad because we’re not even hitting that [replacement rate],” Mr McCrindle said…

Mr McCrindle said it was likely the birth rate would drop even further in 2021 as people delayed having children because of the coronavirus pandemic…

Mr McCrindle said the drop in international migration owing to border closures would also slow the country’s growth and contribute to an ageing population.

“I don’t think we need a lot of population growth but we don’t want to go backwards, so suddenly births are the key, that can really do something,” he said.

Mark McCrindle really needs to read Dr Jane O’Sullivan’s recent research paper, entitled “Silver tsunami or silver lining? Why we should not fear an ageing population”, which expertly debunks misplaced fears over an ageing population:

Key Points

With people living longer than ever and the baby-boomer generation reaching retirement age, some people worry that we will run short of workers and taxpayers. But demographic ageing will stop well before that occurs. Retirees will never outnumber younger adults.

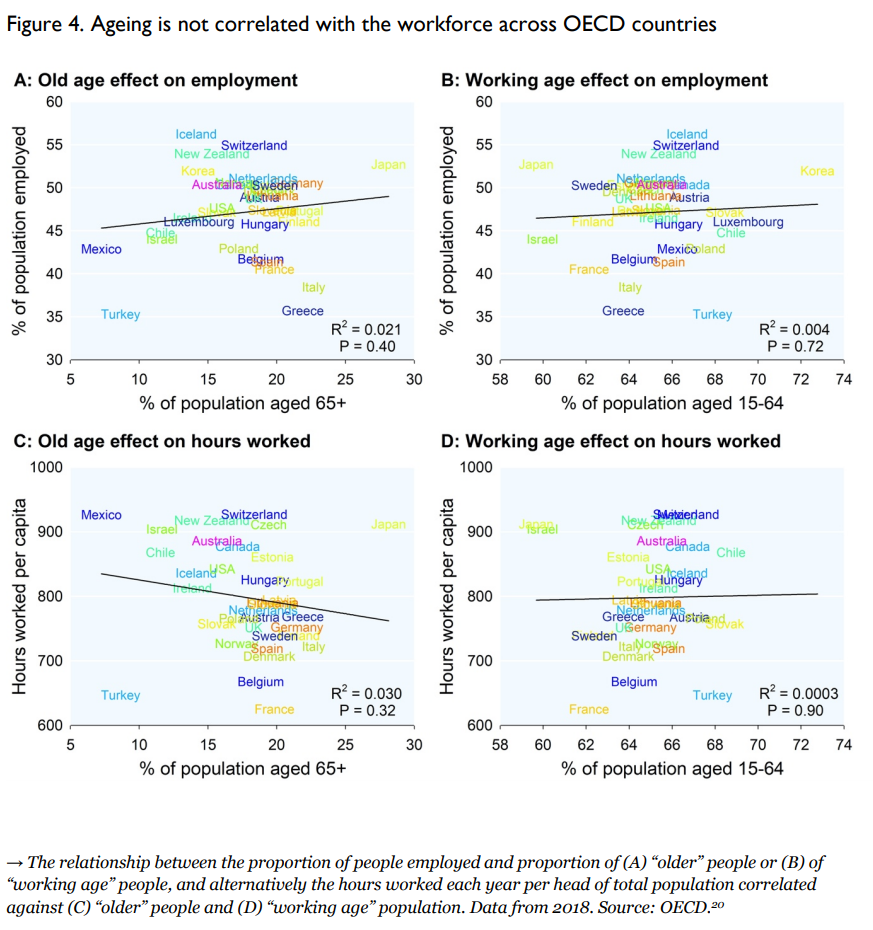

In the countries that have aged the most, there has been no shortage of workers. Instead of less employment, they have less unemployment and underemployment. Economic models that predict less economic activity as populations age are based on false assumptions.

The rise in the proportion of older citizens accounts for only a small fraction of the rise in health costs. The major increase in costs is due to new, improved and more services per person.

Longevity has deferred, rather than extended, the period in which the elderly need more health care and aged care.

High levels of immigration can slow, but not prevent, population ageing. But the cost of extra infrastructure and education to sustain population growth is greater than the avoided costs of pensions, health care and aged care.

Those with vested interests in population growth have overstated ageing concerns, to make high immigration seem essential. The resulting negative social and environmental impacts continue to accumulate for no net economic gain…

The workforce responds dynamically to the demand for labour

Despite several countries already experiencing a declining proportion of working-age people for more than two decades, none has seen a related decline in workforce. Compared with Australia, Japan has almost twice the proportion of older citizens but roughly the same proportion of people who have jobs.

With the same demand for workers but fewer working-age people competing for jobs, there is less unemployment and underemployment.

Improved wages and conditions attract more people into the workforce. This is what economic theory expects the labour market to do. But the economic models which predict that ageing will constrain the workforce have ignored these feedbacks…

Boosting population growth does not solve ageing

The Australian government’s main response to demographic ageing has been to boost population growth through incentives to have more children (particularly the “baby bonus”) and elevated immigration levels. Neither strategy prevents population ageing in the long run.

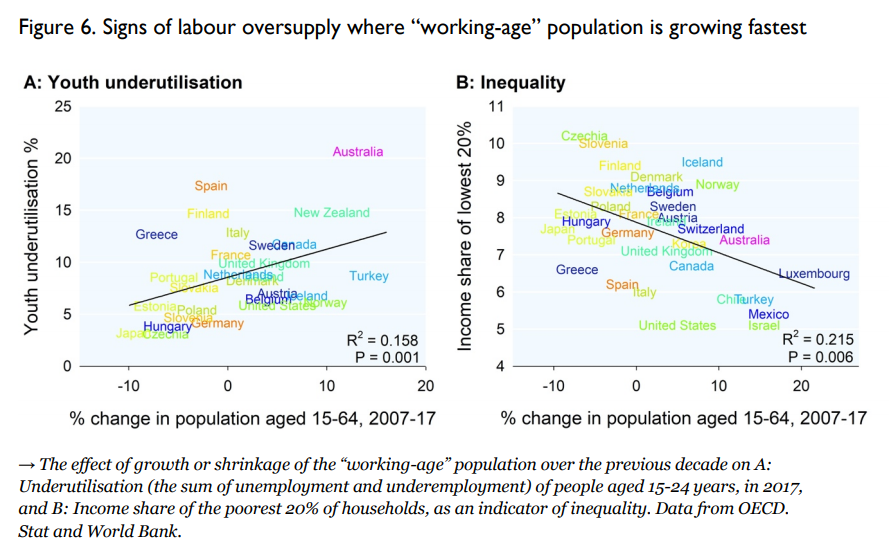

As immigration levels are increased, each additional migrant has less and less effect on the population age structure. Boosting births increases the proportion of children rather than working-age people. There is no evidence that boosting the working-age proportion has increased employment per capita. Instead, Australia’s labour market has been oversupplied, with high immigration contributing to youth underemployment, wage stagnation and rising inequality.

The cost of population growth exceeds the cost of ageing

The Parliamentary Budget Office (PBO) estimated that ageing will cost the Federal budget “around $36 billion by 2028-29”. This estimate is based on two false assumptions: (1) that a smaller working-age proportion means less economic activity, and (2) that health and aged care costs rise in proportion to the over-65 population.

Even if the latter were true, the cost of extra infrastructure to support population growth outweighs the small extent to which that population growth could lessen pension, health-care and aged-care burdens. Most of this infrastructure cost falls to State and local governments, and private individuals, rather than the Federal government.

The national interest should not be narrowly defined as merely achieving a balanced Federal budget. The rate of population growth is at the discretion of the Federal government. Changing policies on immigration and pronatalism could quickly ease congestion and improve State government finances, and would allow infrastructure to catch up with our recent growth…

Silver tsunami or silver lining?

An older, numerically stable or decreasing population offers many benefits for quality of life, environmental sustainability and economic stability. Depopulation dividends could make us richer, smarter, safer, fairer, greener, healthier and happier.

Advertisement

One of the reasons why Australia’s faces a population ageing ‘problem’ today is because of the high birth and immigration rates of the 1950s and 1960s.

These migrants (which include my parents) and baby boomers have now grown old, thus adding to Australia’s current ageing ‘problem’.

Therefore, promoting greater birth rates or importing more migrants to solve ageing is the equivalent of ‘can-kick economics’, because today’s children and migrants will also grow old, thus creating further ageing problems in 40 year’s time. Some migrants will also bring along older family members.

Advertisement

The solution to Australia’s ageing ‘problem’ rests on tackling the two Ps of productivity growth and greater labour force participation.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.