Karen Maley has published an article in The AFR entitled “Why we should stick with the 12pc super guarantee rate”, which is worth countering since it makes a number of dubious arguments:

The [Retirement] review points out that the old-age pension has been rising faster than inflation over the past decade, and has risen faster than wages since 2014.

But the problem is that there’s no guarantee that the Australian economy will always be robust enough to afford to provide a large cohort of retirees with a decent old-age pension.

It’s simply impossible to predict what the economy will look in 50 years, when someone who is entering the workforce now in their early 20s will be contemplating retirement…

Because it’s imprudent to assume that Australia will always be affluent enough to afford to pay retirees a satisfactory old-age pension, it makes sense to encourage people to build up the financial capacity to fund their own retirement.

What’s more, the Callaghan review rhapsodises the economic benefits that the country receives from the $3 trillion in retirement savings…

“The investment of superannuation assets will play a significant role in the recovery of the Australian economy from the downturn initiated by the COVID-19 pandemic.”

And it points out that the federal government’s decision to allow people suffering financial stress during the pandemic to access up to $20,000 of their compulsory super savings helped cushion the impact of the pandemic…

Frydenberg should show leadership by making strong commitment to eventually raising the rate to 12 per cent for all employees…

First, Maley’s argument about budget sustainability doesn’t hold much water given the cost of raising the super guarantee (SG) outweighs any benefits from lower future pension outlays.

Indeed, lifting the SG to 12% would cost the federal budget an extra $2 billion a year, which comes on top of the already outrageous $43 billion in annual costs from superannuation concessions.

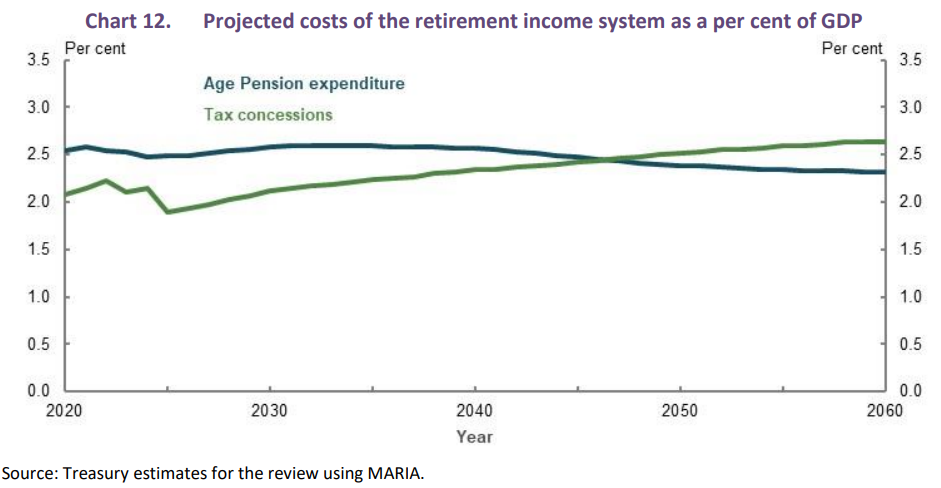

Government expenditure on the Age Pension as a proportion of GDP is projected to fall slightly over the next 40 years to around 2.3 per cent [from 2.5 per cent]. Higher superannuation balances reduce Age Pension costs. The cost of superannuation tax concessions is projected to grow as a proportion of GDP and exceed that of Age Pension expenditure by around 2050. This is due to earnings tax concessions. The increase in the SG rate to 12 per cent will increase the fiscal cost of the system over the long term…

The sustainability of compulsory superannuation is best assessed by looking at its full budgetary impact and not just the reduction in Age Pension expenditure as the superannuation system matures. The cost of superannuation tax concessions also needs to be taken into account…

Around 71 per cent of people over Age Pension eligibility age received Age Pension or other pension payments as at June 2019. Notwithstanding an ageing population, this proportion is projected to fall to 62 per cent in 2060. There is also a shift toward people receiving a part-rate pension (rather than the full-rate pension), rising from 38 per cent of age pensioners today to a projected 63 per cent in 2060. This shift is the result of higher superannuation balances and the impact of the means test, particularly the assets test, in determining eligibility for the Age Pension.

In contrast, as the superannuation system matures, the cost of superannuation tax concessions is projected to grow as a proportion of GDP such that by around 2050 it exceeds the cost of Age Pension expenditure as a per cent of GDP (Chart 12). This is the result of growth in the cost of earnings tax concessions…

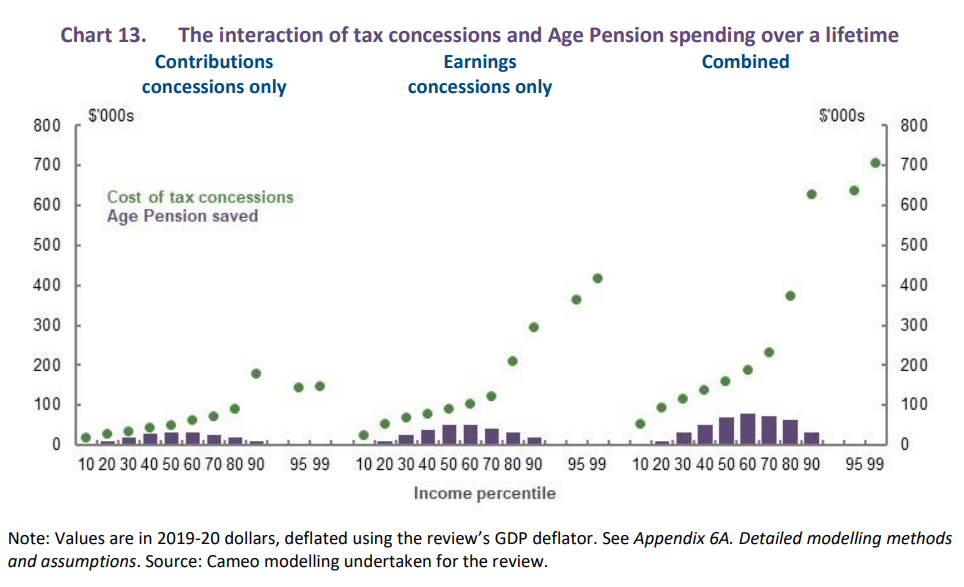

To the extent that superannuation tax concessions are contributing to higher superannuation balances of lower- to middle- income earners, they help to reduce Age Pension expenditure. But the main influence behind the growth in superannuation balances is the SG. Tax concessions are largely concentrated among higher-income earners who are close to and above preservation age. Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

The Retirement Income Review also added that the SG is “not a cost-effective way to help people achieve adequate retirement incomes” and actually increases inequality:

There are areas where superannuation tax concessions are not a cost-effective way to help people achieve adequate retirement incomes. In particular, the cost of the earnings tax exemption in retirement will grow faster than the growth in the economy as the system matures and provides the greatest boost to retirement incomes of higher-income earners…

Changes to superannuation earnings tax concessions would improve equity, and in turn boost public support for the system…

While the Age Pension helps offset inequities in retirement outcomes, the design of superannuation tax concessions increases inequality in the system. Tax concessions provide greater benefit to people on higher incomes.

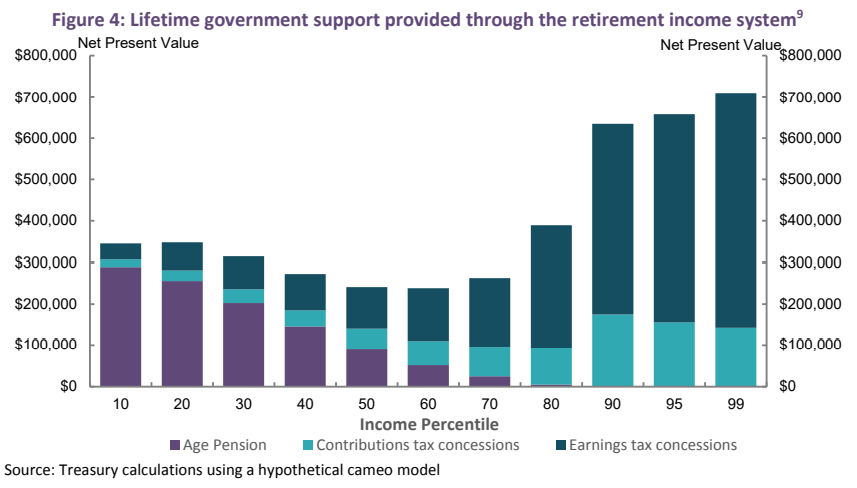

It’s easy to see why, given the lion’s share of super concessions flow to high income earners (see next chart). This makes superannuation more of a tax avoidance scheme for the rich than a genuine retirement scheme.

Advertisement

Maley’s argument about “the economic benefits that the country receives from the $3 trillion in retirement savings” is also spurious. Strangely, she has backed up this point by noting that “the federal government’s decision to allow people suffering financial stress during the pandemic to access up to $20,000 of their compulsory super savings helped cushion the impact of the pandemic”, which argues to give people access to their own money rather than locking it away in superannuation accounts.

That is, if giving people access to $20,000 of super savings was good for the economy, lifting the SG to 12% would pull disposable income from the economy and would be unambiguously bad.

Advertisement

Curiously, Karen Maley only gave lip service to the reduction in take home wages that would arise if the SG is increased and she didn’t even bother to mention the billions lost in fees each year due to inefficiency.

As we keep saying, the main beneficiary from lifting the SG to 12% are superannuation funds, which would earn fatter fees on bigger funds under management. But their gains would come at the direct expense of both taxpayers and workers.

It’s time to abandon the planned increases in the SG once and for all.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.