Federal Government stimulus – most notably the HomeBuilder and First Home Loan Deposit Scheme – has done a terrific job juicing new home construction.

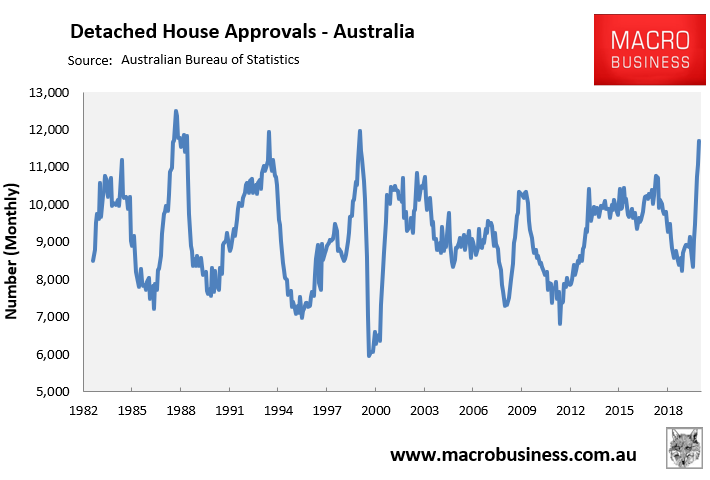

Detached house approvals have hit a 20-year high:

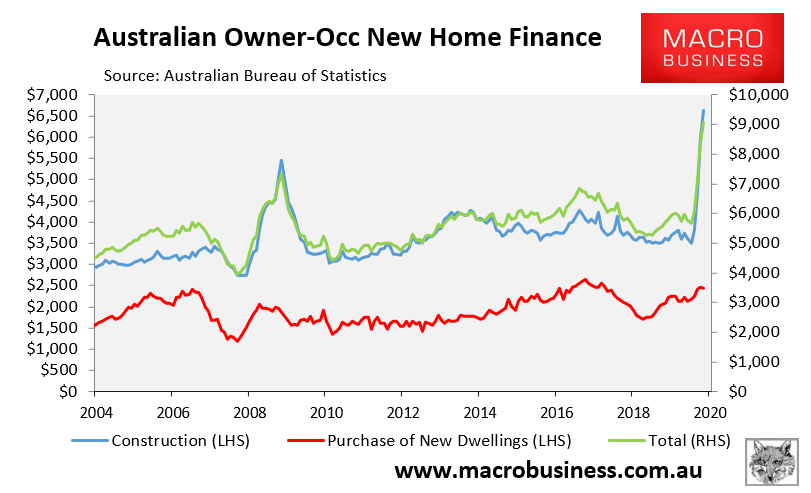

Whereas construction finance commitments have experienced an unprecedented rise:

This has inevitably posed the question of “what happens to construction when the stimulus unwinds”?

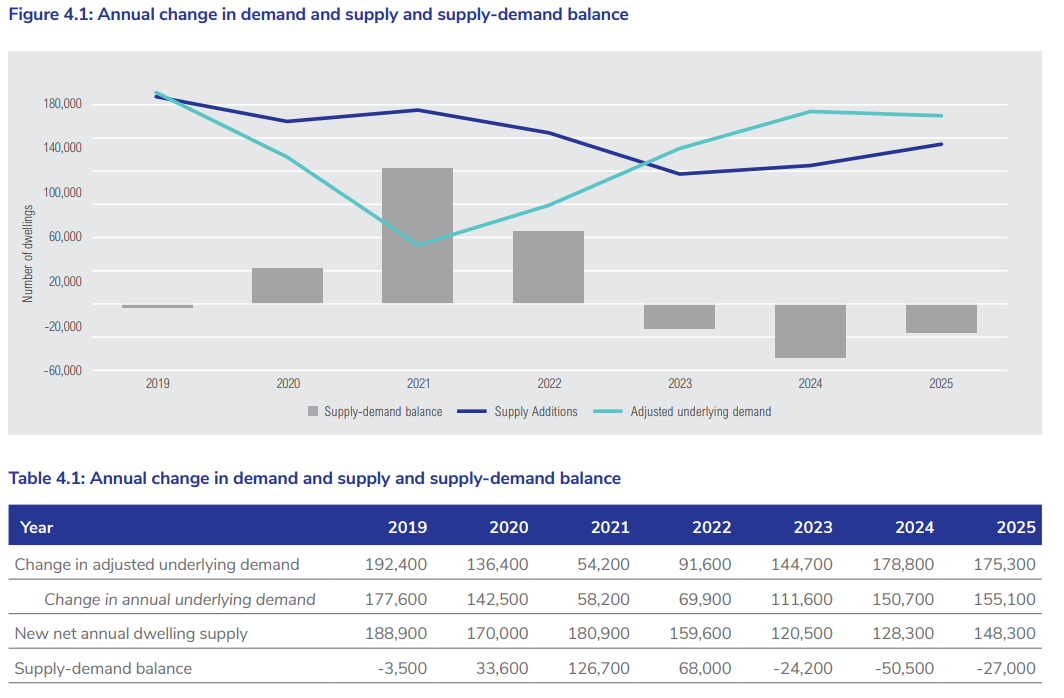

The latest forecasts from the National Housing Finance & Investment Corporation (NHFIC), released last month, forecasts that construction will collapse in 2022 as stimulus unwinds:

According to NHFIC, net annual dwelling additions will decline from 180,900 to 159,500 in 2022 and then to only 120,500 in 2023.

If these forecasts come to fruition, then the housing construction industry is facing a sharp contraction.

This will put pressure on federal and state governments to extend stimulus to prevent the downturn. It will also encourage the federal government to reboot mass immigration to backfill supply.

Australia is the property equivalent of a narco state, after all.