There has been a stunning recovery in the labour market but the rising share of part-time employment, rising participation and still elevated unemployment suggests the market is quite different to what it was pre-COVID.

Total employment: 50k from 90k (revised from 90k); Unemployment rate: 6.6% from 6.8% (unrevised 6.8%); Participation rate: 66.2% from 66.1% (revised 66.1%).

The labour market recovery has been far stronger than anticipated.

Total employment is almost back to pre-COVID levels while under-employment, and those working zero hours for economic reasons, are almost back to more normal levels.

But the recovery has all been in part-time employment as full-time employment remains well below per-COVID levels.

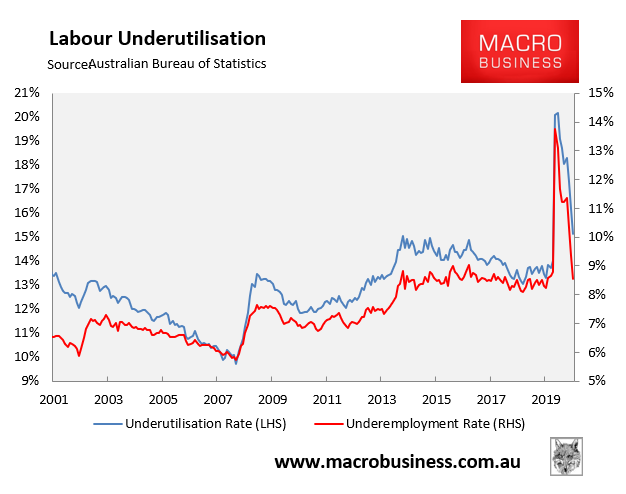

In addition, unemployment is still greater than pre-COVID levels as participation has lifted. Underemployment is also higher than March though it has improved at a much faster pace than expected. And with the recovery in employment being focus in part-time rather than full-time employment, total hours worked is still down -1.4% on March.

What is also surprising is that number of people working zero hours for economic reasons is back to around March levels, not something we expected to see until the second half of 2021.

Altogether, while there has been a surprisingly solid bounce back from the COVID shock it is also clear the structure and nature of the labour market is quite different to what it was pre-COVID. And, at least for now, the robust supply of labour is providing a significant offset to the robust demand for labour.

The Victorian economy re-opened on November 8th and with the ongoing recovery in NSW we had expected to see a positive employment run into the year end. Also, the Northern Beaches was not declared a hot spot until December 18, too late to have an impact on this survey.

In December total employment rose 50k (0.4%), a touch softer than Westpac’s +60k forecast and spot on the market median of +50k. Total employment has now lifted 518.8k from the April low and is just 87.6k (or 0.7%) below the level in March. This has been a far more solid recovery from the significant shock of the COVID lockdowns than was widely expected.

In the month full-time employment gained 35.7k/0.4% while part-time employment gained 14.3k/0.3%. Part-time employment has surged back in the early post COVID recovery and is now 24.7k/0.6% higher than in March. By contrast full-time employment continues to lag and is 112.4k/1.3% lower than it was in March.

In November the survey reported a decline in unemployment even with a solid lift in participation; for December we had expected to see the re-opening of the Victorian economy to continue to drive participation higher and for this reason unemployment would drift higher even with solid employment gains. In the end, participation lifted 0.6ppt to 66.16% resulting in a 20.0k lift in the labour force which was less than the gains in employment hence the 0.2ppt fall in the unemployment rate to 6.6% (from 6.83% to 6.60% at two decimal places).

Also underpinning just how strong this recovery has been the trend improvement in underemployment which continued in December with the rate falling from 9.4% in November to 8.5% in December. The national underemployment rate is now 0.3ppt lower than it was in March, a very unexpected outcome. We had thought underemployment would remain elevated especially as the share of part-time workers, who tend to have a higher rate of underemployment than full-time workers, grew.

The underutilisation rate, which combines unemployment and underemployment, fell -1.1ppt to 15.1%. Given the higher level of unemployment the underutilisation rate is 1.1ppt higher than it was in March. In May it peaked at 20.2%, 6.1ppt higher than March.

What is also surprising is that number of people working zero hours for economic reasons is back to around March levels, not something we expected to see until the second half of 2021. Westpac estimates an effective unemployment rate which as well as those defined as unemployed includes those that work zero hours for economic reasons as well as adding back those that left the labour market with the COVID shutdowns hit (by assuming the participation rate can go no lower than where it was in March). The effective rate peaked at 15.4% in April and by December it was back down to 7.2%, a significantly better improvement than expected. The effective unemployment rate is currently 0.6ppt higher than the official unemployment rate. Back in March the effective unemployment rate was 5.8%, also 0.6ppt higher than official unemployment. With out a doubt is appears at the national macro level we have seen a full correction to the COVID shock to the labour market.

Even with such a significant improvement in the labour market, we are yet to say that the labour market can be described as tight. It is not just that unemployment is higher than March but the employment to population ratio is 0.6ppt lower. In addition, with the recovery in employment being focus in part-time rather than full-time employment, total hours worked is still down -1.4% on March. Part-time hours worked are 1.4% higher than March with hours worked per part-time employee up 0.8%. Full-time hours worked are -1.9% less than in March with hours worked per full-time employee down -0.7%. So not has the share of part-time workers grown but they are also being worked harder, which may help to explain the fall in underemployment and fall in zero hours worked.

By contrast, not only are full-time workers struggling to get back to March employment levels they are also being worked less. The fact that full-time workers tend to me more attached to the labour market would help to explain why participation is so elevated participation, with the increase in part-time work drawing in more workers interested in part-time work (particularly females) while full-time workers remain on the sidelines looking for a job.

Nevertheless, even with these caveats we have to admit it has been a stunning recovery in the Australian labour market in a very short period of time.

Turning to the states, Victoria has been a key driver employment gains in the last three months (+170.3k since September) but it also may have helped to spur a further recovery in NSW (+43.6k since September) and Qld (+41.5k) where it had appeared that the recovery was stalling. Given that the December Northern Beaches outbreaks (which lead to tightening of COVID restrictions in Sydney and the closure of the borders by Victoria, Qld, SA and WA) occurred too late to be captured in this survey we would expect any impact to show up in January. The Weekly Payrolls data did reveal a sharp downturn in late December but we don’t know if this is earlier, or larger, than the usual seasonal downturn in employment experienced during the Christmas/Summer holiday period. We need to see the Payrolls data for the first two weeks in January to see if this downturn deepened much further.

Victorian total employment lifted 14.6k in December while participation fell -0.2ppt to 66.0% seeing the force there by drop by -7.5k leading to a -0.6ppt fall in the unemployment rate to 6.5%. Victorian unemployment peaked at 7.4% in October.

The unemployment rate fell 0.1ppt in NSW to 6.4%, even with a -17.1k fall in employment, as the participation rate fell 0.5ppt to 65.6% with a -22.6k fall in the labour force.

Unemployment also fell in Queensland, down –0.2pp to 7.5%, but this time it was due to a solid 36.6k gain in employment more than offsetting a 0.7ppt rise in participation to 66.7% resulting in a sound 33.7k lift in the labour force.

Unemployment fell 0.1ppt in WA to 6.2% (the state holds the national low for unemployment) as the small 0.4k gain in employment was offset by a -0.1ppt fall in participation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.