Four and a half years after the vote, Britain is properly out of the European Union and moving into a new era. It will surely be a freer nation, but will it be a richer one? Anatole has argued that the UK faces a long period of sub-par growth that will leave it worse off. My approach in this piece will be to consider the UK’s position by asking three questions: (i) What is the message from financial markets, which are forward-looking? (ii) How is the UK positioned as a trading nation? (iii) Which parts of the world economy will it gravitate towards, now that it can move according to opportunities rather than EU diktat?

Part 1: The message from financial markets

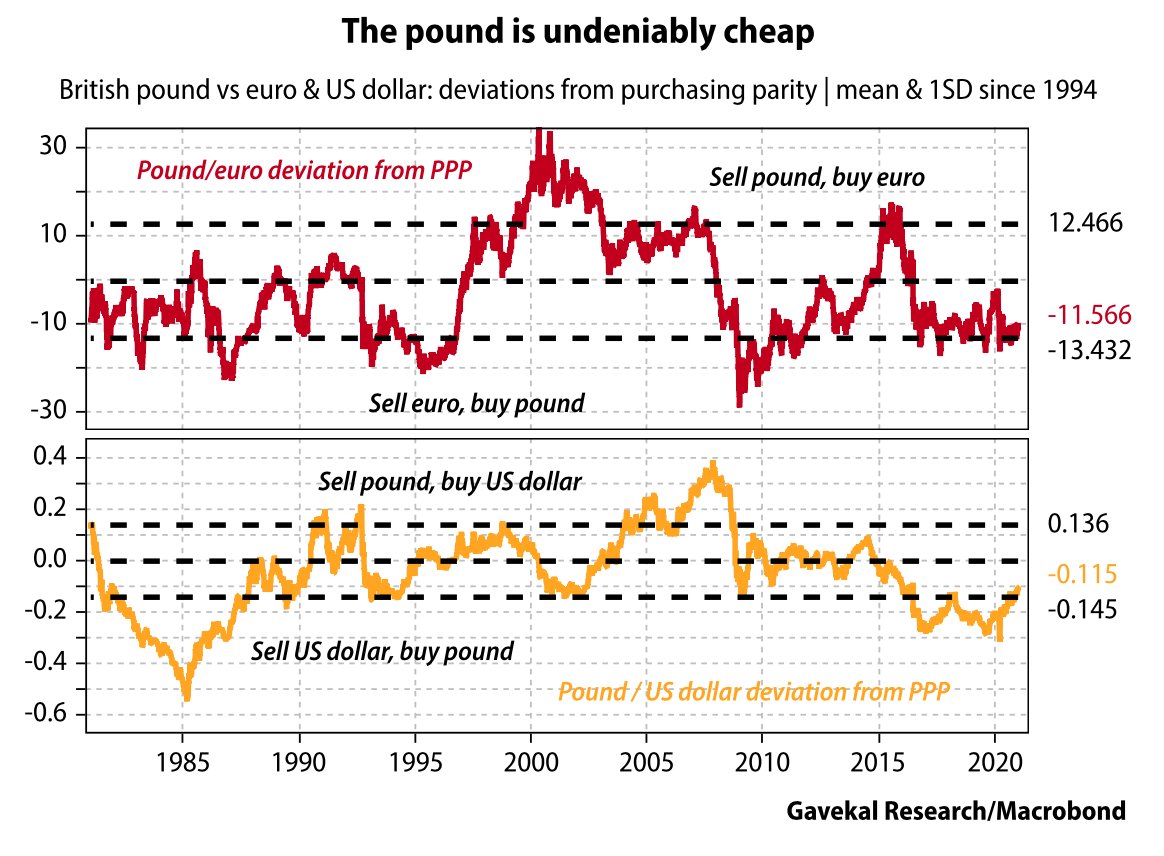

The exchange rate Let’s start with the sterling exchange rate, and deviations in percentage terms between the spot rate (red and yellow lines) and its purchasing power parity level (PPP line at zero). The reversion to PPP is one of the great “return to the mean” trades; it always happens but one never knows when. The “good news” for sterling holders is that the pound has been “undervalued” for more than four years against both the euro and the US dollar.