AFR senior correspondent, Aaron Patrick, has taken aim at Paul Keating’s compulsory superannuation system, claiming it “has evolved into a state-sponsored tax shelter for non-self-made millionaires”:

Super is stacked in favour of the rich… men like former prime minister Paul Keating who spent their careers in high-paid careers now benefit from super rules so loose that today more than 10,000 people with $5 million and above in their accounts receive at least $70,000 a year in tax concessions…

“With higher-income earners receiving more superannuation tax concessions than lower- and middle-income earners, the superannuation tax concession component of government support increases inequality of private incomes for people aged 65 and over,” the [retirement] review states on page 40…

The consequence, according to the analysis by Callaghan, Kay and Ralston, is that superannuation has evolved from promoting retirement self-sufficiency to preserving family assets to pass on to children…

While the debate rages over increasing the superannuation guarantee, which would generate tens of billions for the superannuation and finance industries, a more serious challenge is mostly ignored.

Over the long term, super tax breaks are going to become a bigger budget cost than the age pension, which already consumes 2.5 per cent of total economic output, according to the review.

In other words, Keating and his fellow rich retirees will get more from the state than most struggling pensioners.

Well argued. Because one’s superannuation nest egg is a function of how much they earn and how long they work, it automatically misses lower income earners and those with broken employment histories (such as mothers).

Accordingly, the lion’s share of tax concessions flow to higher income earners – a situation made worse by the 15% flat tax on superannuation contributions/earnings, which gifts higher income earners the biggest tax benefits:

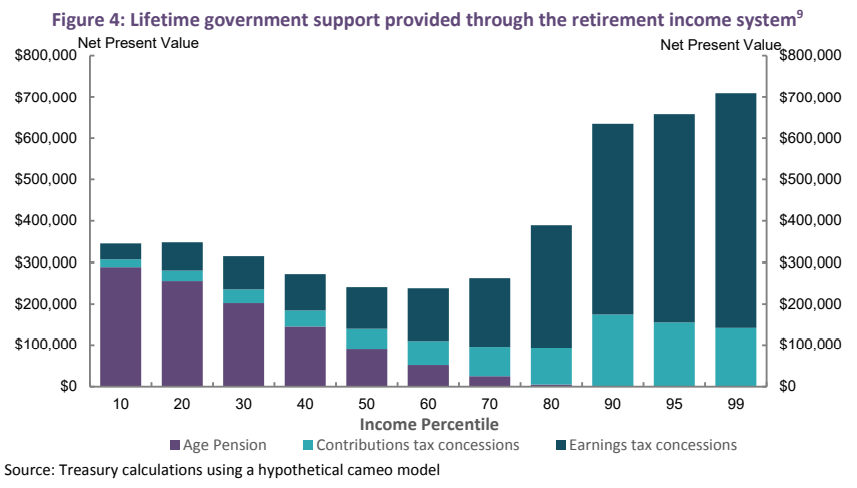

As illustrated above, taxpayers spend at least twice as much supporting the retirements of the top 1% of income earners as they spend on someone receiving the age pension.

Looking at superannuation specifically, the top 1% of income earners are projected by the Treasury to receive more than $700,000 in superannuation concessions over their working lives, roughly 14-times the $50,000 of concessions received by the bottom 10% of income earners.

Thus, the superannuation system effectively takes the disparities in working-life incomes and magnifies them in retirement, enshrining inequality in the process.

At a minimum, the scheduled increase in the superannuation guarantee to 12% should be cancelled by the federal government, since it would only worsen the above inequalities and further damage the federal budget.

Preferably, the compulsory superannuation system should be abolished altogether, with the massive budget savings redirected into lifting the Age Pension – Australia’s true retirement safety net.