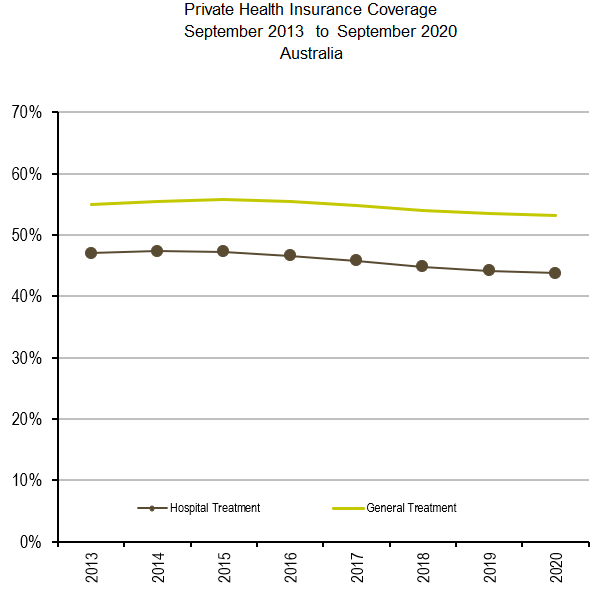

The latest private health insurance coverage data from APRA revealed that the private health hospital coverage of adults fell to a new low of 43.8%, and has fallen by 3.3% since the Coalition took office in 2013:

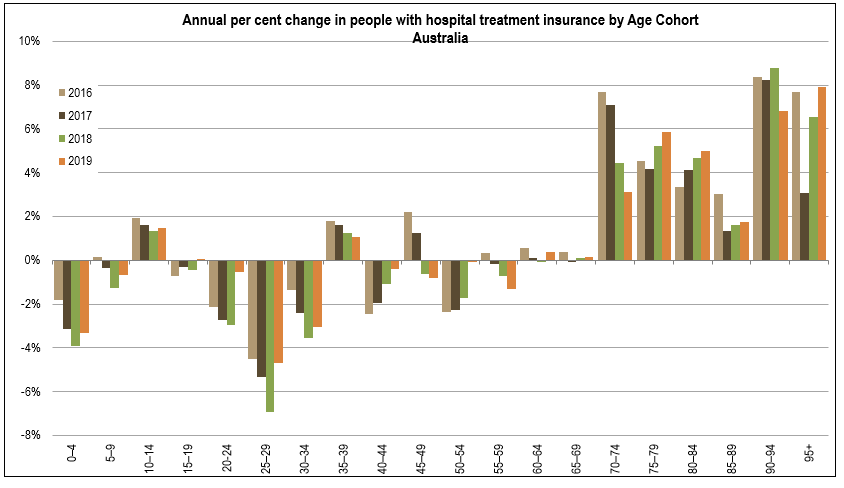

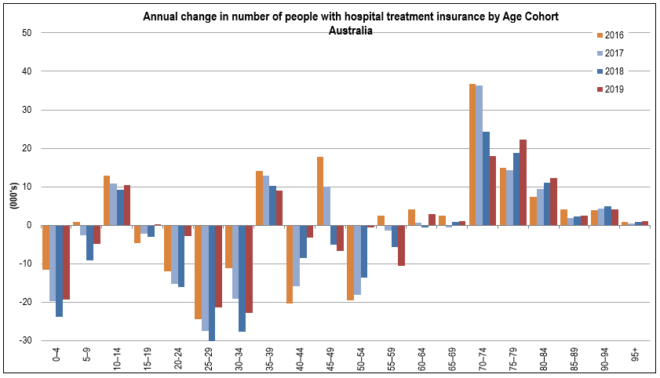

Separate annual data from APRA also shows that coverage has collapsed amongst healthy young cohorts while rising among the elderly:

Advertisement

The above charts add weight to the claim that Australia’s private health insurance industry is facing a ‘death spiral’. Young and healthy people (the so-called “invincibles”) continue to leave system, thus leaving a larger proportion of unhealthier, older, expensive users.