ANZ Research has released a new report on the New Zealand property market, which claims that a “perfect storm” has developed that has driven “unprecedented gains”:

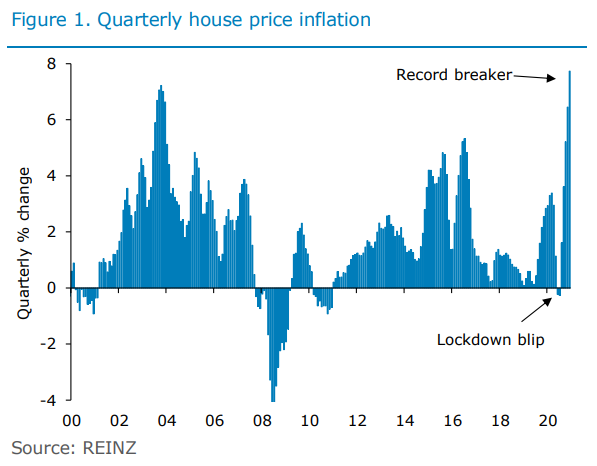

Record Breaker

House prices rose 2.9% in December, following similar stellar rises in October and November. This saw a quarterly gain of 7.7% for Q4 (figure 1) – the biggest quarterly gain on record (based on data from 1992).

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.