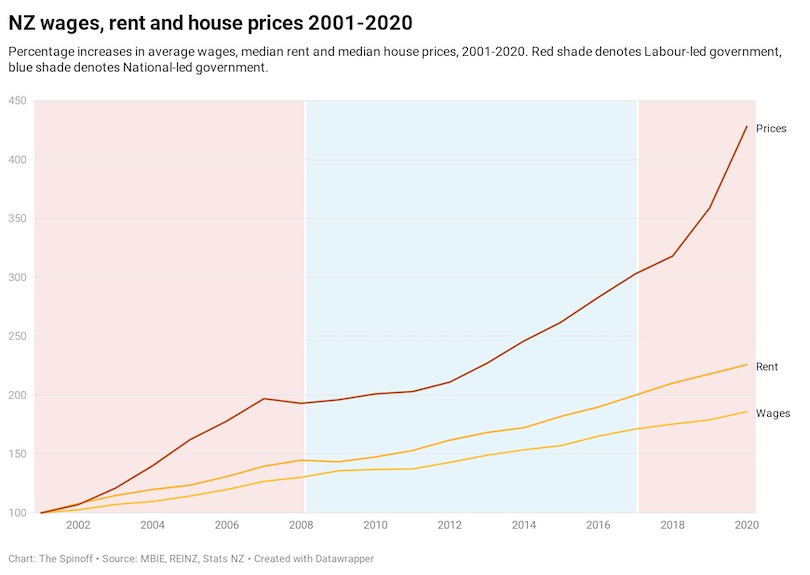

The Spinoff has published the below “deranged” chart on New Zealand’s housing market showing how for two decades, under both National and Labour governments, housing costs have risen far faster than wages:

Labour is in a real bind here, because while 2020’s extraordinary 20% year-on-year price rise is an unmitigated disaster for anyone trying to save a deposit for a home, it’s also partly why Labour remains so enormously popular…

Each of the main parties shares something else in common: that for all their concern at runaway prices, none will ever admit the cost of housing might need to come down. All we ever get is an expressed desire for prices and rents to stabilise, to stay flat so that wages might start to catch up.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.