Workers are paying between 71% and 100% of increases to the superannuation guarantee (SG) through lower take-home wages. This is according to research commissioned by the federal government’s Retirement Income Review, with the research being undertaken by two Australian National University economists.

Release of the research comes as the Morrison Government is deciding whether to proceed with the legislated incremental increase of the SG from 9.5% of gross wages to 12% between July and 2025, while the economists have advised the government to balance the goal of increasing superannuation amounts with the costs and benefits of doing so.

From The AFR:

The document, The Economic Incidence of Superannuation, was obtained by The Australian Financial Review.

ANU Tax and Transfer Policy Institute professor Robert Breunig and senior research officer Kristen Sobeck concluded that “workers bear the cost of increases in the superannuation guarantee through lower wage growth”.

“The results suggest that wage growth for workers who receive above the superannuation guarantee rate is consistently lower than wage growth for those who receive the superannuation guarantee,” they said in a report to inform the review.

“As a result, total compensation across the two groups of workers tends to converge over time suggesting that workers initially bear the majority of the incidence of superannuation and over time they bear the full incidence.

“These results translate to workers bearing between 71 per cent to more than 100 per cent of the costs associated with legislated increases in the superannuation guarantee through lower wage growth”…

“Lower wage growth also implies less disposable income available to workers and their families to consume today or to save through alternative means,” they noted.

“Subsequently, the government will forgo the tax revenue from labour income taxed at individuals’ marginal personal income tax rates, for greater superannuation contributions that are taxed concessionally.”

Indeed, the Retirement Income Review explicitly noted that lifting the compulsory SG rate to 12% would disadvantage low-income earners and reduce workers’ lifetime incomes:

“A rate of compulsory superannuation that would result in people having an increase in their living standards in retirement may involve an unacceptable reduction in living standards prior to retirement, particularly for lower-income earners… This is based on the view, supported by the weight of evidence, that increases in the super guarantee rate result in low wages growth, and would affect living standards in working life”.

“The weight of evidence suggests the majority of increases in the super guarantee come at the expense of growth in take-home wages. The view is based on empirical research, economic theory, evidence across a number of countries and the original policy intent of superannuation guarantees”.

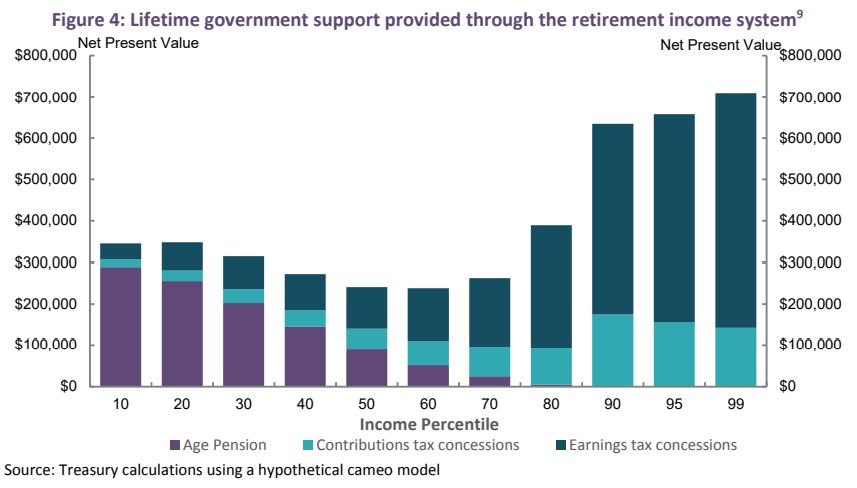

Australia’s compulsory superannuation system already exacerbates inequality by handing the lion’s share of tax concessions to high income earners:

According to the Retirement Income Review, inequality will worsen if the SG is lifted to 12%:

“Increases in the superannuation guarantee rate will increase lifetime government support for higher-income earners by more than lower- and middle-income earners.”

Therefore, the Retirement Income Review arrived at similar conclusions to MB, which from the outset has lobbied against lifting the SG to 12% because:

- It would suppress future wage growth and disposable income, which would most adversely impact lower-income earners already struggling to make ends meet.

- It would increase inequality, since higher income earners receive the lion’s share of super concessions.

- It would worsen the long-term sustainability of the federal budget, since the cost of superannuation concessions outweighs the benefits from lower pension outlays.

The main beneficiaries from lifting the SG to 12% would be super funds themselves, since it would provide them with more funds under management and enable them to milk fatter fees to the detriment of workers and taxpayers.

Lifting the SG to 12% was always bad policy and should be dumped by the Morrison Government.