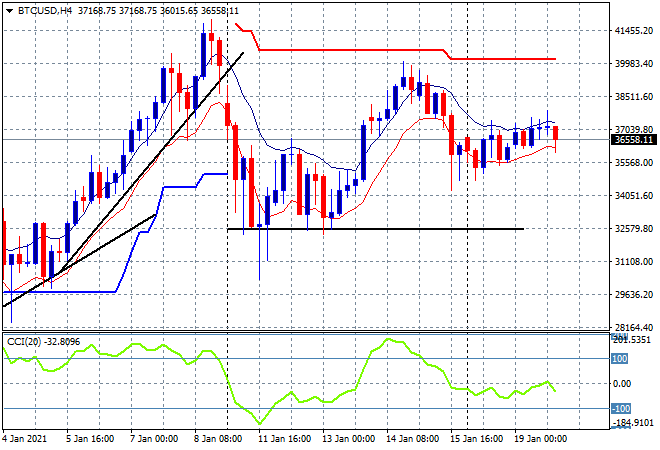

Two events changed risk appetite overnight with the closely watched German ZEW survey and Janet Yellen’s testimony in Congress supporting the bullish mood on Wall Street as traders returned from the US long weekend. Oil prices lifted more than 2% while the USD retreated against most of the majors. Bitcoin continued its tepid start to the week with lower volatility than usual, still hovering around local resistance at the key $36000 level as the consolidation trade continues – notice building resistance in the short term above $37K:

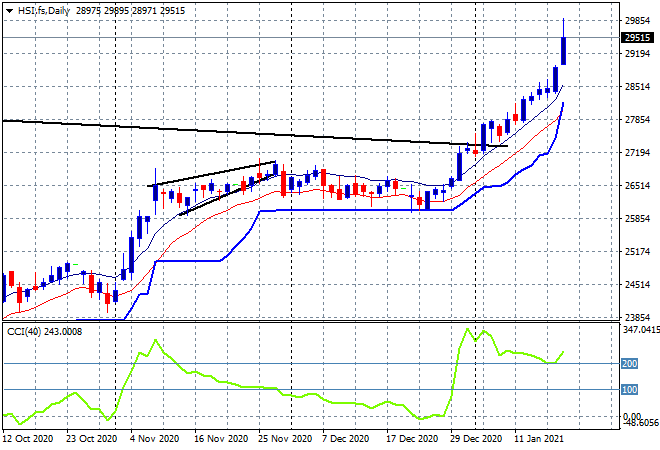

Looking at share markets in Asia from yesterday where the Shanghai Composite was flat going into the close but abruptly sold off, finishing down 0.8% to 3566 points. Meanwhile in Hong Kong the Hang Seng Index soared higher, breaking out significantly again and rising nearly 3% in one session, closing at 29642 points. The daily chart shows a huge lift higher that is not sustainable with a blowout trade here moving too far above the trendline and ripe for a pullback:

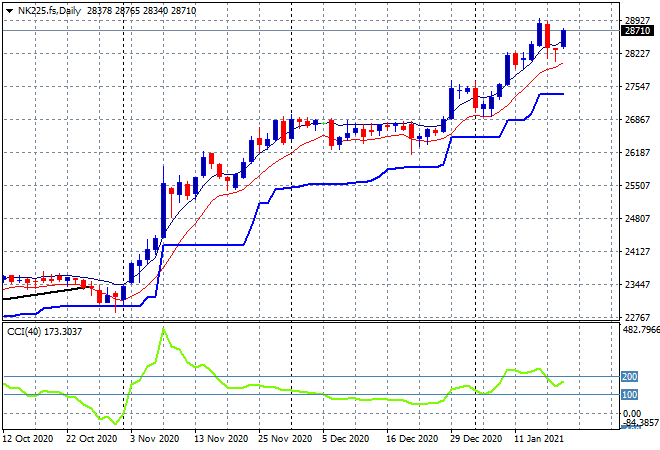

Japanese markets were in reverse mode, taking back all of Monday’s losses with the Nikkei 225 closing 1.3% lower to 28616 points. This is likely to reverse again today with futures suggesting a slight uptick on the open as the positive uptrend continues. The obvious 30000 point target level still remains obvious:

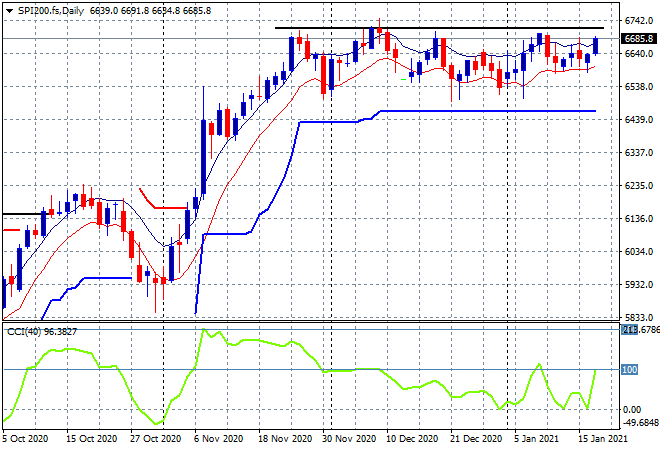

The ASX200 made a solid advance, closing 1.2% higher to 6742 points, heading straight back above the 6700 point level despite the Australian dollar putting on gains as well. SPI futures are indicating more upside on the open as the daily chart still signalling a clear bullish rectangle pattern as momentum picks up:

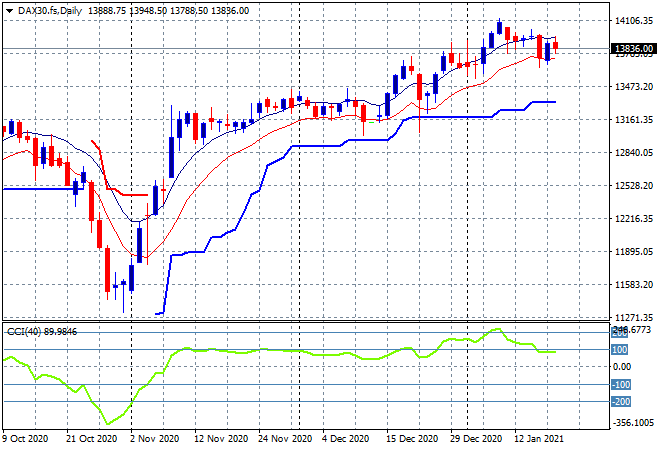

European markets had mild pullbacks across the continent due to a higher Euro despite the positive ZEW survey and the bullish mood on Wall Street, with the German DAX finishing 0.2% lower at 13815 points. Resistance at 14000 points is still too strong with the current stall phase continuing as momentum is no longer overbought. The potential for a swing play back down to ATR support at the 13200 point level is still there:

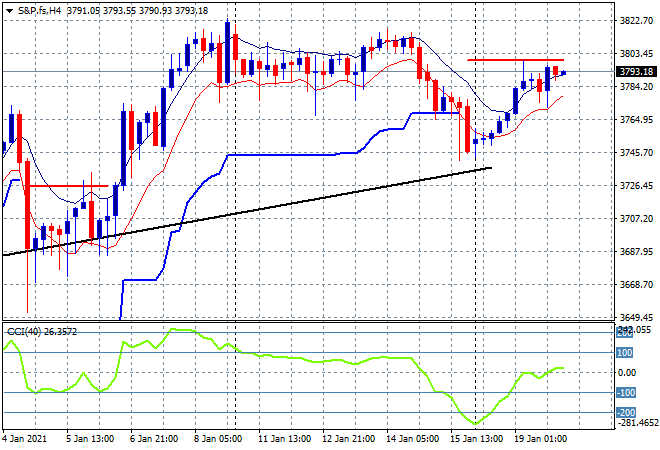

Wall Street returned from the long weekend with the S&P500 surging over 0.8% to finish at 3798 points. The four hourly chart remains on its post election trend, as the futures swing play converts into real returns this week but I still contend that the volatility of the upcoming inauguration/impeachment may shake things to the downside:

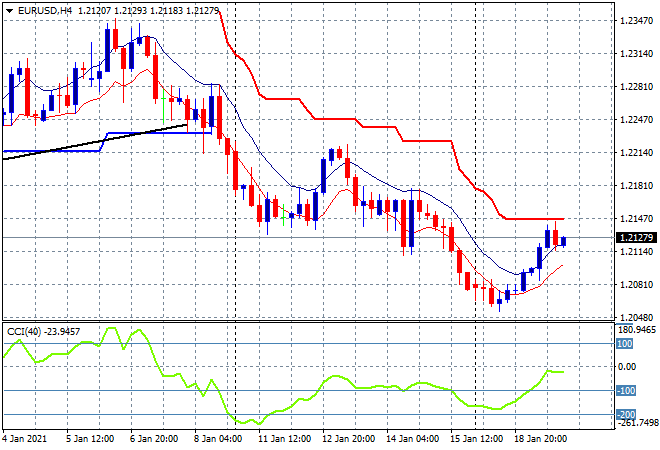

Currency markets came back into USD weakness on the ZEW survey but more so on the Yellen testimony, where the prospect of a lot of fiscal stimulus saw the USD fall against the majors, with Euro lifting right through the 1.21 handle overnight. This comes after making a two week low, and threatening former weekly support/former resistance at the 1.1950 level but the four hourly chart clearly shows this is not over with momentum not yet positive or overhead resistance cleared:

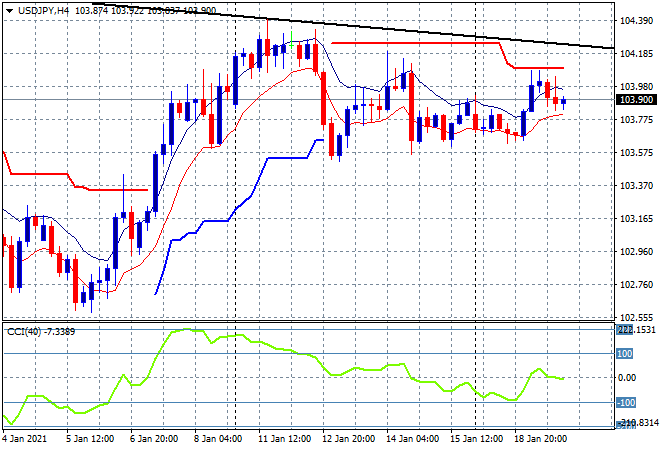

The USDJPY pair was pushed back only slightly however, with the four hourly chart showing a mild decline back below the 104 handle, which is firming as a key resistance level for sometime now. The long held downtrend from the 2020 highs (upper black sloping downtrend line) is still not under threat:

The Australian dollar had a minor push higher but was unable to sustain itself above the 77 handle overnight, showing a lot of internal weakness as a result. The four hourly chart is still very messy, showing an oscillation around the 77.50 point of control that still has the potential to swing back up there but the overall trend remains down:

Oil prices came back again as increased volume and a lower USD helped risk spirits, with Brent lifting more than 2% to be back above the $55USD per barrel level. Price remains just above the pre COVID February 2020 level (upper horizontal black line) with strong medium term support but it must make a new daily high soon or could suffer a quick rollover:

Gold remains the biggest loser with no real change in the overall deflationary downtrend, despite a lower USD, as it remans below last weeks session lows at the $1840USD per ounce level. As I said last week, basic price action just did not look good for the shiny metal and I would suggest we are on track to get back below the $1800 level very shortly:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!