Australia’s rent-seeking superannuation industry is talking its book again, this time calling on the federal government to deposit up to $5,000 into the bank accounts of low-income earners:

The Australian Institute of Superannuation Trustees (AIST) wants the government to top up the retirement accounts of low-income earners who withdrew money from their super to help them get through the pandemic…

According to AIST chief Eva Scheerlinck, those who had to access the scheme were “already experiencing disadvantage and … were already facing a retirement savings shortfall”.

She’s called on the government to help them make up this shortfall with a one-off contribution of up to $5000 paid into the retirement accounts of those who earn less than $39,837 a year, accessed their super early, and met certain eligibility criteria.

“This would be the most effective way to close the COVID super gap for these Australians,” she said.

“[The one-off] contribution would be set at a quarter of the value of the super the member accessed and be capped at a maximum $5000 contribution for those who accessed the full $20,000”…

The Grattan Institute is not a fan of the super top-up plan, saying there are more effective ways of keeping Australians out of poverty in retirement.

“If the concern is poverty, then there are much more direct ways to fix that than putting $5000 into someone’s superannuation account on the expectation that some of those people will struggle [when] they reach retirement, when many others won’t,” said Grattan’s household finances program director Brendan Coates…

“[A super top-up] is not a priority compared to increasing the social security net,” he said.

The motivation for AIST’s request is obvious: the taxpayer money deposited into member super accounts would increase funds under management and enable the super industry to extract fatter management fees. It is pure self-interest.

This is an industry, after all, that has grown solely on the back of government legislation mandating almost every working Australian deposit 9.5% of their wages into a super account.

The Australia Institute’s chief economist, Richard Denniss, sums up the industry nicely:

Much is made of the enormous size of Australia’s $2.9tn pool of superannuation savings, but we talk much less about the fact that the only reason it grew so big was that we literally force the vast majority of employees to spend 9.5% of their income buying superannuation every week. Let’s be clear: if we forced all Australians to get a massage every week or buy a new Australian car every year, we would have an enormous massage and car industry as well…

We hand out $43bn a year in tax concessions for super. It’s obscene and it only survives because the superannuation industry is so skilful at confusing people, boring people, or both…

Tax concessions for superannuation literally amplify inequality in Australia.

That’s right. Australia literally spends $43 billion a year to line the pockets of wealthy Australians, of whom receive the lion’s share of tax benefits:

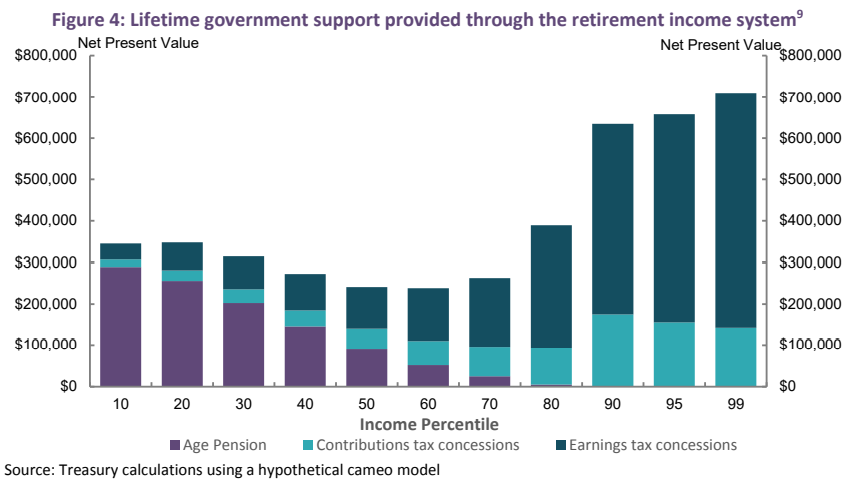

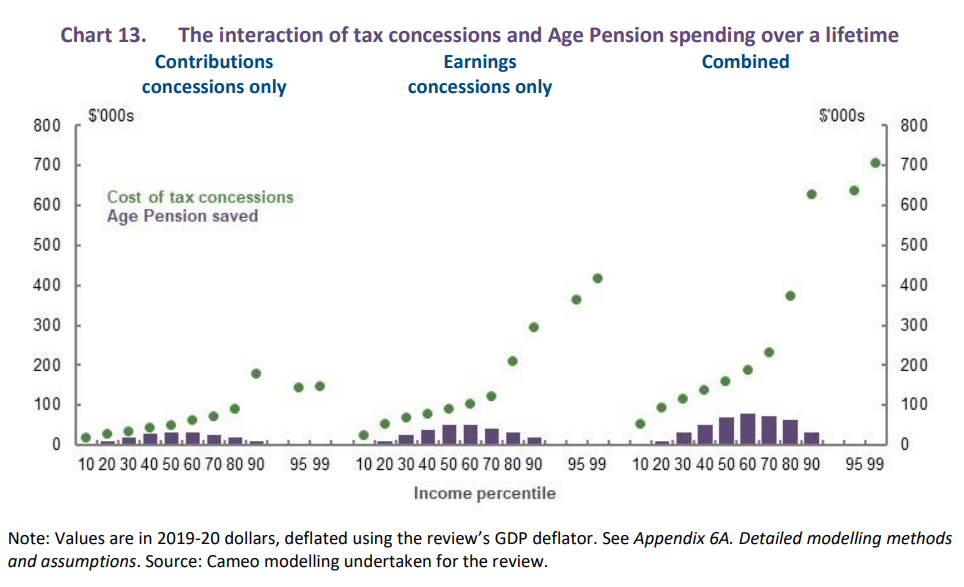

Worse, the high cost of these concessions and their poor targeting means that the superannuation system costs the federal budget more than it saves in Aged Pension costs, even over the long-run:

If lifting the retirement living standards of lower-income Australians is truly the goal, it would make far more sense to abolish compulsory superannuation altogether and redirect the immense budget savings into raising the Aged Pension – Australia’s true retirement safety net.

Of course, the parasites in the super funds management industry would never support such sensible policy. The super gravy train is simply too profitable.