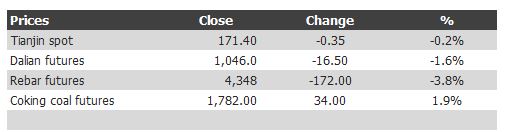

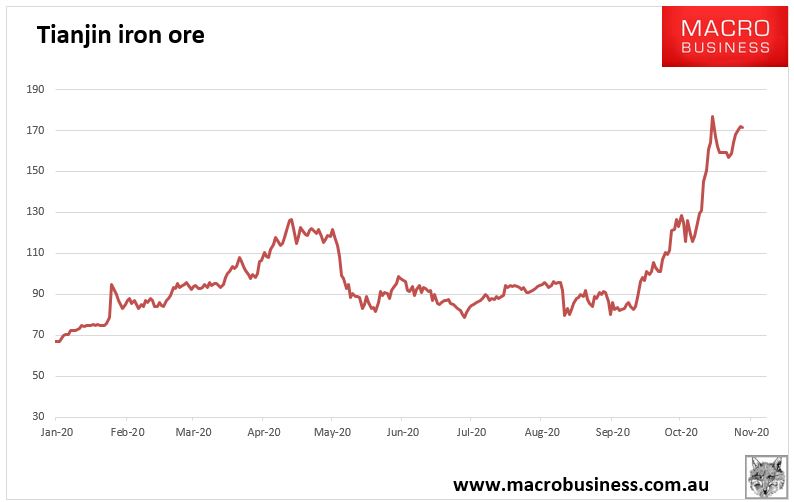

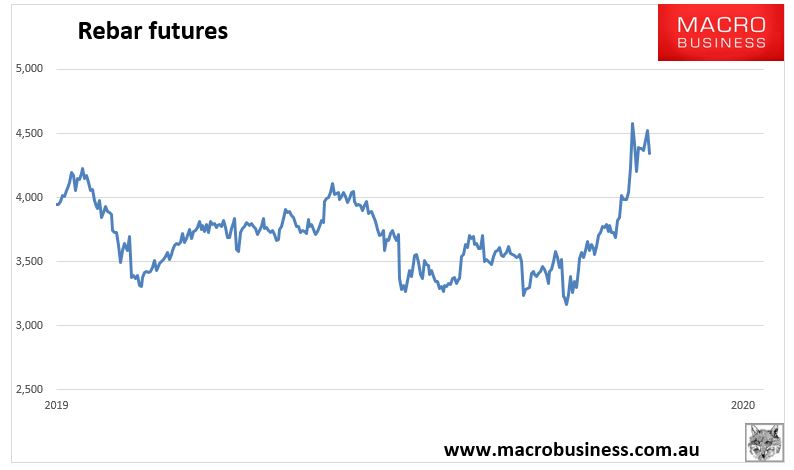

The iron ore complex had a wobbly start to the trading week as futures dropped alongside spot prices on Monday, as stockpiles increased for a second consecutive week on easing seasonal demand. Rebar futures dropped the most, down nearly 4% while spot iron ore still remains above $170USD per ton:

Meanwhile the Samarco mine will add to the seaborne supply this week after restarting operations in December, some five years after the collapse of a dam lead to 19 people killed, according to Mining.com

According to the company, approximately 75,000 tonnes of iron ore pellets will be shipped from Brazil to Europe. The company resumed its operations on December 23, with 26% of its total production capacity, which represents the production of about 7-8 million tonnes of iron ore per year.

The dam, owned by Samarco – controlled by Vale and BHP – burst, releasing 39.2 million cubic meters of tailings waste in the Rio Doce Basin, killing 19 people. It was considered Brazil’s worst environmental disaster.

The company estimates that in 2029 it should reach a production scale between 22 million and 24 million tonnes of iron ore per year, the same level as before the tragedy.