By Gareth Aird, head of Australian economics at CBA:

Key Points:

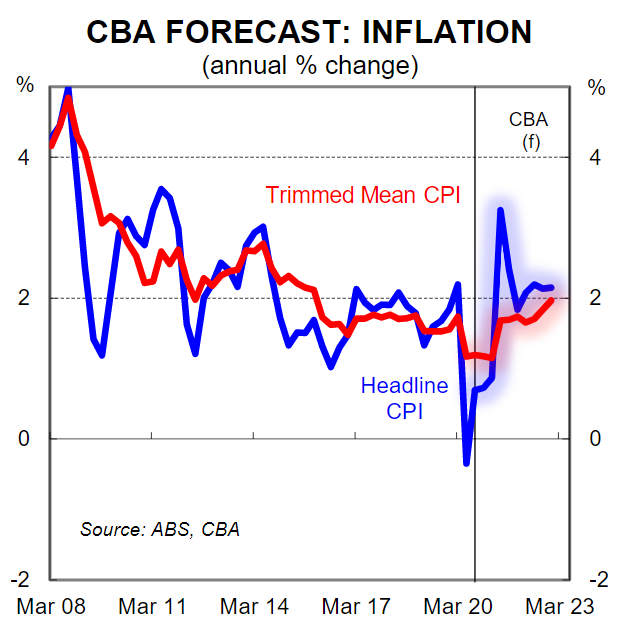

- We expect the headline CPI to increase by 0.9% in Q420 (+0.7%/yr).

- The trimmed mean CPI on our forecasts will print at +0.4% (+1.2%/yr).

- The inflation debate may heat up over 2021 as we expect some ‘demand-pull’ inflation to show up in the data.

Overview

The unique nature of theCOVID-19economic shock and the policy response to it means that the outlook for inflation is a little more uncertain than it has been in recent years. As a result, financial markets will be very much focussed on the quarterly CPI releases over 2021.

We have become very used to low and stable inflation in Australia (and globally). And whilst it appears at this stage that low inflation will continue, we do not think that it is assured just because the unemployment rate will be comfortably above the 4½%non-accelerating inflation rate of unemployment–the ‘NAIRU’. A strong consumer led recovery poses the risk of higher inflation, particularly if fiscal support continues to be large and the disparity between household incomeand wages growth remains wide. Indeed we expect to see some ‘demand-pull’ inflation show up in the data from here, albeit that is unlikely to lift underlying inflation back into the RBA’s target band over 2021.

The Q4 20 CPI

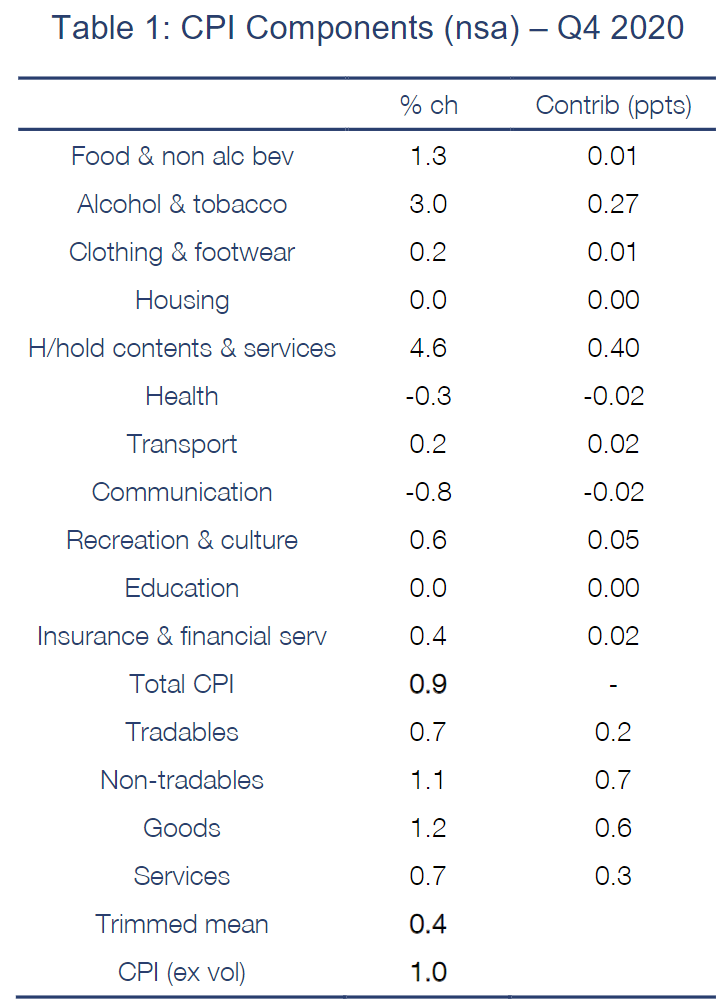

On Wednesday27 January the ABS will publish the Q420 CPI. We expect to see a solid 0.9% increase in headline inflation largely driven by: (i) child care returning to normal levels(it was free for 8 days in Q3 20); and (ii) a strong lift in tobacco prices due to the excise. Those two factors alone are anticipated to add 0.6ppts to the headline CPI.

Context of course is key. The Q2 20 CPI fell by 1.9%and only partially rebounded by 1.6% in Q3 20. So in annual terms a 0.9% increase in the quarterly rate over Q4 20 leaves headline inflation unchanged at just 0.7% (a 0.9% increase in Q4 19 drops out of the annual calculation).

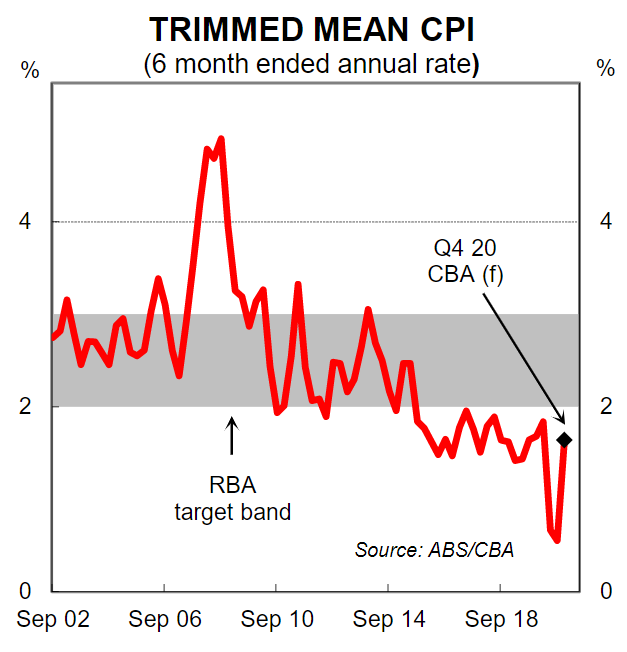

Underlying inflation is expected to remain low in the Q4 20 CPI. Our forecast is for the trimmed mean, the RBA’s preferred measure, to rise by 0.4% over the quarter. Such an outcome would see the annual pace of core inflation remain at just 1.2%. The six month annualised pace of underlying inflation on our figuring accelerates to 1.6%. See Table 1 opposite for our detailed forecasts for the Q420 CPI basket.

Inflation and the RBA

The RBA currently expects underlying inflation to remain well below their 2-3%/yr target over their forecast horizon which extends to end-2022. That is an uncomfortable place to be for an inflation targeting central bank. But we think the RBA has discounted the prospect of some demand-pull inflation too quickly. We believe that the RBA’s focus on cost-push inflation means their inflation forecasts are too low. As such, we expect underlying inflation to be higher than the RBA’s forecasts by end-2021 (CBA +1.7%/yr; RBA +1.0%/yr).

From a monetary policy perspective we think that the RBA will leave its inflation profile in the upcoming February Statement on Monetary Policy (SMP) largely unchanged (baring a big surprise in the Q4 20 CPI). Given the overall readings in the Q4 20 CPI are expected to remain low and the economy will still be operating well below the level of unemployment associated with full employment we expect the RBA to extend their bond purchases by $A100bn when the current $A100bn bond buying program (QE) is due to be completed in April. We do not expect them to announce any extension to QE at the February Board meeting. Rather it will come either at the March or April Board meeting.

The first RBA Board meeting for 2021 is on 2 February. Governor Philip Lowe is scheduled to deliver a speech on 3 February. And the February Statement on Monetary Policy(SMP) will be published on 5 February. We will publish our full monetary policy outlook piece in early February.