By Gareth Aird, head of Australian economics at CBA:

Key Points:

- With weak wages growth set to persist and some further appreciation of the Australian dollar expected, the outlook points to low inflation continuing over 2021.

- But our expectations for a strong consumer-led economic recovery means some demand-pull inflation is likely and the risk of underlying inflation pushing through2%/yr over 2021 is non-trivial.

- Financial markets will be on high alert if inflation surprises to the upside in 2021.

Overview:

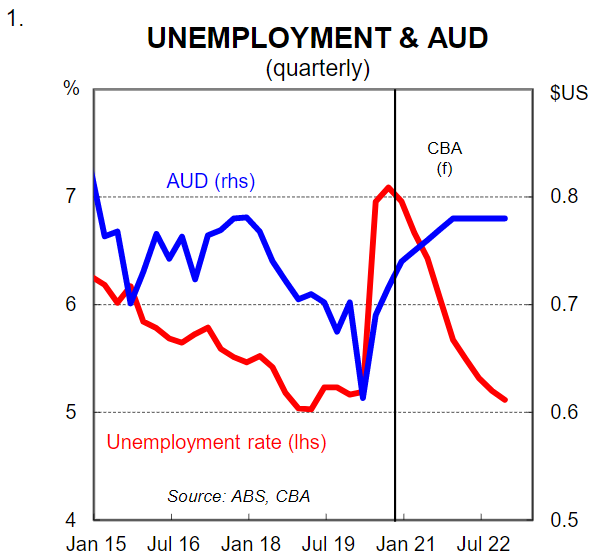

On the surface the rationale for low consumer price inflation to continue in 2021 appears straight forward. The economy will be operating with an output gap and that will mean weak wages growth (the unemployment rate will fall, but it will remain above the non-accelerating inflation rate of unemployment–the ‘NAIRU’). In addition we expect the Australian dollar to appreciate a little over 2021 which will put downward pressure on import costs (chart 1). So there will be little in the way of ‘cost-push’ inflation.

However, we think the inflation outlook is a little more complicated. The unique nature of theCOVID-19economic shock and the policy response means that we are likely to see some ‘demand-pull’ inflation in 2021. It may not be broad-based, but it could be enough to see inflation step up a little and that could make financial markets edgy.

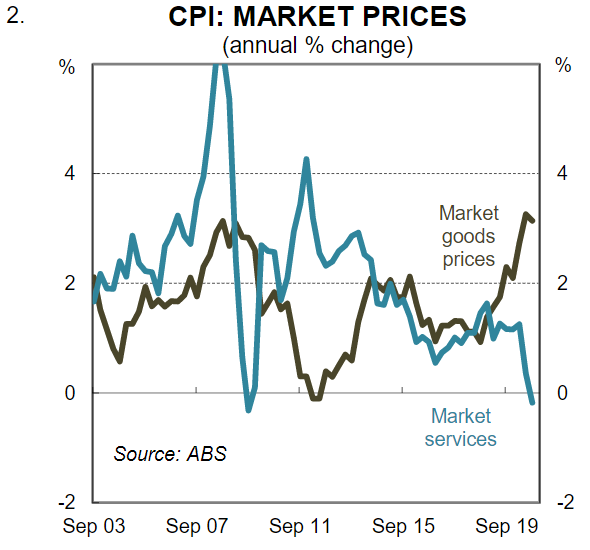

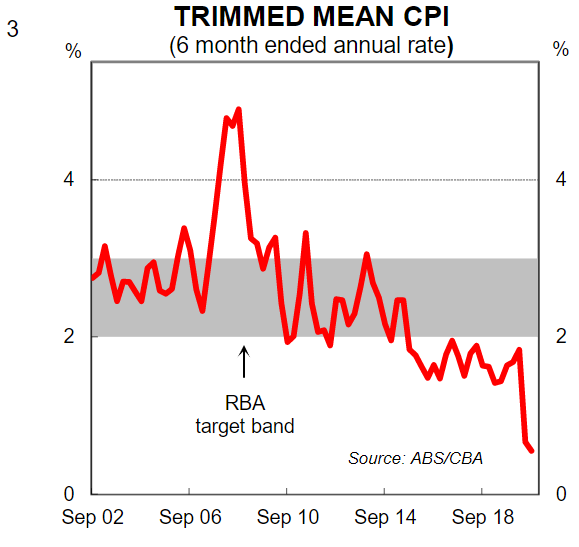

There were some components of the Q3 20 CPI that gave us a taste of what could be more widespread in 2021. The prices of a number of goods rose quite sharply due to a spike in aggregate demand. As a result, market goods inflation stepped up (chart 2). To be clear, overall inflation has so far been low (chart 3). But there have been some upward movements in the prices of some goods over the COVID-19 period that means it is prudent to take a deeper dive into the inflation outlook.

In this note we consider the case for and against higher inflation in 2021 from both a cost-push and a demand-pull perspective. On balance we believe that the cost-push story will be the dominant driver of inflation outcomes and we expect only a partial offset from some demand-pull inflation. This means that our central scenario is for low inflation to continue in 2021.

However, we expect underlying inflation to be higher than the RBA’s forecasts by end-2021 (CBA +1.7%/yr; RBA +1.0%/yr). And there is a non-trivial risk that 6-month annualised core inflation pushes through the key 2% watermark at some stage in 2021. Such an outcome would cause some discomfort in financial markets, particularly fixed income markets.

We have become very used to low and stable inflation in Australia (and globally). And whilst it appears at this stage that low inflation will continue, we do not think that it is assured just because the unemployment rate will be comfortably above the 4½% NAIRU. A strong consumer led recovery poses the risk of higher inflation, particularly if fiscal support continues to be large and the disparity between household income and wages growth remains wide.

The case for low inflation

Wages growth, import costs and inflation expectations are generally key inputs into inflation models. Indeed one of the inflation models that we have largely relied on in the past uses these three inputs, with various lags, to forecast inflation. This model of course requires us to take a view on the future path of wages growth as well as the Australian dollar. But at this juncture that seems relatively straight forward. Wages growth will remain low over the next few years because of spare capacity in the labour market. We expect both the unemployment and underemployment rates to fall as GDP rises and job creation follows. But it will take a few years before the labour market has tightened sufficiently for any broad-based wages growth to emerge. As such we expect wages growth to be ~1.0% in 2021. This will keep a lid on production costs (unit labour costs of course being a key part of the cost of production, particularly in the services sector).

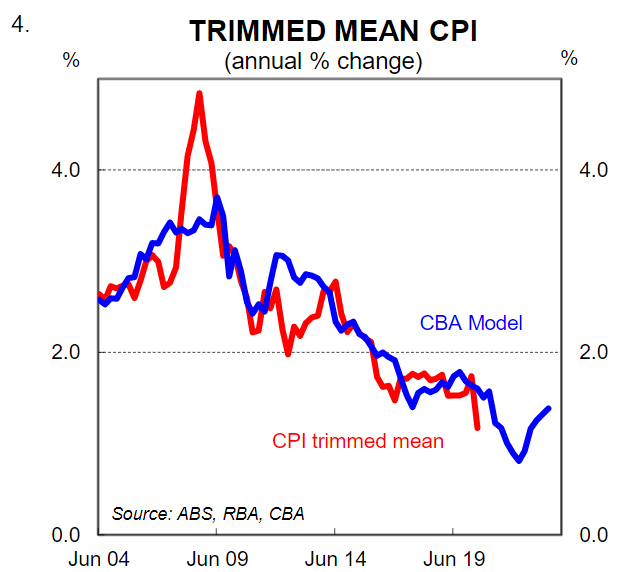

Our forecast for the AUD to appreciate to $US0.78 by end-2021 means that imported inflation is also likely to remain low, notwithstanding any upward movements in commodity prices. And finally inflation expectations remain low. So overall the model we have previously used to estimate core inflation points to inflation remaining low and for the trimmed mean to print around 1%/yr by end-2021(chart 4). This is very much in line with the RBA’s forecast for underlying inflation.

All models, however, have limitations. And the inadequacies of models to predict the future are most evident during a big economic shock or ‘black swan’ event. As such, we are not taking a literal read of our previously used inflation model to forecast inflation in 2021. Rather we are using it as starting point and have over layed other factors, as discussed below.

The case for higher inflation

Cost-push inflation is not the only type of inflation to consider. Demand-pull inflation, which is the increase in aggregate demand, categorised by the four sections of the economy: households, business, government, and foreign buyers, is the other key type of inflation.

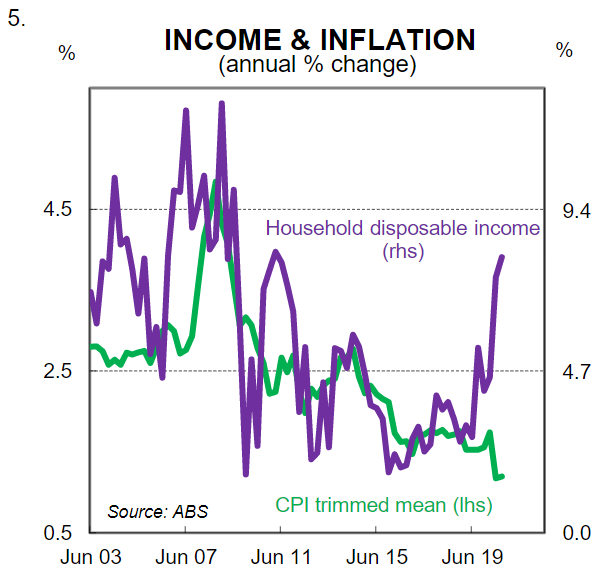

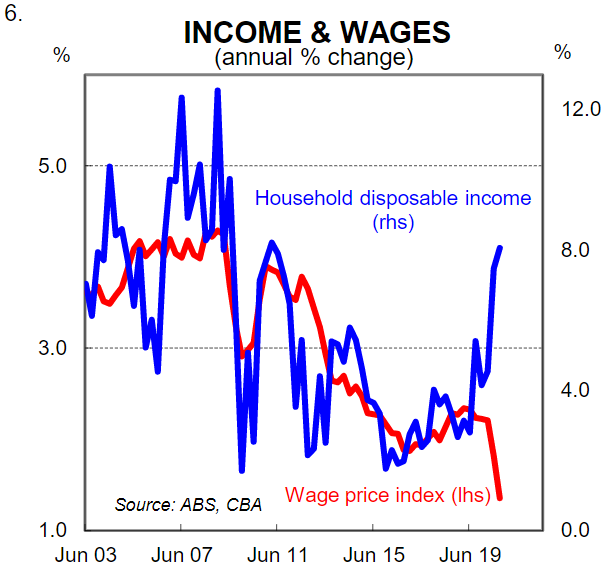

It is harder to model demand-pull inflation, but we think a good starting point is to have a look at the relationship between household disposable income and inflation. We do this because changes in household disposable income capture changes in the spending power of the household sector. The analysis shows that there’s been a pretty close relationship historically between growth in household disposable income and consumer price inflation (chart 5). That is largely because household disposable income and wages have tended to be closely positively correlated (chart 6).

Over the COVID-19 period, however, things look very different. The huge fiscal injection of cash into the household sector has seen household disposable income surge. But wages inflation has been weak. Therefore running an inflation model that has only wages growth as an input will be capturing changes in the cost of production for a business (i.e. cost-push inflation). But it will not be capturing the huge lift in household income that has increased the purchasing power of households and could contribute to demand-pull inflation.

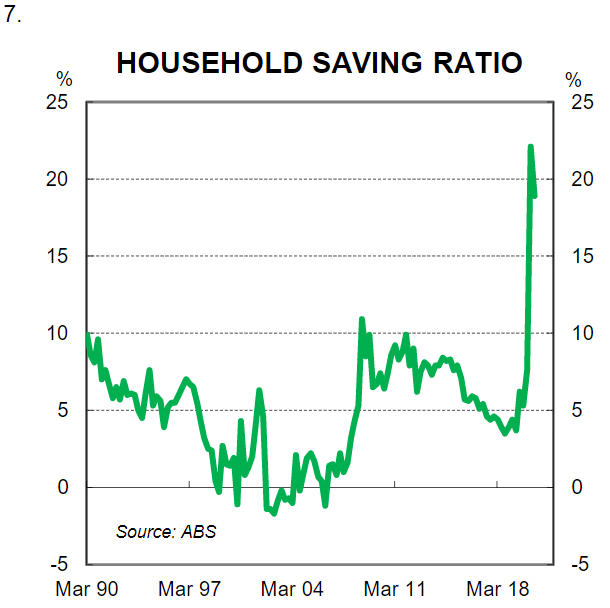

Indeed as it currently stands that purchasing power has not been fully realised. That is because a lot of the income that has been channelled into the household sector has been saved due to COVID-19 restrictions (chart 7). On our calculations the Australian household sector has built up in excess of $A100bn (5% of GDP) in additional savings that have been accrued since COVID-19 arrived in Australia – this excludes the early withdrawal of superannuation of ~$A36bn. An expected drawdown of some of these savings due to the elevated level of consumer sentiment and a willingness to spend will see the demand for certain goods and services lift. It is reasonable to assume that as this happens some businesses will lift the prices of the goods and services they are selling where there is higher demand.

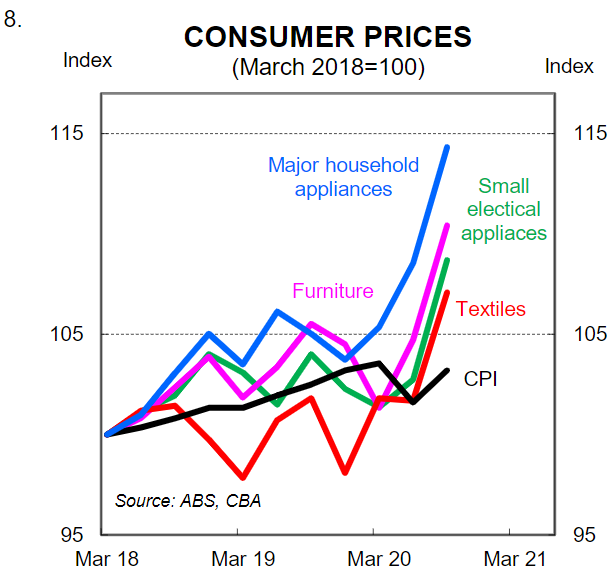

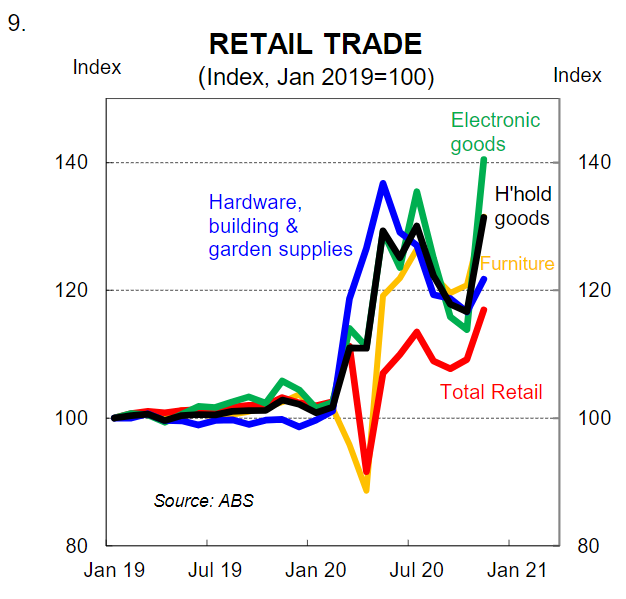

There is evidence that this has been happening already over the COVID-19 period. Prices for furniture, textiles, major household appliances and small electrical appliances have all risen very sharply since Q1 20 (chart 8). And this is where there has been a strong lift in consumer demand (chart 9).

The interesting aspect of any drawdown in savings is that additional spending creates new income –one person’s spending is another person’s income. When a consumer buys a meal at a restaurant or gets a haircut the money spent ends up as income to the restaurateur or the hairdresser. So any drawdown of savings will boost income simultaneously. This will create a positive feedback loop that will support aggregate demand in the economy. Materially higher prices therefore in 2021 for some goods and services is a distinct possibility. Indeed we expect to see strong price rises in some pockets of the CPI basket. The key question for us is around whether there will be enough demand-pull inflation to see overall inflation rise.

Our forecasts

In determining the extent to which demand-pull inflation is likely to lift the CPI in the absence of cost-push inflation it is helpful to look at the composition of the CPI basket.

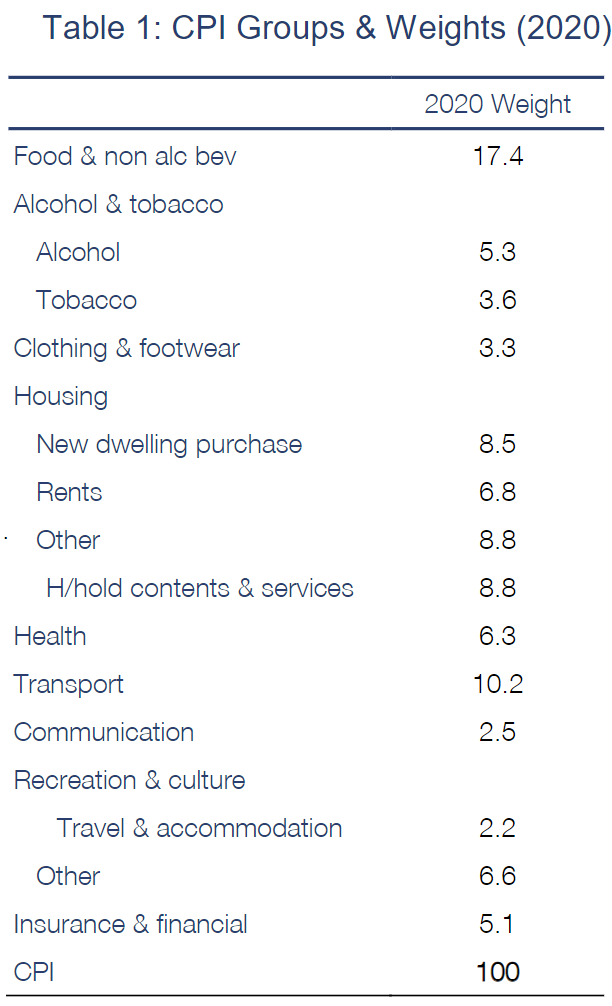

Table 1 lists the key CPI groups and their relative weightings (incorporating the new 2020 weight update). The areas that standout to us as being the most likely to display some demand-pull inflation are food, alcohol, the new dwelling purchase component of housing, and recreation & culture. These goods and services collectively account for ~40% of the CPI which is significant. However, working the other way is a number of goods and services in the CPI basket that will exert a disinflationary force on the CPI. Some of these expenditure groups, like communication, have been falling for years. But some will be new. Housing rents stand out to us as a component of the CPI that will fall in 2021 and that is unusual historically (rising vacancy rates will drive rents lower). So as always there will be a variety of forces that are influencing price outcomes across the various groups in the CPI basket.

On balance we estimate that demand-pull inflation could lift underlying inflation by 0.7ppts in 2021above what ‘modelled’ inflation signals. As such our central scenario sees the trimmed mean at 1.7%/yr at end-2021 (0.7ppts above the RBA’s forecast). We expect headline inflation to be tracking at 2%/yr over H2 21 – big rises in tobacco prices due to the excise explain the bulk of the disparity between headline and underlying inflation. Base effects will also play a role in 2021 on the annual headline rate due to some unusual things happening to the CPI basket in 2020 (temporarily free childcare in Q2 2020 is the main culprit).

Whilst our inflation profile tracks higher than the RBA’s it is still pointing towards relatively low inflation continuing. However, we think the risks are to the upside. Our base case takes into account some demand-pull inflation, but it could be stronger than we have pencilled in. The fiscal response to COVID-19 has simply been incredible and the household sector is cashed up. The timetable of the COVID-19 vaccine rollout in Australia will be critical to the pace of the economic recovery in 2021. If the domestic economy has clear air from COVID-19 in H2 21 with interstate borders fully open, no social distancing requirements and the risk of the reimposition of lockdown measures negligible we will likely upwardly revise our inflation forecasts. Financial markets are very used to low and stable inflation and nominal bond yields imply low inflation is here forever. Fixed income markets are likely to get edgy if underlying inflation surprises to the upside. We think there is a clear risk of that happening in 2021 even with the economy operating with an output gap.

Monetary policy implications

From a monetary policy perspective we think that the RBA will leave its inflation profile in the upcoming February Statement on Monetary Policy(SMP) largely unchanged. But as the year unfolds we expect them to modestly upwardly revise their profile for inflation as the economic data leaves them with little choice. In one sense the RBA’s inflation forecasts are now less relevant in their decision making because, as Governor Philip Lowe stated in a speech in October 2020, they are now, “putting a greater weight on actual, not forecast, inflation in our decision-making.” But their inflation forecasts will stay play a role in their forward guidance.

Over H2 20 the RBA provided explicit forward guidance by stating that “the Board does not expect to increase the cash rate for at least 3 years.” But that line cannot be repeated indefinitely for it is always at least 3 more years from whenever it is last said. At some stage in the future as the labour market continues to tighten and inflation lifts a little the RBA Board will no longer continue to say that the cash rate is on hold for a further 3 years. When that happens the RBA will need to do something about the target yield on the 3yr Australian Commonwealth Government Bond (ACGB) – currently 0.1% which is the same as the cash rate target. More specifically, they will need to either remove the target or lift the target yield. We had been of the view that this could happen by the middle of 2021 based on our forecasts for the unemployment rate. But the reimposition of restrictions in a number of jurisdictions over the past month because of some community transmission of COVID-19 means that we hold that view with less conviction now.

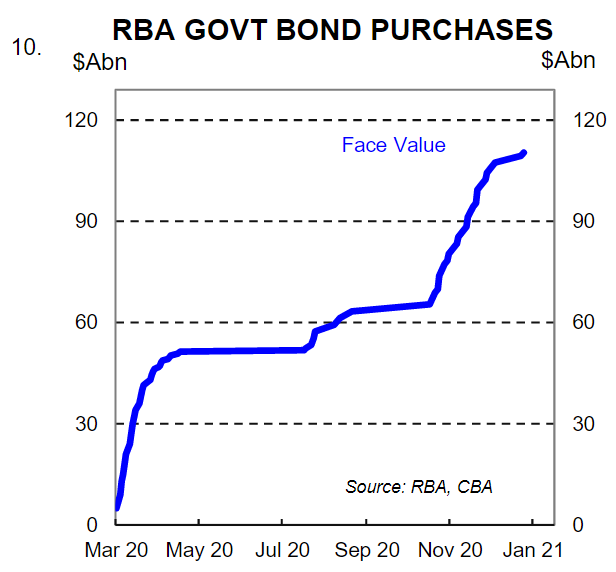

In any event, markets will likely be more focussed at the moment on what the RBA will do from April when the current $A100 bn bond buying program (QE) is due to be completed (chart 10). On that score, we expect an extension of QE and for the RBA to commit to buying a further $A100bn of government bonds (both Commonwealth and Semi-Government –the mix may change a little from the current 80/20 split).

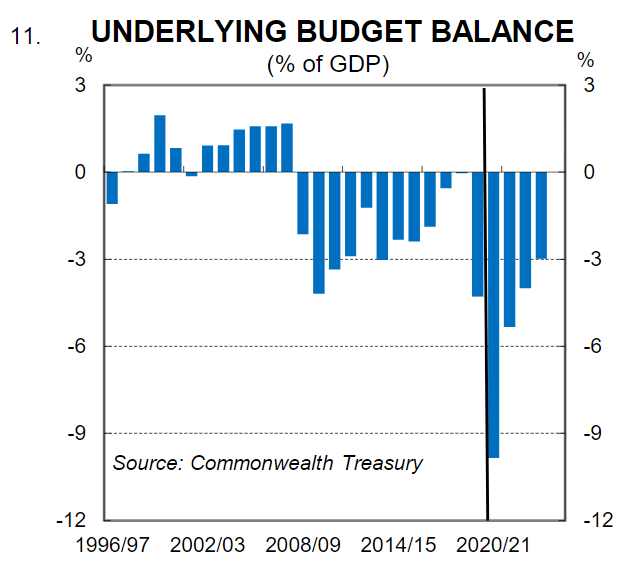

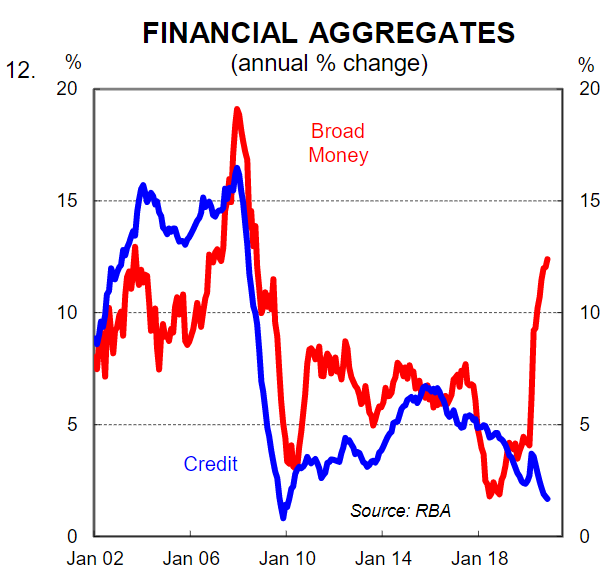

Overall the inflation story is very much one to watch in 2021. Markets may be faced with digesting the competing forces of more RBA bond buying against some upside inflation surprises. And as we move forward from here more generally the dynamics around inflation are likely to move in a way that means it is no longer sufficient to look at the inflation outlook via a pure ‘modelled’ lens. The medium term outlook for inflation should be considered in the context of the intersection of monetary policy and fiscal policy and how that pertains to monetary financing). Put another way, ongoing big fiscal deficits funded via the printing press which boosts the money supply could be a recipe for higher inflation (charts 11 and 12).

For RBA watchers the first RBA Board meeting for 2021 is on 2 February. Governor Philip Lowe is scheduled to deliver a speech on 3 February. And the February Statement on Monetary Policy (SMP) will be published on 5 February. We will publish our full monetary policy outlook piece in early February.