By Gareth Aird, Head of Australian Economics at CBA:

Key points:

- Growth in household income has inched higher over the past few months despite the two-staged tapering of the JobKeeper and JobSeeker payments.

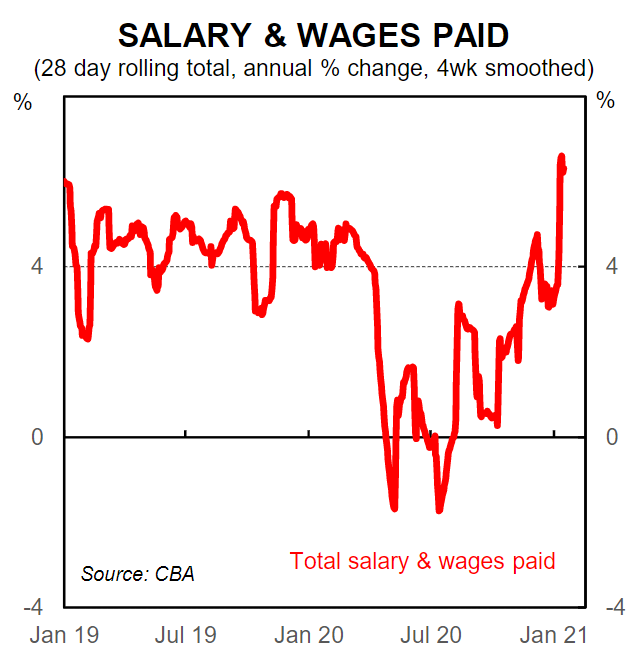

- Growth in salary and wages paid into CBA bank accounts has lifted materially over recent months reflecting strong growth in employment, hours worked and the personal income tax cuts.

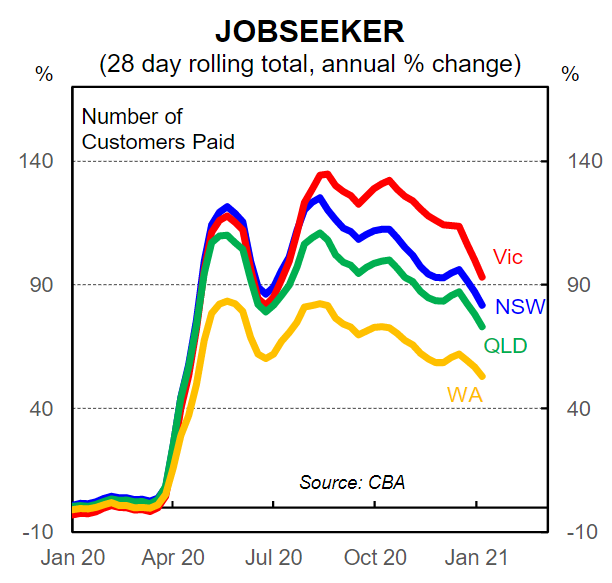

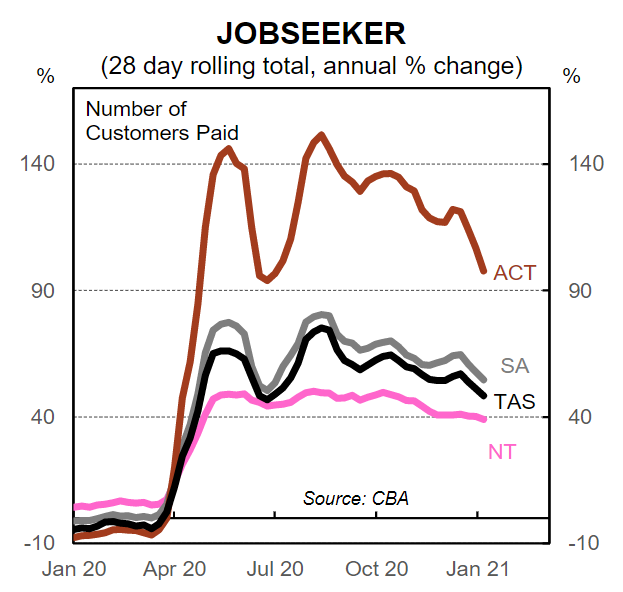

- The number of people receiving JobSeeker continues to fall as the labour market improves.

- There has so far been a seamless transition away from public support as the economy improves, but any further lockdowns and/or the reimposition of restrictions will be more damaging from Q2 21 without further public support for businesses and their employees (JobKeeper is currently due to expire on 28 March 2021).

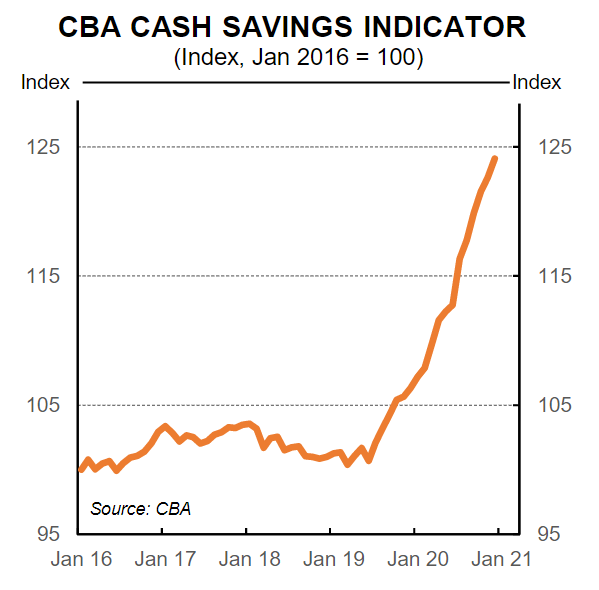

- The average total savings balance per household continues to rise sharply and the huge amount of savings accrued by the household sector will be a key source of support for household consumption in 2021.

- We retain our view for GDP to increase by a strong 4.2% in 2021 and 3.8% in 2022.

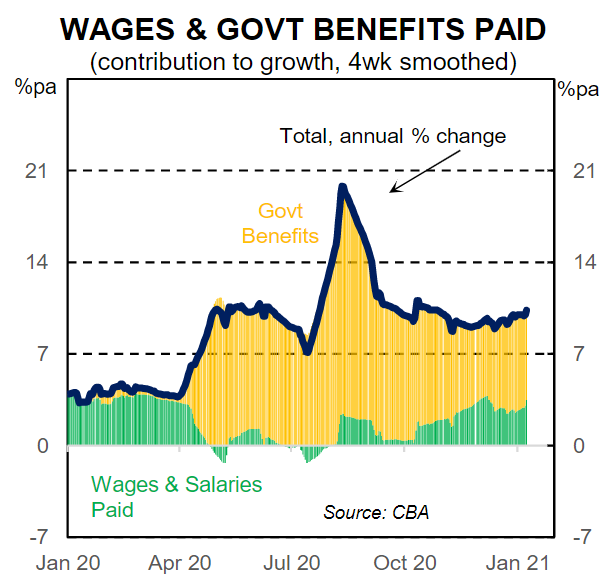

Annual growth in wages and salaries paid into CBA bank accounts has accelerated sharply over the past few months(latest w/e 15 January). The positive impact of a lift in employment and hours worked coupled with personal income tax cuts has more than offset the reduction in JobKeeper payments.

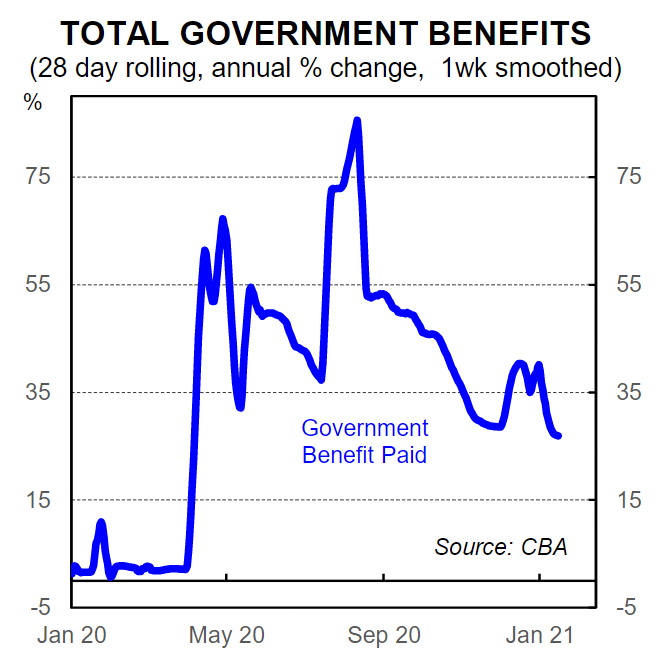

Growth in government benefit payments has eased primarily because: (i) the number of people receiving the JobSeeker payment has declined; and (ii) the ‘coronavirus supplement’ has been reduced in a two-step fashion (it was lowered from $A550 per fortnight to $A250 per fortnight in Q4 20and to $A150 per fortnight in Q1 21).

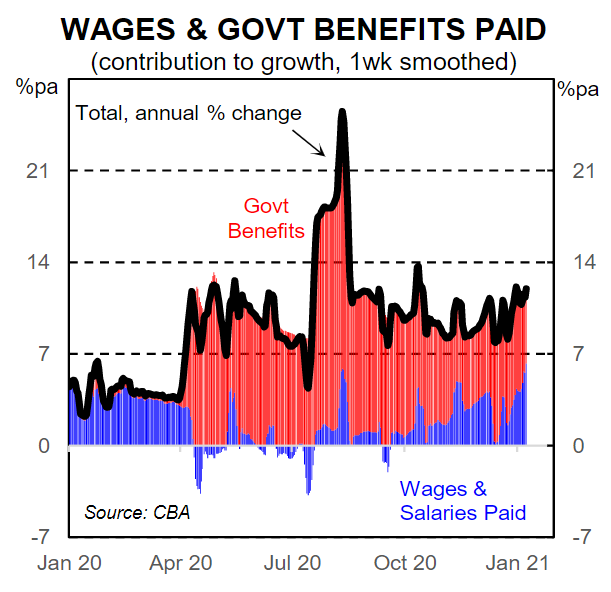

Overall growth in wages & salaries paid plus government payments oscillated around 10%/yr over Q4 20 –well above pre-COVID levels. Strong growth in household income has continued over the first half of January (latest w/e 15 January).

Our 4wk smoothed calculation on wages & salaries paid plus government benefits indicates a gentle upward trend in household income growth over the past few months. So far policy settings on income support seem very well calibrated.

The number of people receiving JobSeeker continues to fall across the board as the labour market tightens and more people return to paid work.

Most of the smaller states along with the NT have had smaller proportionate increases in the number of people receiving JobSeeker. The ACT is the exception where there was a big increase in the proportion of people receiving JobSeeker.

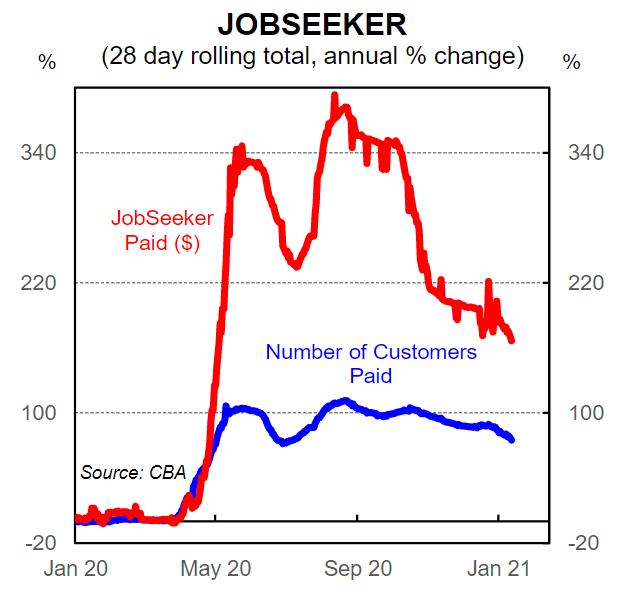

The reduction in the ‘coronavirus supplement’ was accompanied with an increase in the income free threshold. From Q4 20 someone receiving JobSeeker has been able to earn up to $A300 per fortnight and still receive JobSeeker in full – previously it was $A106 or $A143 per fortnight depending on age.

The disparity between household income growth and spending has generated a massive increase in savings. The CBA average total savings balance per household, including home lending related savings and transaction or savings accounts, was up a whopping 16.7%/yr at December 2020. The early withdrawal of super has also contributed to the lift in the stock of savings.