By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The Australian economy staged a remarkable recovery over the second half of 2020 and we expect strong economic growth to continue over the next two years.

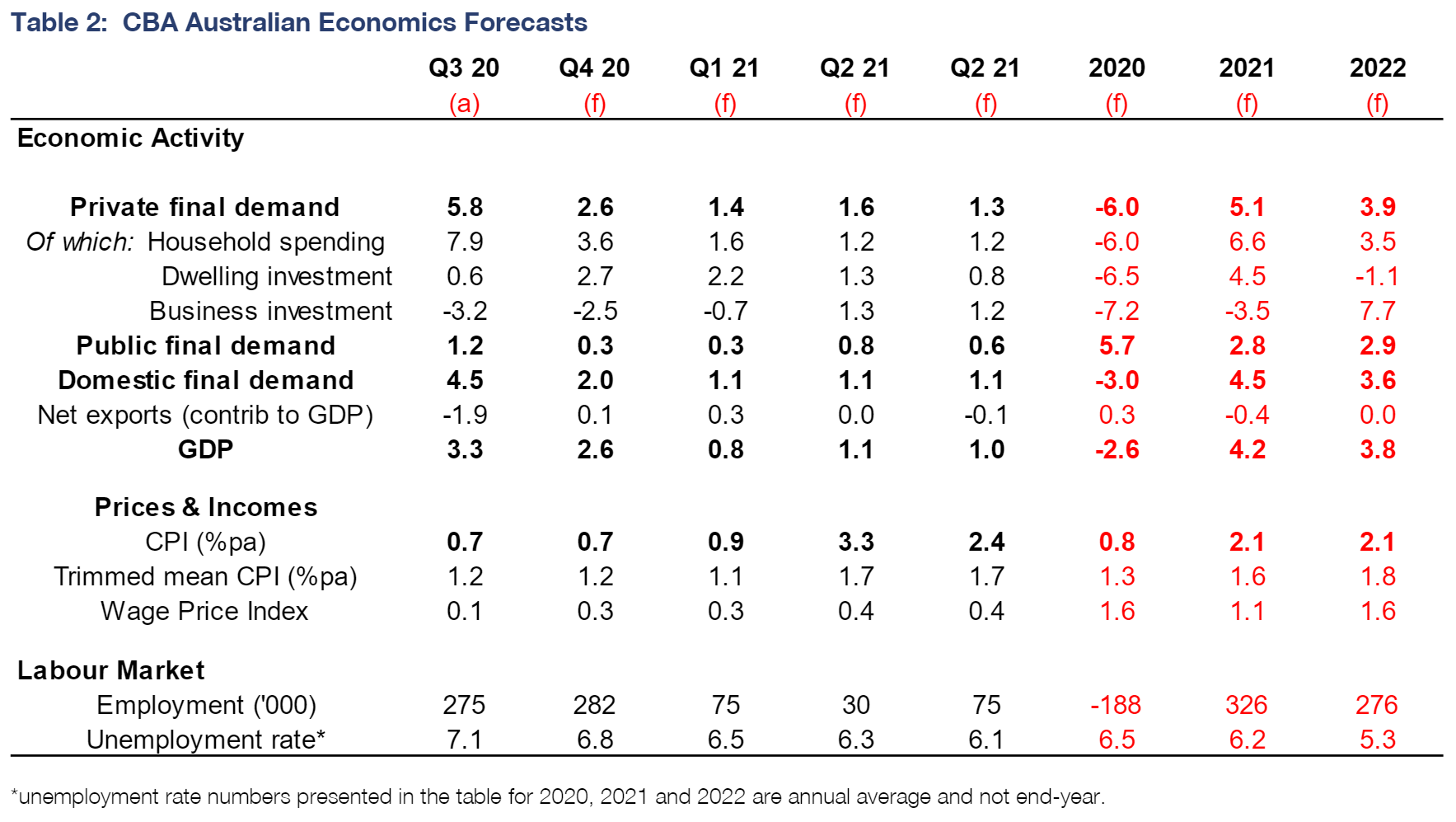

- We retain our view for GDP growth of 4.2% in 2021and 3.8% in 2022 but upgrade our forecast for Q4 20 GDP which raises the level of our GDP profile.

- We expect the unemployment rate to be 5.7% at end-2021 and 5.0% at end-2022.

- Fiscal and monetary policy support remain critical to the recovery and we expect the RBA to extend its government bond buying program by a further $A100bn.

Overview:

The economic shock induced by COVID-19 and the policy response to it is unparalleled. Government interventions in the economy have been radical by historical standards. And swings in the economic data over a relatively short period of time have been incredible. Indeed charting the economy over the COVID-19 period gives the impression that the economy has been under the influence of a remote control. The play, pause, slow motion and fast forward buttons have all featured!

The strategy of turning on and off large parts of the economy to stop the spread of COVID-19 meant there needed to be an almighty policy response to hold the economic machine together. And that is exactly what we got from the monetary and fiscal authorities. Support from industry, particularly the banking sector, has also played a key role in supporting the economy.

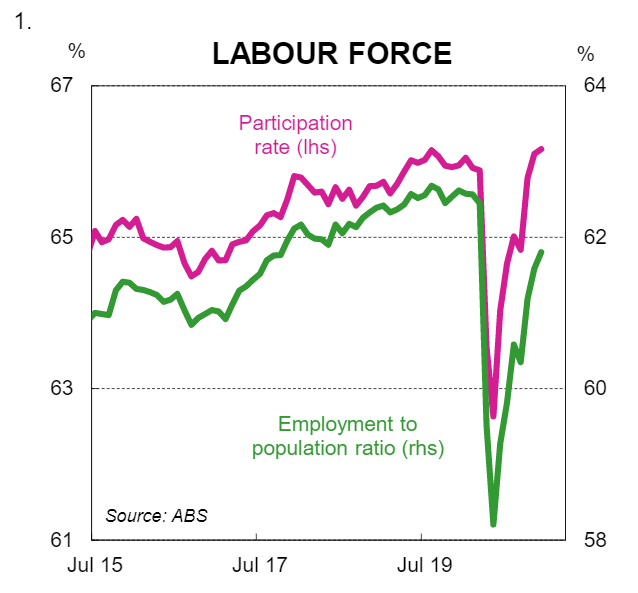

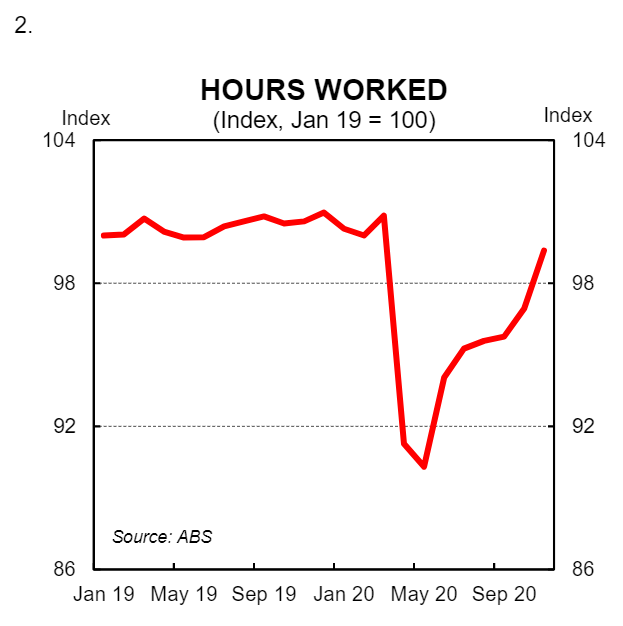

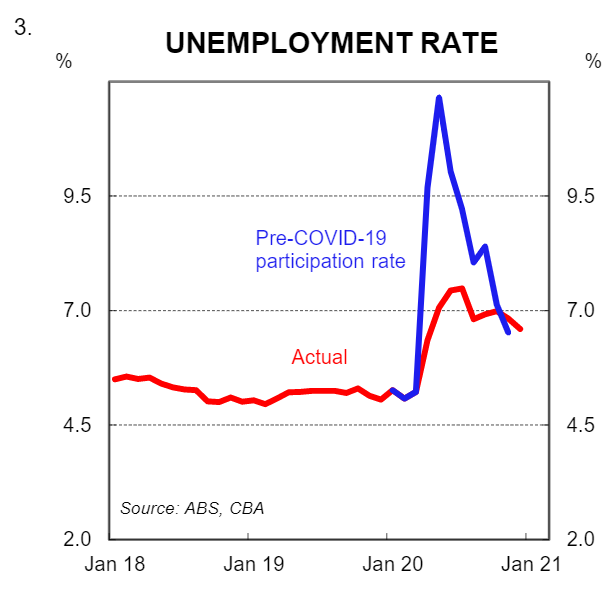

In an overall sense policymakers have so far been very successful in managing both the health and economic outcomes. COVID-19 cases in Australia have been very low and remain low. And the domestic economy staged a strong recovery over the second half of 2020 that was a lot better than most forecasters expected. So far our optimistic take on the economic recovery has been validated. Indeed the labour market data at the national level indicates that the recovery has essentially been V-shaped (chart 1,2 & 3).

The re-emergence of COVID-19 clusters in some states in late December 2020and the reimposition of restrictions and interstate border closures was a stark reminder that the virus has not gone away and we are not out of the woods yet. It also means that we may see some air pockets in the economic data over H1 2021 if more clusters of the virus surface. But we don’t expect the economic recovery to be derailed, particularly given that the COVID-19 vaccine rollout in Australia is due to begin shortly. Indeed the domestic economy could be booming in the second half of the year if the vaccination schedule is successful and the economy has clear air.

Policymakers spoke often over 2020 about the need to build a metaphorical ‘bridge’ to take us to the other side. But generally speaking nobody knew how long or wide the ‘bridge’ needed to be. Things look a lot clearer today. We begin 2021 with increasing clarity on a COVID-19 vaccination rollout which means we have a much clearer picture of when we will be on the other side.

In this note we discuss the Australian economic outlook. Regular readers will know that we have been constructive on the economy through the COVID-19period and we have not shifted that stance. We retain our above consensus central scenario we put forward in November last year for GDP growth to be 4.2% in 2021and 3.8% in 2022. But we upgrade our forecast for GDP in 2020 to a contraction of 2.6% (versus 2.8% previously). This means that we expect the level of GDP to be a little higher in 2021 than previously anticipated. We expect the unemployment rate to be 5.7% by end-2021. Growth comfortably above trend is expected to continue in 2022 and the output gap is likely to be closed by the end of 2022,when we expect the unemployment rate to be 5.0%.

COVID-19 vaccinations to begin in February

For the bulk of Q4 20 it felt like the threat of COVID-19 had all but disappeared in Australia. Community transmission of the virus was non-existent and by design or default a successful elimination strategy had been achieved. This meant that restrictions in all states were largely eased in entirety, and interstate borders were open. The festive season was set to see consumer spending surge after a strong November, and domestic tourism was likely to boom over the holiday period. Elimination, however, proved temporary. A‘COVID cluster’ on Sydney’s Northern Beaches emerged in mid-December that spread to a few other jurisdictions. The policy response was to reimpose restrictions, introduce localised lockdowns and put in place border closures.

The reimposition of restrictions put a dampener on Christmas for many Australian households and businesses. But the COVID-related news has not been all one way. Crucially the news around a vaccine has been positive. In early January the Federal Government announced a COVID-19 vaccine national rollout strategy that is expected to begin in mid-February this year(six weeks earlier than the Government originally anticipated). Up to 680k people are set to receive the first lot of vaccinations. That group includes quarantine and border workers, frontline health workers, and aged care and disability staff and residents. The Government expects the vaccination rollout to be completed by the end of October 2021.

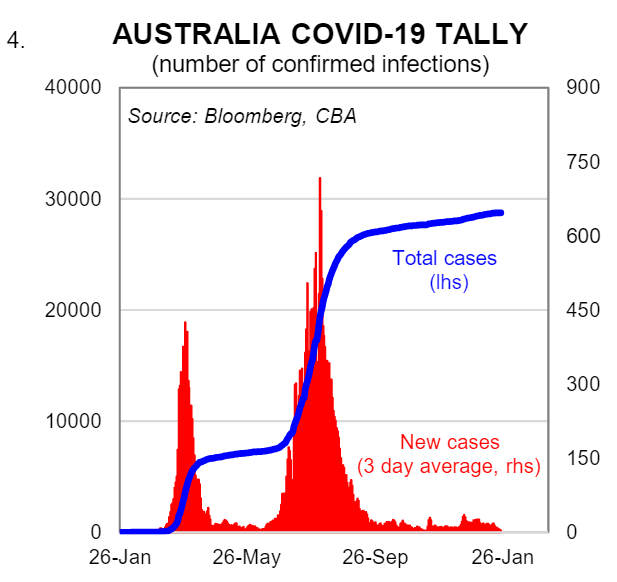

The full rollout of the COVID-19 vaccination is a ‘game changer’ as far as the economic outlook goes and the impact that the virus is having on the economy. A vaccine does not mean that COVID-19 will disappear. But it will spell the end of lockdowns and domestic COVID-related restrictions. In short, the Australian economy will have clear air once the rollout is complete and the very thing that has been holding the economy back will no longer be an issue. It is likely, however, that restrictions will remain in place on international borders for a limited time after the rollout is complete. But that is not particularly problematic as far as the economic recovery goes. The Australian economy essentially has to negotiate around 9 months of potentially choppy waters before it is smooth sailing. We say ‘potentially’ as the calmer economic waters that were with us over the bulk of Q4 20 may very well return. At the time of publication Australia has gone 11 days free from community transmission of COVID-19 and authorities once again seem to have engineered an outcome that means the threat of catching the virus is incredibly low (chart 4). As a result, a number of the current restrictions that remain in play are likely to be eased shortly. In summary, we expect the domestic economy to continue to recover well through 2021 before the vaccine rollout is complete provided any outbreaks are traced and well contained and significant restrictions are not reimposed for an extended period.

Consumers retain an optimistic outlook

The household perception of the economy is a key driver around consumer decisions to spend or save. Confident consumers are more likely to spend income, while cautious consumers are more likely to save it. That relationship has decoupled slightly over the COVID period because of restrictions which limit the ability of households to spend on a range of goods and services at various times, regardless of how they feel. But in general confidence and spending decisions are aligned.

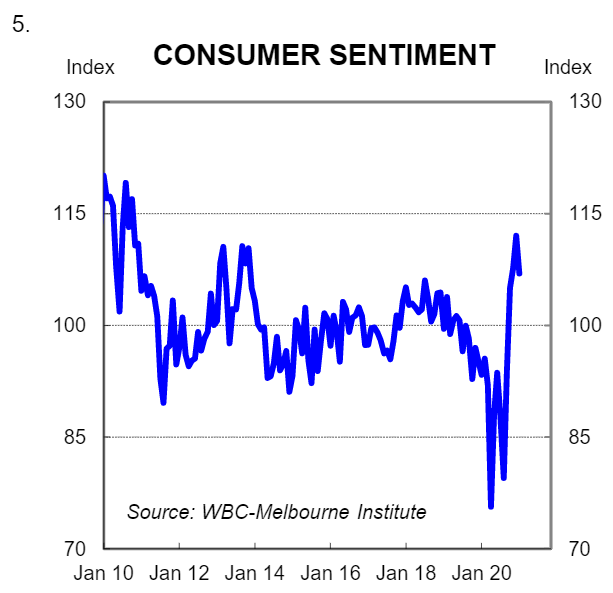

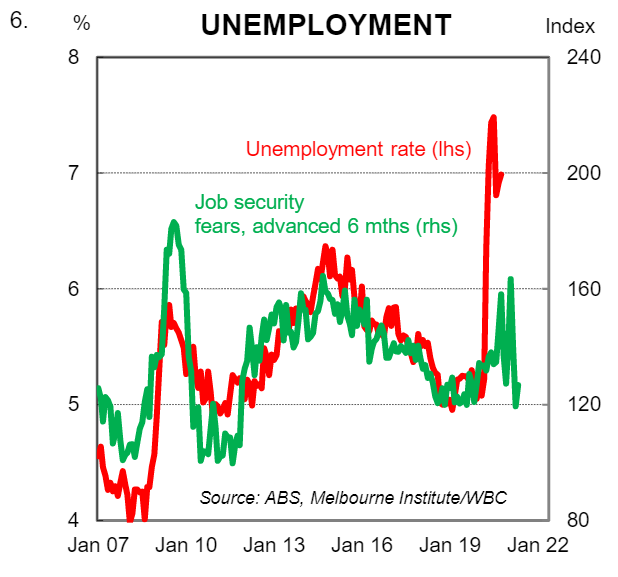

The latest read on the WBC/Melbourne Institute monthly consumer sentiment report is particularly encouraging. According to the January survey confidence dipped, but the headline index printed at 107 which is well above the key 100 watermark level that separates optimists from pessimists (chart 5). It is also well above the long run average level of 101. Confidence had lifted to a 10yr high in December. And despite the negative news around some ‘COVID clusters’, the reimposition of restrictions and interstate border closures, consumer confidence only retreated to its November level which at the time was a 7yr high. For context, confidence in January 2021 was 14.6% higher on year ago levels while job security fears sit at below pre-COVID levels (chart 6).

It looks to us like households are focussed on the bigger picture. Namely that the COVID-19 vaccination rollout is imminent and a return to pre-COVID life will occur in H2 21. Consumers are cognisant of the incredible fiscal and monetary support that has been directed at the economic shock. And the policy stimulus coupled with light at the end of the tunnel is keeping confidence buoyant which will see ongoing strength in consumer spending.

Income and savings are still booming

One of the remarkable stories over the COVID-19 period has been around the big lift in household income and the surge in the stock of savings. We have been able to track these dynamics in real time by looking at payments going into CBA bank accounts and changes in the level of household deposits.

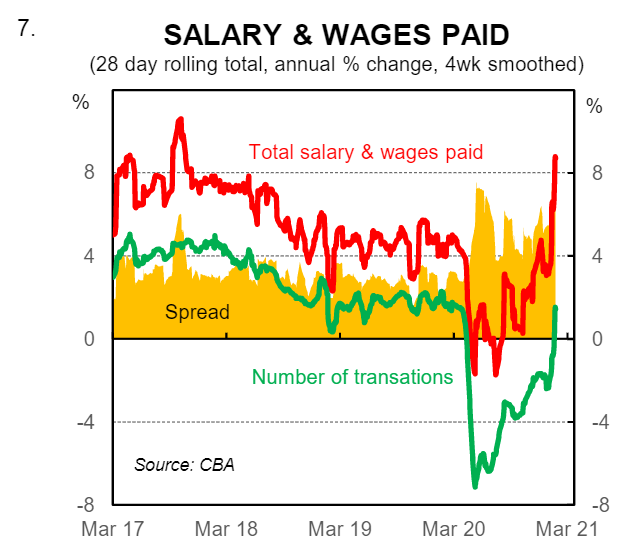

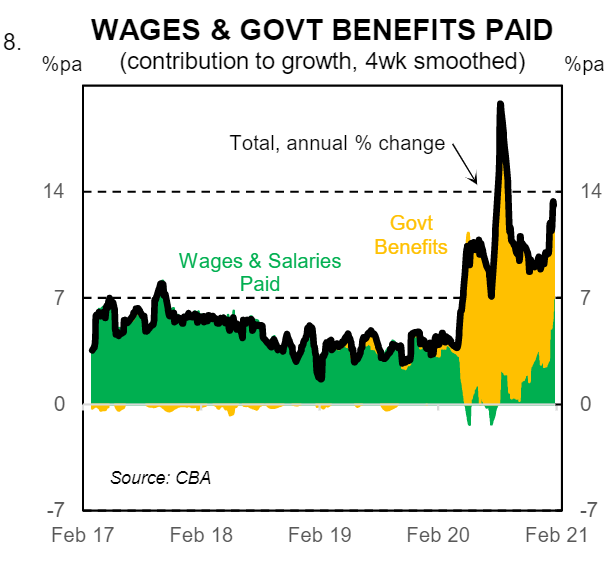

Our latest data, to the week ending 22 January, indicates that growth in household income has inched higher over the past few months despite the two-staged tapering of the JobKeeper and JobSeeker payments (chart 8). More specifically, growth in salary and wages paid into CBA bank accounts has lifted materially over recent months reflecting strong growth in employment, hours worked and the personal income tax cuts. At the same time, growth in government benefit payments has eased primarily because: (i) the number of people receiving the JobSeeker payment has declined; and (ii) the ‘coronavirus supplement’ has been reduced in a two-step fashion (it was lowered from $A550 per fortnight to $A250 per fortnight in Q4 20 and to $A150 per fortnight in Q1 21).

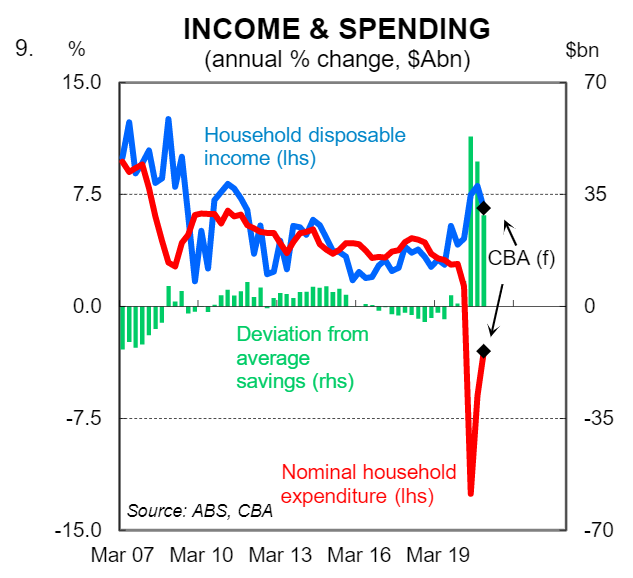

The positive shock to household income has been underway since Q2 20. And our most recent data indicates that it will remain in play throughout Q1 21. This means that a full year of significantly elevated growth in income will be clocked at the end of the March quarter. The surge in income coupled with less spending due to COVID-related restrictions has contributed to an unprecedented lift in savings.

Based on the Q320 national accounts, we estimate that $98bn or 5% of GDP was saved over the June and September quarters (over and above what is normally saved given the household sector is a net saver). Our forecasts for nominal household expenditure and gross household disposable income over Q4 20suggest a further spike in additional savings of $A27bn over the quarter (chart 9). This means that the Australian household sector is likely to have begun2021 with additional savings of around $A125bn or a little over 6% of GDP. These savings exclude the early withdrawal of superannuation and are calculated as the difference between income and expenditure less ‘normal savings’.

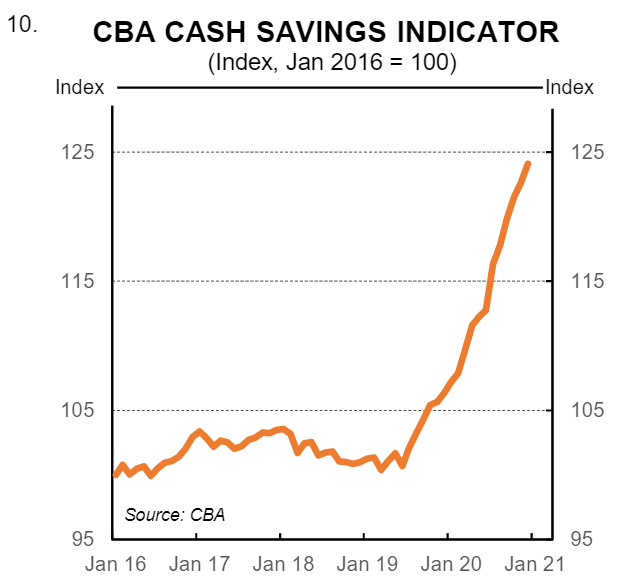

Our CBA cash savings indicator, which is based on the average total savings balance per household, including home lending related savings and transaction or savings accounts, captures the rapid accumulation of savings in the household sector. It has surged over the past eight months to sit 16.7% higher on year ago levels as at December 2020 (chart 10).

A partial drawdown in the accumulated stock of household savings will be a big tailwind on household consumption in 2021. And it will create a ripple effect through the economy. Any drawdown in savings to fund domestic spending creates new income in our economy–one person’s spending is another person’s income. When a consumer buys a meal at a restaurant or gets a haircut, the money spent ends up as income to the restaurateur or the hairdresser. So any drawdown of savings will boost income in the economy simultaneously. This will create a positive feedback loop that will support aggregate demand and job creation.

The housing market will support the economy

Australia’s housing market and the economy are very much interconnected. Residential real estate is Australia’s largest asset class and the stock was estimated to be worth ~$A7.3 trillion as at Q3 20. For the economic outlook the housing market matters both from a prices and turnover perspective. Rising dwelling prices influence economic activity indirectly via the wealth effect. And higher turnover in the housing market is positively correlated with household retail spending, particularly on durable goods such as furniture, home appliances and electrical or electronic devices.

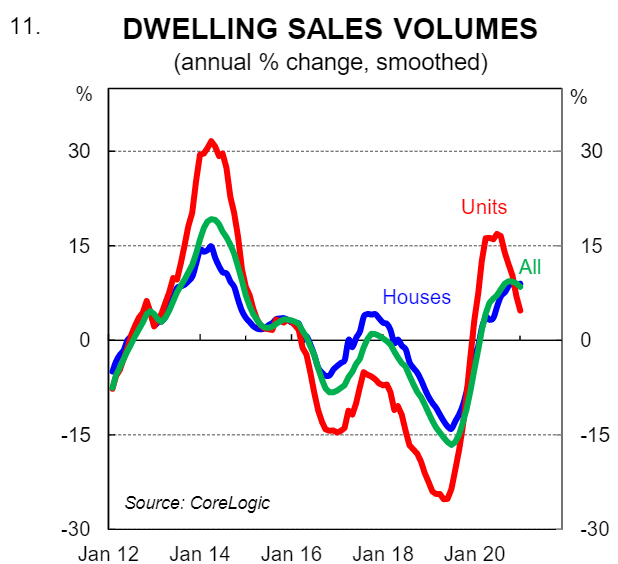

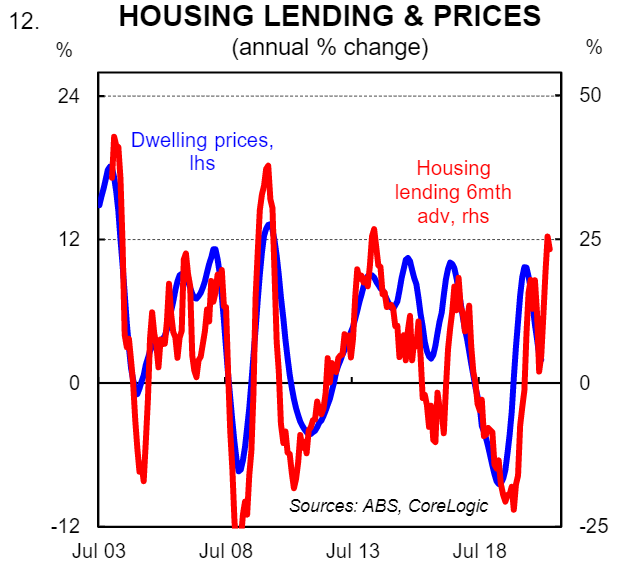

The most recent data shows that dwelling prices are rising in all capital cities. And turnover has picked up (chart 11). We expect these trends to continue over 2021. Lending to owner-occupiers and investors has lifted and this has historically been a reliable forward looking indicator of prices (chart 12). In addition, near term momentum indicators of the housing market have continued to strengthen and our home price model is signalling solid price rises over the next six months. Our forecast is for national dwelling prices to rise by 8% in 2021 (9% for houses vs 5% for apartments). This means that we expect a positive wealth effect to be at work over the year whereby rising home prices are a tailwind on household consumption.

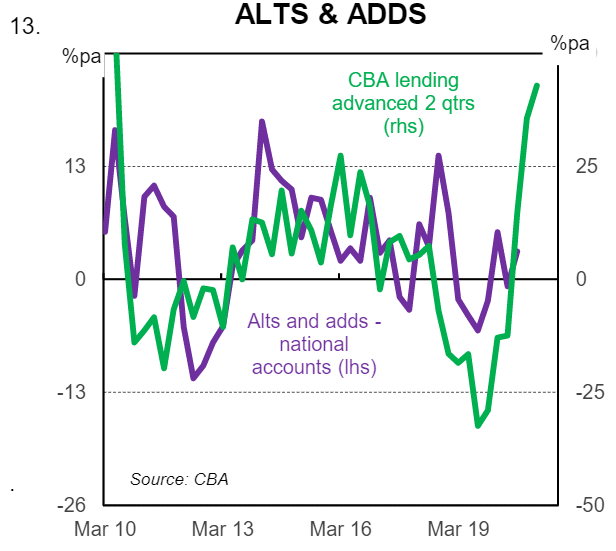

Housing construction will also support the economic recovery in the year ahead. Our lending data indicates there will be a big step up in alterations and additions which are worth 40% of total residential construction (chart 13). New dwelling investment will also make a positive contribution to growth in large part because of the success of the HomeBuilder scheme. Building approvals for houses have surged on the back of HomeBuilder and new dwelling investment is forecast to lift solidly over the year despite an expected drop in apartment construction.

Public capital works programs are huge

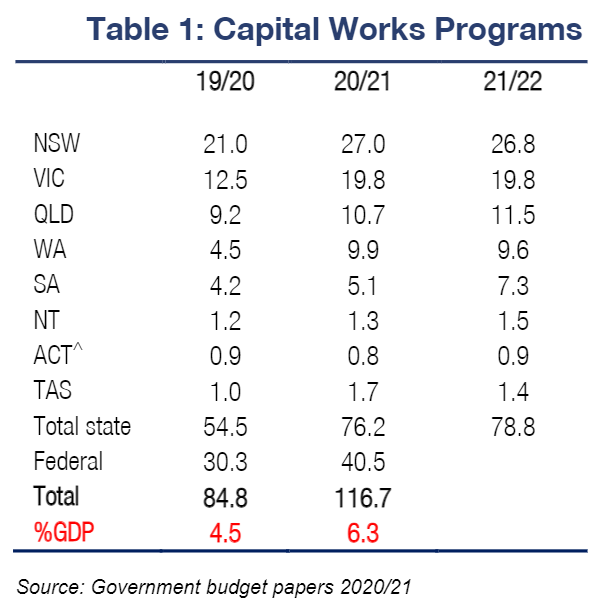

Federal and state governments have both responded to the COVID-19 economic shock by boosting capital works programs significantly. In some jurisdictions these programs were already large. Our bottom up analysis of the 2020 State and Federal Budgets indicates that public sector investment is planned to lift from 4.5% of GDP in 19/20 to 6.3% of GDP in 20/21 (Table 1).

Such an outcome would contribute a very large 1.7ppts to GDP in 20/21 and is nothing short of a boom. We suspect that such ambitious public capital works programs will not be fully delivered in the allotted timeframe and slippage will occur. That is not necessarily a bad thing. It will simply mean that big capital works programs will support the economy over both 2021 and 2022. And it means that there will not be a sharp drag on the economy as projects are completed.

What about the expiry of JobKeeper?

The key near term risk for the Australian economy is the expiry of JobKeeper. Without any policy amendments the JobKeeper program will finish on 28 March 2021. This means that currently eligible businesses will no longer receive the wage subsidy for entitled staff. The Government has not published JobKeeper data with any regularity and we are not sure at this juncture how many businesses and workers are receiving JobKeeper and will therefore be impacted. That said, we know where things stood over the first and second phases of JobKeeper.

The first phase of JobKeeper, announced in March 2020, was taken up by ~1 million businesses and supported ~3.6 million workers. It concluded in late September last year. The second phase involved an extension from 28 September 2020 to 4 January 2021. In November 2020 the Government announced that ~500k business had qualified for the extension covering ~1.5 million employees (following a re-test of eligibility to receive JobKeeper over Q4 20). This was significantly better than the 2020 Budget assumption of ~2.2 million recipients.

There has been no update on this figure and in his recent press conferences over the past month Treasurer Frydenberg has been referring to the figures published in November. We are therefore in the dark on how many businesses and workers were eligible to receive JobKeeper in Q1 21 given the turnover test needed to be satisfied for Q4 20. Notwithstanding, we expect the number of recipients will be significantly lower than Q4 20 given the economy continued to recovery strongly over the December quarter and turnover for many previously eligible businesses would have exceeded the turnover test.

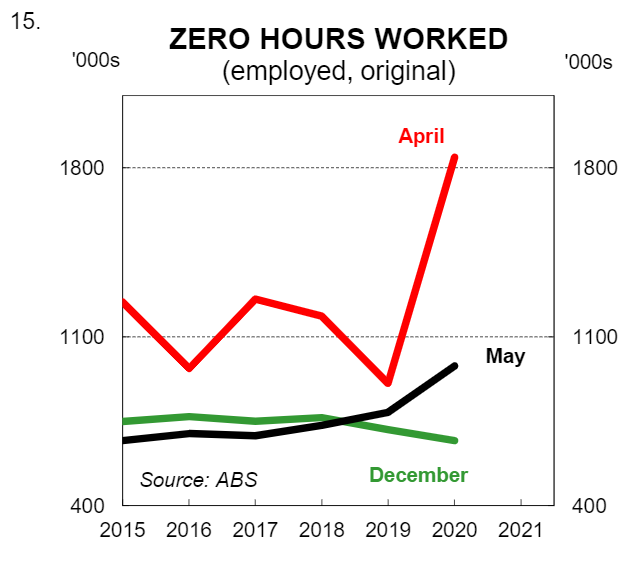

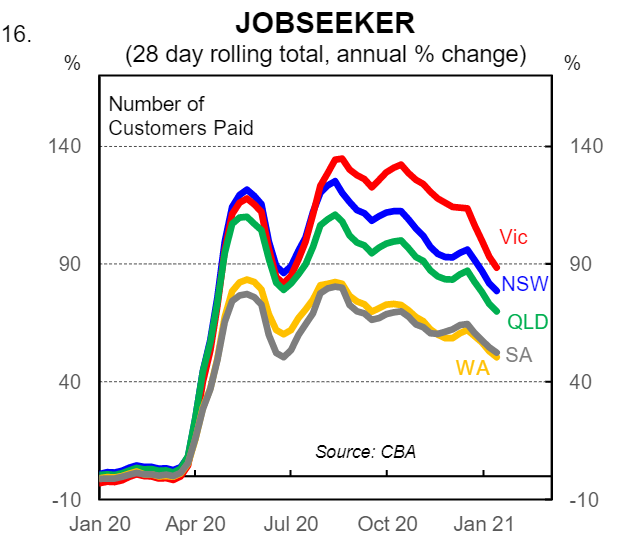

There is a clear risk that businesses will stand down staff when JobKeeper expires. Indeed we expect some retrenchments when the program ends. But overall we do not expect the expiry of JobKeeper to have a major impact on the labour market provided COVID-19 doesn’t resurface and cause lockdowns or major restrictions that limit the capacity of businesses to sell goods and services. Indeed we take comfort from the latest labour force survey which indicated that the number of people considered employed in December 2020but working zero hours for economic reasons was lower than in December 2019 (chart 15). This is in stark contrast to April 2020 when the number of people considered employed but working zero hours was around twice its normal level indicating a lot of people were receiving JobKeeper but not working. CBA wages and salaries data is also encouraging, as covered above, and the number of people receiving JobSeeker continues to fall despite the big drop in the number of businesses receiving JobKeeper (chart 16).

Updated forecasts

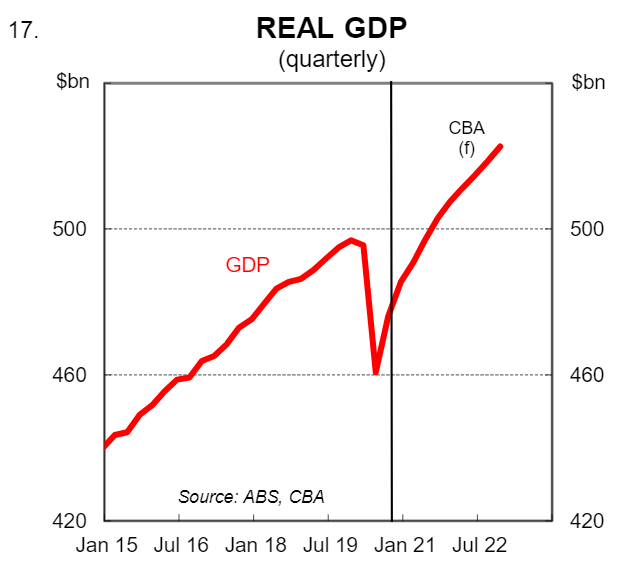

We have made small upward revisions to our profile for GDP because of a stronger than initially anticipated Q4 20 (chart 17). We now expect GDP of 2.6% in Q4 20 versus 2.0% previously. That raises the level of GDP to mean overall we expect the Australian economy to have contracted by 2.6% in 2020. This is an outcome which is much better than official authorities feared when the pandemic arrived in Australia. The RBA, for example, forecast a contraction of 5% in GDP over 2020 in the May 2020 Statement on MonetaryPolicy (SMP). Looking ahead we retain our forecast for strong growth in GDP of 4.2% in 2021 and 3.8% in 2022.

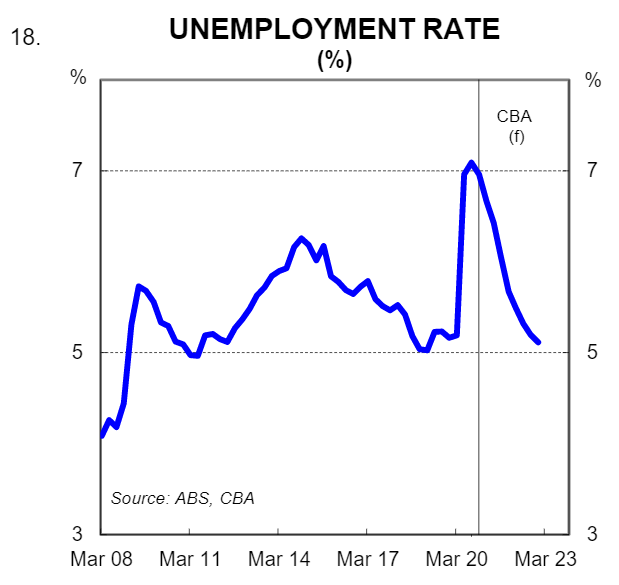

The slight upgrade to our GDP profile would normally lead to a mechanical reduction in our profile for the unemployment rate. But surprisingly the participation rate surged over Q4 20 to hit a record high. It is good news, but from a forecasting perspective it means there is no need for us to lower our profile for the unemployment rate despite higher GDP. Overall we expect the unemployment rate to be 5.7% at end-2021. And we forecast the unemployment rate to be 5.0% at end-2022 (chart 18).

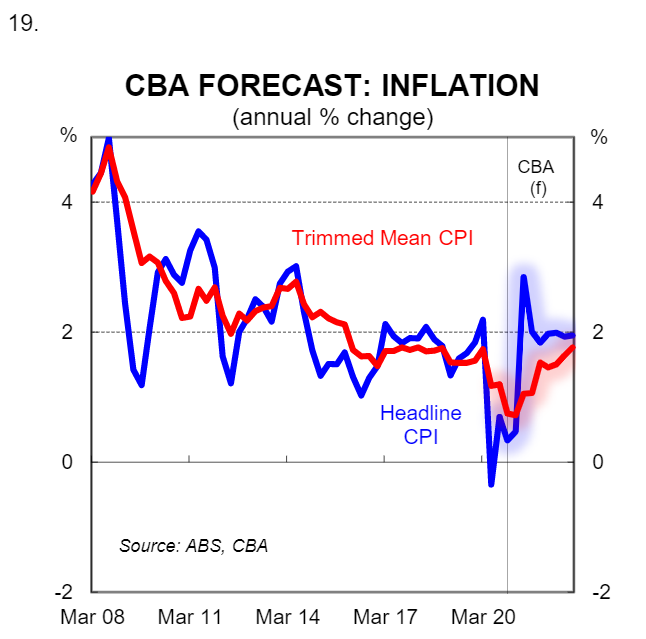

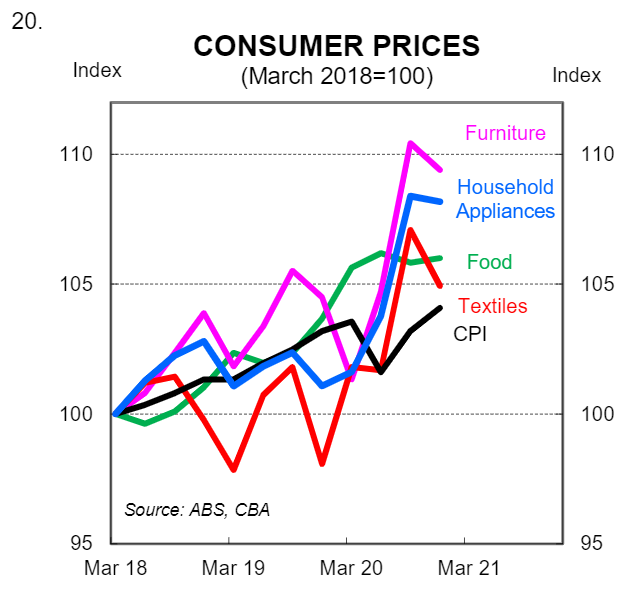

Our central scenario is for inflation to remain low over our forecast horizon but to print higher than the RBA’s forecasts (CBA +1.7%/yr; RBA +1.0%/yr end-21) (chart 19). We continue to point out to readers that the unique nature of theCOVID-19economic shock and the policy response to it means that the outlook for inflation is more uncertain than it has been in recent years. There is a non-trivial risk that 6-month annualised core inflation pushes through the key 2% watermark at some stage in 2021 due to some ‘demand pull’ inflation. Such an outcome would cause some discomfort in financial markets, particularly fixed income markets. There was evidence of demand-pull inflation in the Q4 20 CPI (chart 20).

Given the heightened degree of uncertainty around forecasting at the moment we stress that the overall story is more important than our point forecasts. And the shape of our profile is what readers should focus on. In summary we expect the strong recovery to continue and believe there are upside risks to inflation. Table 2below contains our updated quarterly profile for GDP, employment, unemployment and inflation.

What about the downside risks?

The case that we put forward for the Australian economic outlook is an optimistic one and there are numerous downside risks that mean our forecasts may not come to fruition. A quick checklist of downside risks yields the following: (i) the return of COVID-19 ‘clusters’ and resultant reimposition of restrictions / lockdowns; (ii) end of JobKeeper; (iii) ineffective vaccine/s; (iv) fiscal tightening (i.e. premature budget repair); (v) a surge in net overseas migration when borders reopen (i.e. a labour market supply shock); (vi) higher consumer price inflation leading to a lift in bond yields and a tightening in financial conditions; (vii) further escalation of Australia / China trade tensions that materially changes the outlook for exports; and (viii) macroprudential policy resulting in a tightening in credit supply.

However, whilst we are cognisant of all of these potential downside risks, it is not our central scenario that any of these risks materialise and therefore we do not incorporate them in our base case. Rather they remain risks and we will monitor them. There are also upside risks to consider, although we park them to the side for the time being as we want our readers to focus on our central scenario.

Monetary policy implications

Massive fiscal and monetary policy stimulus has been essential to the economic recovery and we expect monetary policy to remain loose. We expect the cash rate to be left on hold at 0.10% over our forecast horizon (end-2022), which is of course in line with the RBA’s rhetoric that, “the Board is not expecting to increase the cash rate for at least 3 years (last said in December 20)”.

Financial markets right now are most interested in what the RBA will do when its current $A100bn bond buying program (Quantitative Easing (QE)) is due to be completed in April. Given that the overall readings in the Q4 20 CPI were still low and that the economy is still operating well below the level of unemployment associated with full employment, we expect the RBA to extend their government bond purchases by a further $A100bn. We expect the RBA to complete these purchases over a six month period – as was the case with the first tranche of quantity-based QE. Extending their bond buying program is the path of least regret. It will ensure that their policy decisions do not put any undesired upward pressure on the Australian dollar. And it will assist both Federal and State governments in financing their large fiscal expansions. We do not expect the RBA to announce any extension to QE at the February Board meeting. Rather it will come either at the March or April Board meeting.

The outlook for the target yield on the 3yr Australian Commonwealth Government Bond (ACGB) –currently 0.1% which is the same as the cash rate target – is a little more uncertain. The RBA cannot say that it does not expect to increase the cash rate for at least 3 years indefinitely, for there is always ‘at least 3 more years’ from whenever it is last said. At some stage in the future as the labour market continues to tighten and inflation lifts a little the RBA Board will change its explicit forward guidance. When that happens the RBA will need to do something about the target yield on the 3yr ACGB. There are a variety of approaches they could take, with the obvious solutions being either to remove the target or lift the target yield. We had been of the view that this could happen by the middle of 2021 based on our forecasts for the unemployment rate. But the reimposition of restrictions in a number of jurisdictions in late last year and early January because of ‘COVID clusters’ means that the RBA is likely to wait until the threat of any further lockdowns has fully receded before changing tact on the 3yr target. That will not be until the vaccine rollout is close to completion around September/October 2021.

We have not heard from the RBA since mid-December 2020, but we hear from them several times in early February. The first RBA Board meeting for 2021 is on 2 February. Governor Philip Lowe is scheduled to deliver a speech on 3 February. And the February Statement on Monetary Policy (SMP) will be published on 5 February. We expect the RBA to upgrade their forecast profile for GDP and by extension lower their profile for the unemployment rate. Modest upward revisions are also expected to their inflation forecasts although we expect them to continue to forecast below target inflation over the bulk of their forecast horizon, if not all of it. We will have a much clearer picture of current RBA thinking at the end of next week and we will refine our monetary policy views accordingly, particularly around the 3yr target and the term funding facility (TFF).