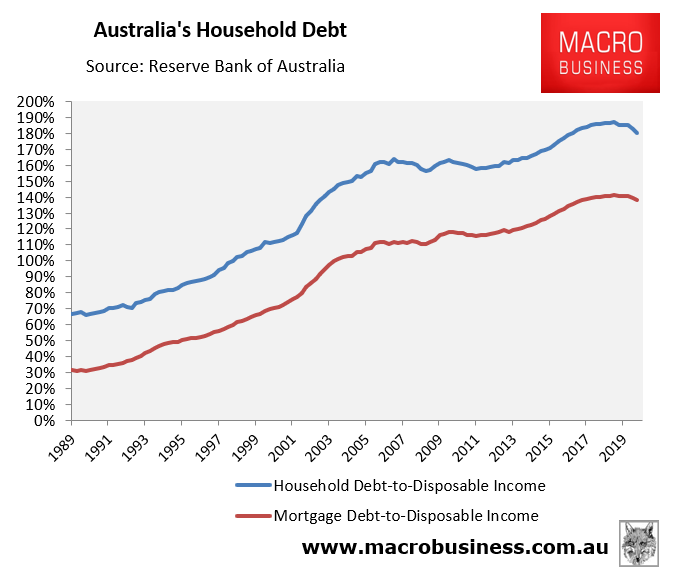

The Reserve Bank of Australia (RBA) has released household debt data for the September quarter of 2020, which reveals that the ratio of household debt to disposable income fell to 179.9% from 182.6% in the June quarter:

Within this figure, the ratio of mortgage debt to household disposable income fell to 138.0% in September from 139.5% in the June quarter.

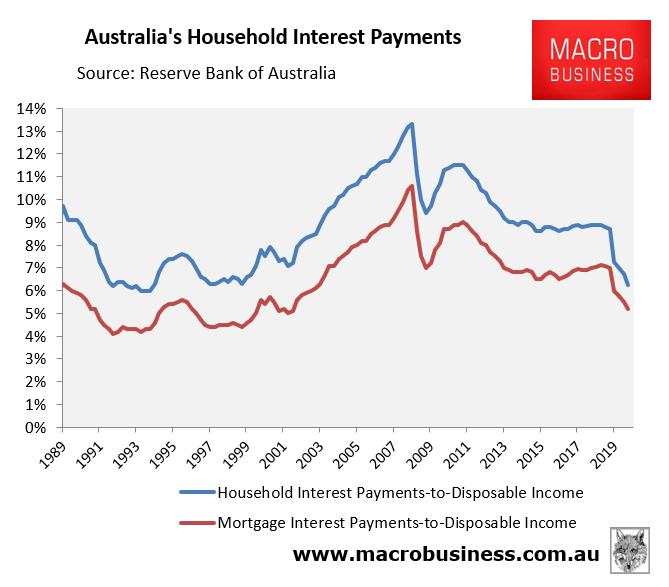

More importantly, the ratio of household interest payments to household disposable income fell to 6.3%. This is the lowest recorded level since September 1999 and less than half the December 2008 peak of 13.3%:

In a similar vein, the ratio of mortgage interest payments to household disposable income fell to only 5.2%, which is the lowest figure since June 2002 and less than half the December 2008 peak of 10.6%.

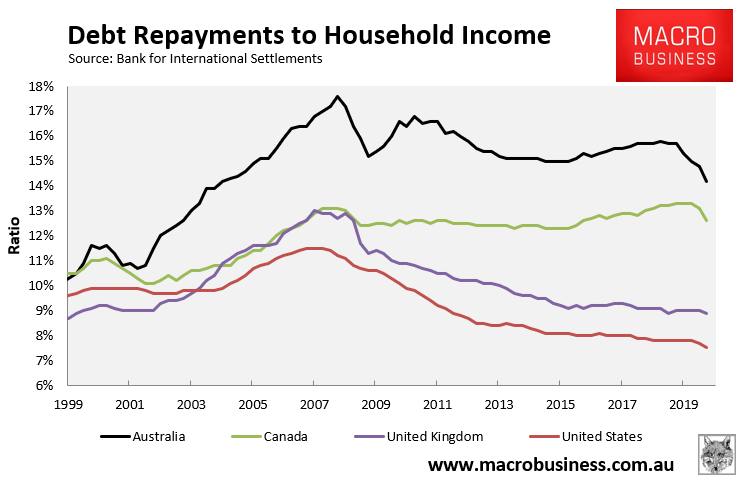

Separate data from the Bank for International Settlements also shows that household debt repayments (i.e. both principal and interest) fell to 14.2% of disposable income in the June quarter of 2020, the lowest recorded level since September 2004:

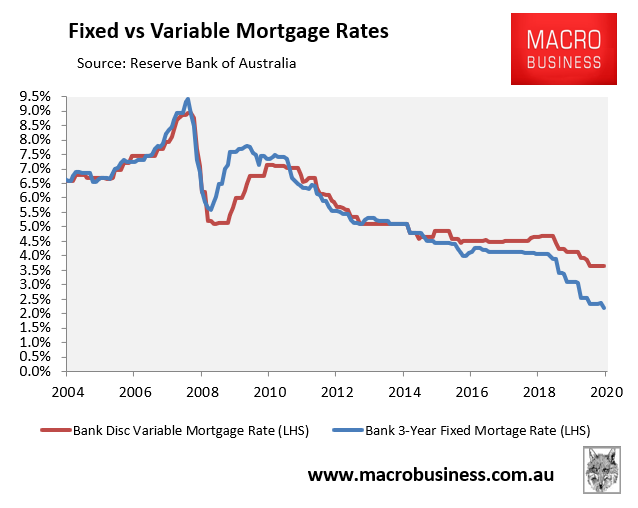

The reason for the cratering debt repayment burden is obvious: average mortgage rates have fallen to all-time lows, namely 3.65% variable and 2.20% 3-year fixed:

Expect the debt repayment burden to fall further as borrowers pivot to fixed rate mortgages. Those rates are way too low to ignore.