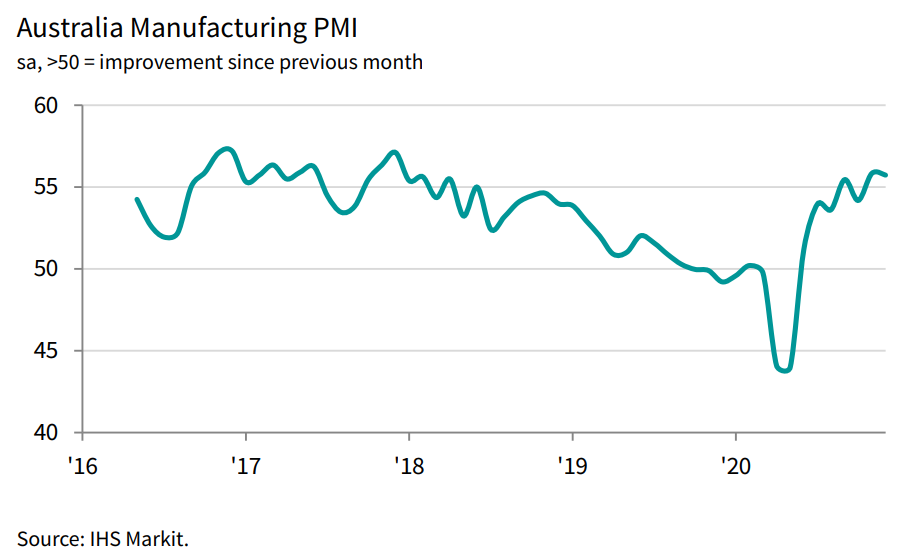

The Australian Markit December Manufacturing PMI is out and it shows that Australia’s manufacturers ended 2020 on a strong note, with the PMI hovering near a three-year high and jobs growth the strongest for over two years:

Key findings:

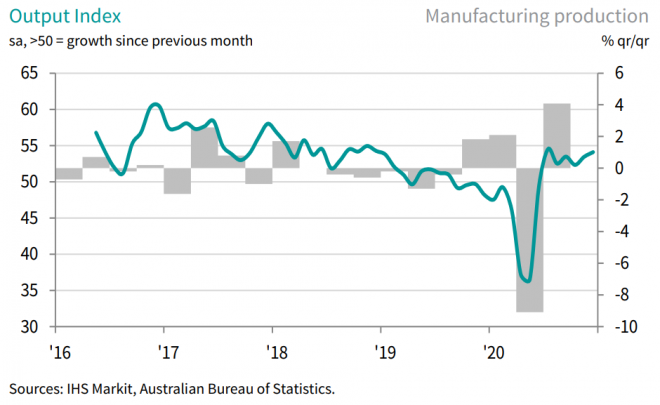

Output and new orders growth continues to accelerate

Jobs growth strongest for over two years as firms boost capacity

Supply chains and exports under pressure amid

Australia’s manufacturing economy continued to recover at one of the strongest rates seen over the past three years in December, with output, order book and employment growth accelerating. Supply chain delays and shipping problems continued to impact input buying and export sales, however, constraining growth at many firms. Business optimism also cooled slightly, in part due to concerns over trade tensions with China.

The headline index from the survey, the seasonally adjusted IHS Markit Manufacturing Purchasing Managers’ Index™ (PMI®) edged down from November’s 35-month high of 55.8 to 55.7 in December, pulled lower by supply chain delays which limited firms’ abilities to buy sufficient quantities of inputs.

Output growth accelerated to the second-fastest in two years, falling just short of July’s recent peak, sustaining the recovery into its sixth successive month. Output was buoyed by a further acceleration of order book growth, in turn reflecting rising demand as the economy showed further signs of lifting from coronavirus disease 2019 (COVID-19) lockdowns. New orders showed the largest gain since November 2018.

The improvement in order book inflows was limited to the domestic market, however, as new export orders fell at the sharpest rate since August, despite signs of rising demand in some key markets such as the US and Europe. Firms cited a combination of worsening trade tensions with China and a further marked deterioration of shipping conditions.

A lack of shipping, container shortages, port congestion and supplier capacity constraints were all commonly reported as having also led to a further substantial lengthening of average supplier lead-times, which in turn led to a noticeable drop in firms’ inventories of inputs.

Inventories of finished goods also fell, down for an eleventh successive month, and backlogs of work rose at the steepest rate since September, in both cases widely linked to production having been constrained by input shortages.

However, many companies also reported that backlogs of work had risen simply due to a short-term inability to expand production capacity sufficiently to meet the recent surge in demand. Efforts to boost capacity were reflected in manufacturers taking on extra staff at a rate not seen for just over two years.

Input prices meanwhile rose sharply, with the rate of increase the fastest since June. Higher costs commonly reflected shipping surcharges and suppliers enjoying greater pricing power amid the recent upturn in demand. Average selling prices also rose as producers sought to pass these higher costs on to customers.

Finally, expectations of output in the year ahead remained positive, with companies hopeful of life returning to normal as the COVID-19 pandemic recedes. Production gains are set to be boosted by increased sales and marketing activity. However, the overall degree of optimism cooled compared to November, in part due to concerns over the ongoing pandemic and escalating trade tensions with China.

Comment

Commenting on the latest survey results, Chris Williamson, Chief Business Economist at IHS Markit, said:

“Australia’s manufacturers ended 2020 on a strong note, reporting one of the strongest upturns in production since 2018 as order books continued to recover. Many firms even struggled to boost capacity sufficiently to meet the recent surge in demand, despite the sector taking on extra staff at the fastest rate for two years.

“The upturn in production was made even more impressive by supply chains having been severely disrupted again by a combination of shipping delays, shortages of inputs and an increased rate of loss of exports.

“Businesses also remained optimistic about the outlook for the year ahead. On balance, however, expectations were reined in slightly compared to November due to increased concerns that the pandemic will stretch further into 2021 than previously thought, and the possibility of escalating trade tensions.”

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.