The Australian dollar took a pounding last night:

As DXY surged off a little head and shoulders bottom:

Westpac has the wrap:

Event Wrap

The US Federal Reserve’s FOMC left its policy settings unchanged as was widely expected: a 0%-0.25% Fed funds rate range, and at least $120 bn/month bond purchases. The statement reiterated that QE will be maintained until “substantial further progress has been made toward the Committee’s maximum employment and price stability goals.” The pace of the recovery in the economy and employment was seen to have “moderated…with weakness concentrated in the sectors most adversely affected by the pandemic.” Looking ahead, the Fed said the path of the economy will depend on the course of the virus, adding “including progress on vaccines.” The ongoing public health crisis is seen to pose “considerable risks to the economic outlook.” The vote was a unanimous 11-0, with new member Waller participating, along with the four voting members rotated back: Barkin, Bostic, Evans, and Daly.

US durable orders were mixed in December. Although the headline was disappointing at +0.2%m/m (est. +1.0%m/m) there were upside revisions to Nov. (to +1.2%m/m from +1.0%m/m). The ex-transport measure rose 0.7%m/m (vs. est. +0.5%m/m, prior +0.8% from initial +0.4%), non-defence +0.6%m/m (est. +0.5%m/m, prior +1.0% from initial +0.5%). This is always a volatile series but even more so at present especially given the disruptions to the transport sector.

German GfK consumer confidence survey was soft at -15.6 (est. -7.9, prior -7.5), as was French consumer confidence (92, est. 94, prior 95), as Covid-related restrictions and lockdowns weighed on prospects for Q1.

The ECB’s Knot stressed that it was prepared to take further action and had “further policy tools” to support the regional economy. He also reiterated that it was monitoring EUR strength and would “counter appreciation if needed”.

The UK and EU continue to spar over Covid vaccine supplies, with growing concern over delivery shortfalls, notably from UK-based AstraZeneca. Lockdowns look set to resume in France, and the UK is preparing for an extension of its current stringent lockdown.

Event Outlook

Australia: The Q4 export price index is expected rise 4.0% on higher commodity prices, notably iron ore. Meanwhile, Westpac is looking for a 1.5% fall in the Q4 import price index as the strong AUD drives cheaper imports.

New Zealand: Westpac expects that the December trade balance will increase to +$1450m as import disruptions continue.

Euro Area: Despite clear headwinds facing the bloc, January economic confidence will be supported by the ECB’s commitment to ongoing monetary stimulus (market f/c: 89.5).

US: Initial jobless claims will be released for the week ended Jan 23rd. Claims stabilised in the last update after spiking the week prior (market f/c: 875k). Finally, Q4 GDP is set to expand 3.9% (annualised); the recovery slowed abruptly in the December quarter as COVID-19 cases surged.

So, we now have both the ECB and Chinese authorities pushing back against the USD devaluation. I still think it has further to run. But it’s overextended now.

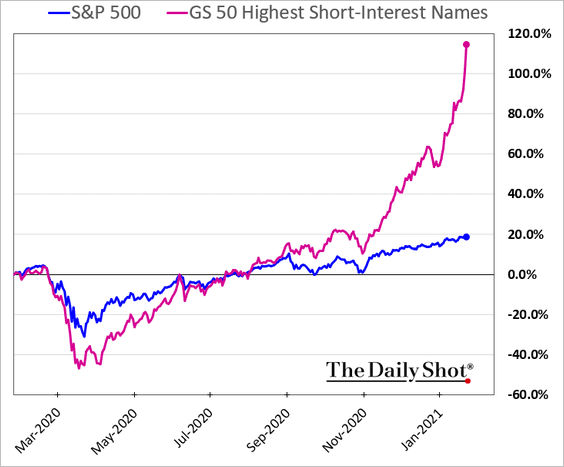

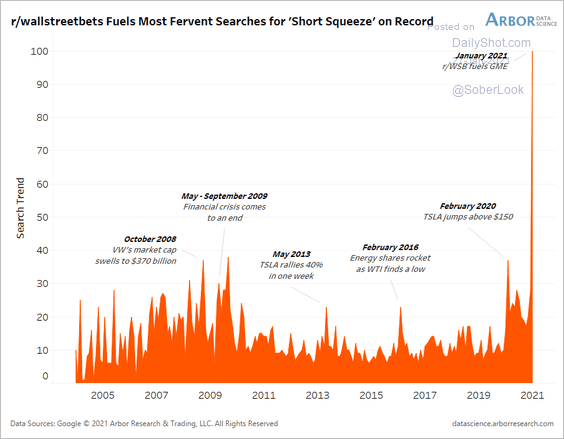

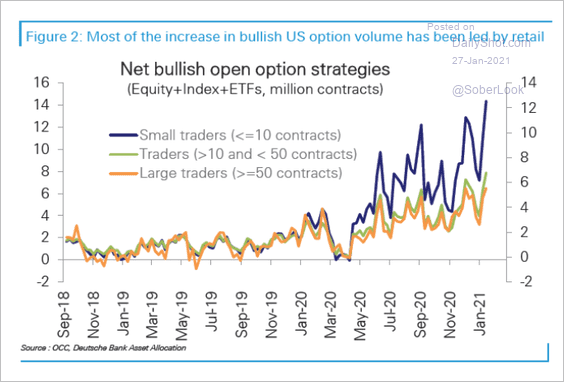

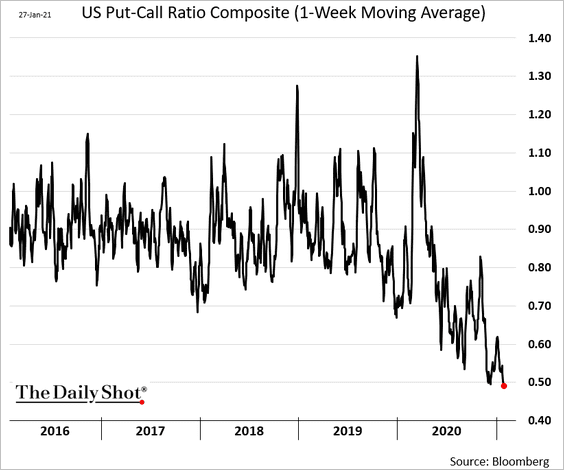

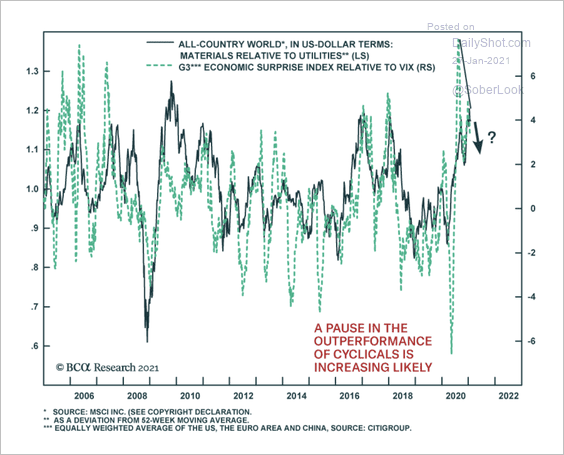

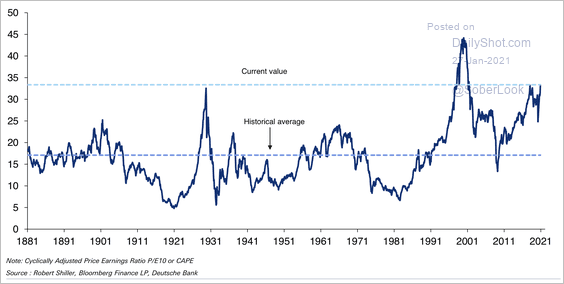

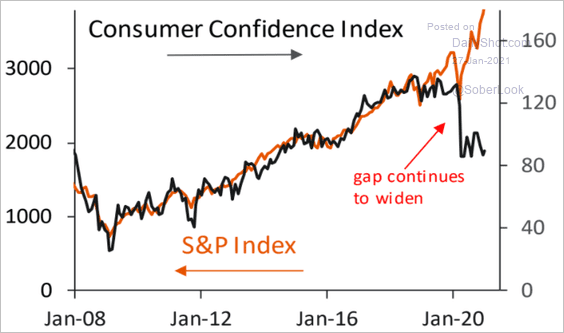

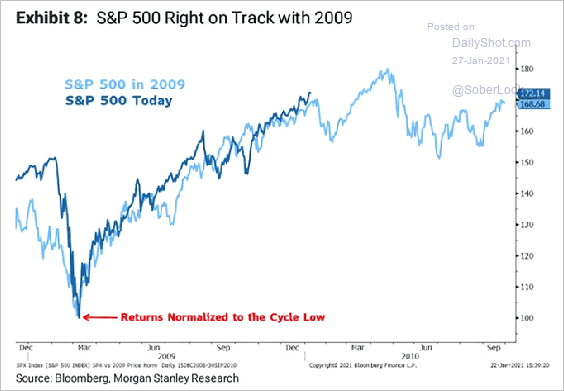

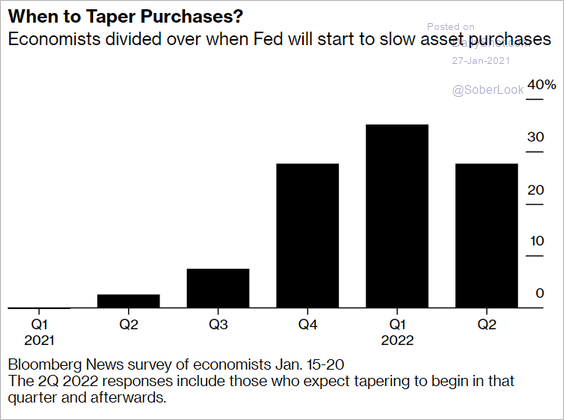

As are stocks. Some charts from Daily Shot:

The entire reflation trade is due for a decent pullback, including the Australian dollar. The tech bubble could pop at any time:

Which, ironically, will support no taper at all!