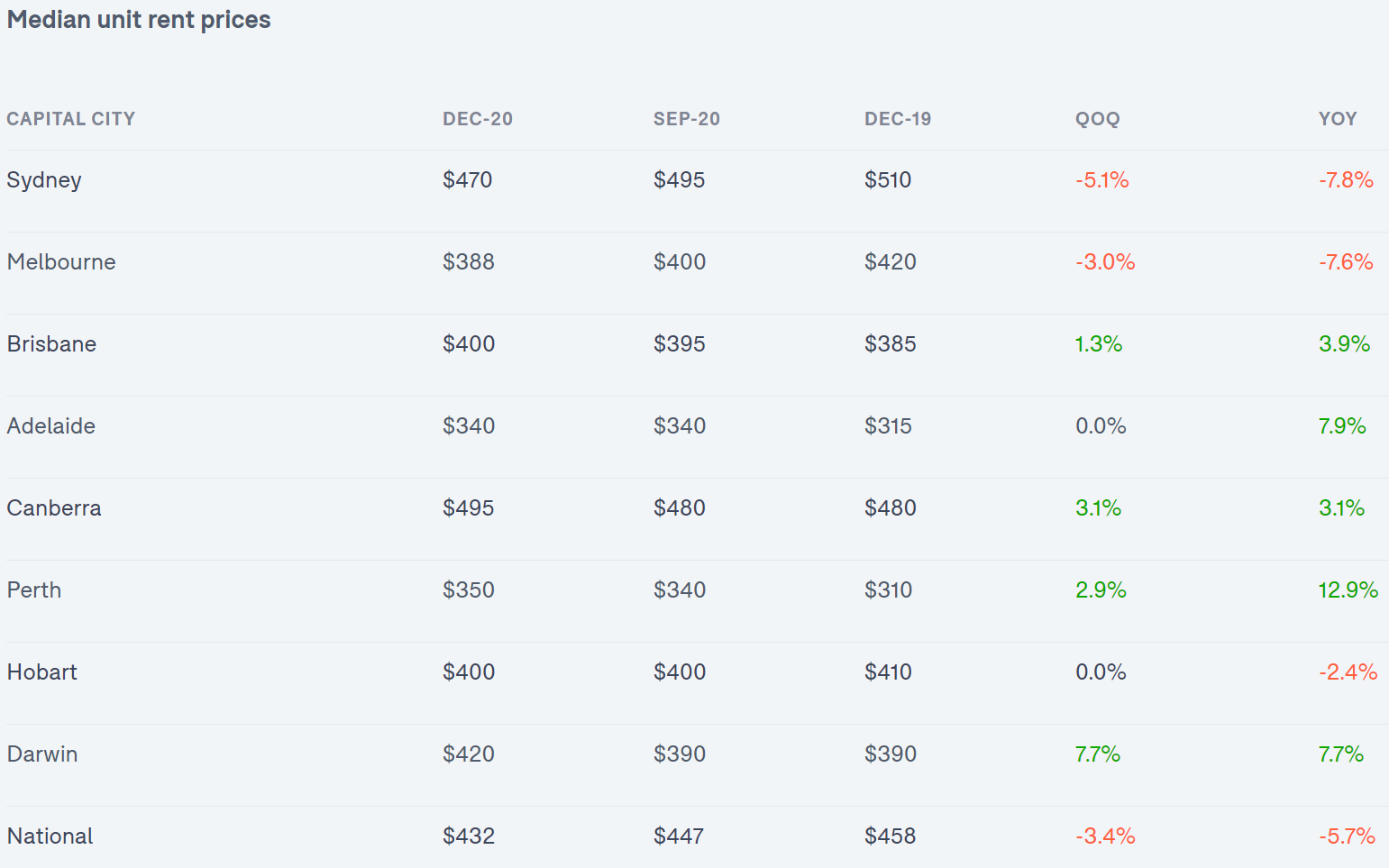

Domain’s December quarter Rental Report has been released, which reveals that apartment (unit) rents have fallen off a cliff across Sydney and Melbourne, driven by collapsing demand from international students and migrants alongside ballooning supply:

In Sydney, apartment rents have plummeted to 2013 levels whereas they have fallen to 2016 levels in Melbourne:

Sydney

Unit rents made the steepest quarterly and annual fall since Domain rental records began in 2004. Unit rents tumbled $25 over the December quarter to $470 a week and since pre-pandemic March $50 has been shaved from asking rents. The cost of renting a unit has now returned to 2013 levels. Unit rents have been hardest hit in the city and east and inner west with rents at an eight-year low, and the lower north shore is the cheapest in nine years.

Annually unit rents have been falling since mid-2018 but this trend has been accelerated by changes as a result of COVID-19. The pandemic-induced collapse to overseas migration and foreign student numbers has reduced rental demand. Units have felt the impact, particularly inner-city apartments, which are home to more rentals and have a greater exposure to demand sourced from overseas migrants. The additional dynamic of heightened apartment construction in recent years has also added to the supply pool…

Melbourne

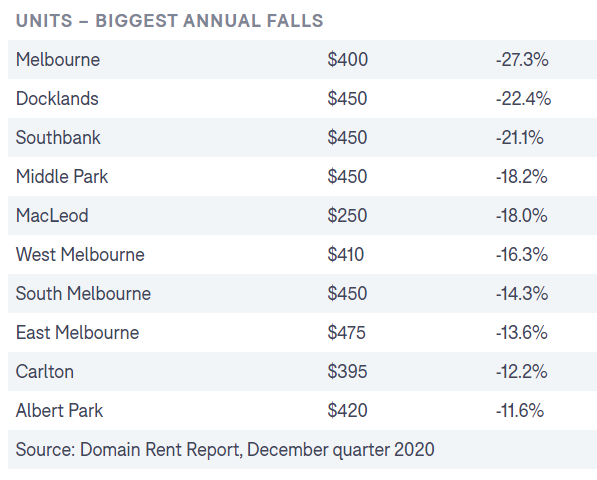

Of all the capital cities, Melbourne units have recorded the deepest fall in asking rent since pre-pandemic March, down 9.8 per cent. Although the rate of decline eased over the December quarter, three consecutive quarterly falls have resulted in the steepest annual fall on record. Unit rents are now at 2016 levels. For the first time in five years Melbourne is the third most affordable capital city to rent a unit, after Adelaide and Perth. A marked change considering Melbourne was the third most expensive city to rent a unit back in March. Inner-city apartments have been hardest hit with rents at a seven-year low, followed by the inner east and inner south hitting a four-year low.

Melbourne’s elevated vacancy rate is directly associated with secondary lockdowns and state border restrictions. Rental demand has been severely reduced as international border closures curtail overseas migration, as well as a drop in tourism and changes to personal finances. This has had a greater impact on inner city apartments, heightened in areas that have seen extensive high-rise construction in recent years.

Advertisement

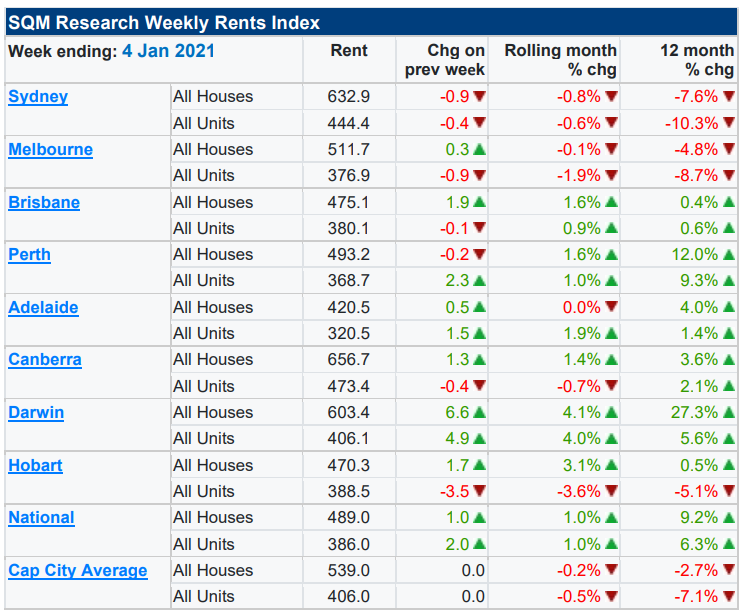

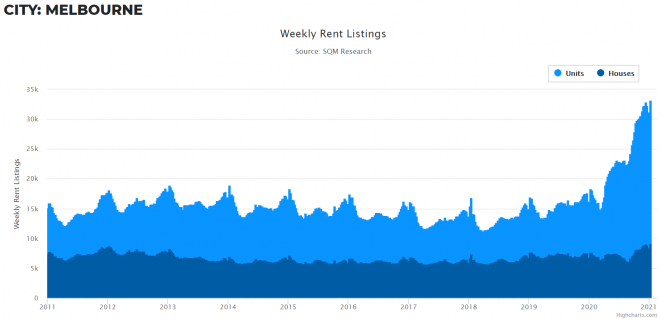

SQM Research corroborates this data, showing a large fall in apartment asking rents across Sydney and Melbourne:

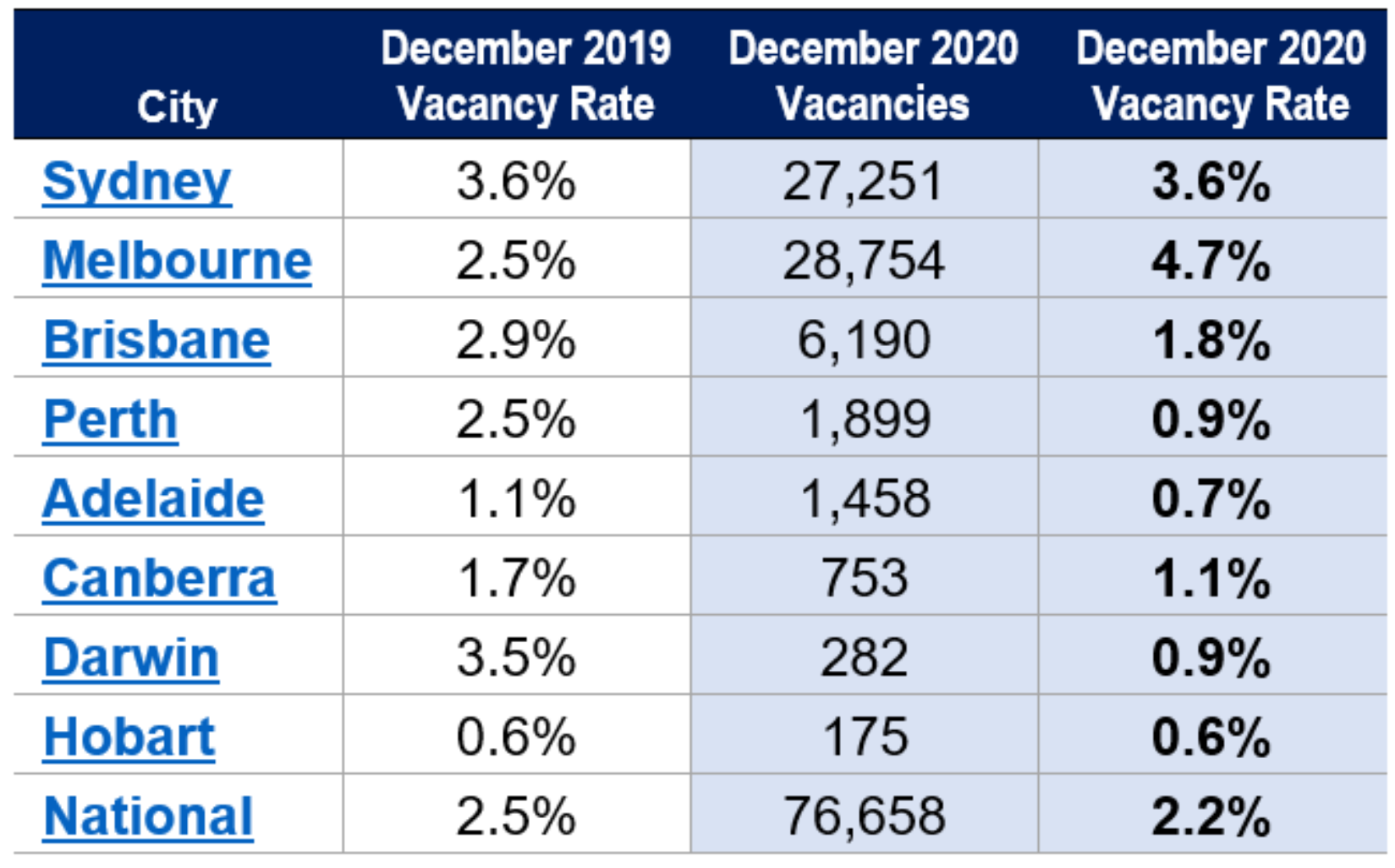

This is on the back of elevated vacancies (and a ginormous increase across Melbourne):

Advertisement

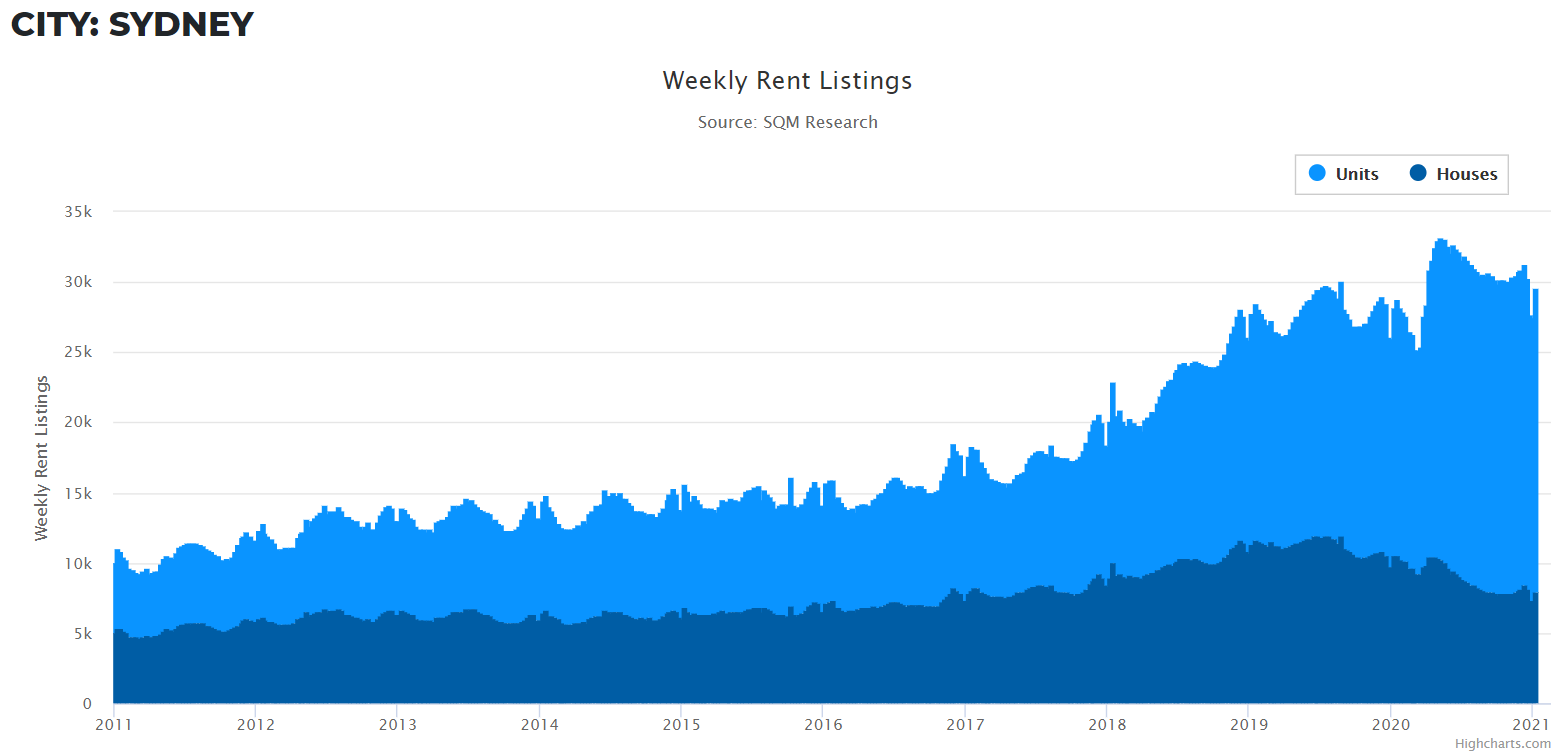

As well as swelling apartment rental listings across both markets:

Advertisement

To add insult to injury, Domain reports that short-term rental owners have put their properties on the long-term market, which has worsened the oversupply amid falling demand:

A glut of vacant inner-city apartments once used as short-term accommodation has helped push Melbourne rental prices to a four-year low, with new figures showing more than half the short-stay listings in the CBD were withdrawn in the last year…

A jump in supply coincided with a drop in demand, with available Melbourne CBD vacation rentals dropping from 3401 in December 2019 to just 1541 a year later, according to data from short-term rental analytics firm AirDNA.

As many owners offered empty units for long-term lease, residential rents in the CBD fell by 27.3 per cent in the year to December, to a median $400 per week, on Domain data…

Charter Keck Cramer director Angie Zigomanis said short-term accommodation added back into the rental market exacerbated the downward pressure on rents in inner-city areas.

Landlords of short-stay rentals in the heart of Sydney that once fetched hundreds of dollars a night have been forced to return them to the long-term rental market amid the pandemic, with the supply glut slashing prices for locals…

Thousands of available short-stay listings in Greater Sydney were shed over the year to December, according to data from short-term rental analytics firm AirDNA.

More than 20,300 short-term listings were available in December 2019, falling to under 11,400 a year later.

According to SQM managing director Louis Christopher:

“It’s clear Sydney and Melbourne apartment investors were the losers of 2020 with rents and prices falling”.

That’s an understatement. On the other hand, renters in these two cities were big winners.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.