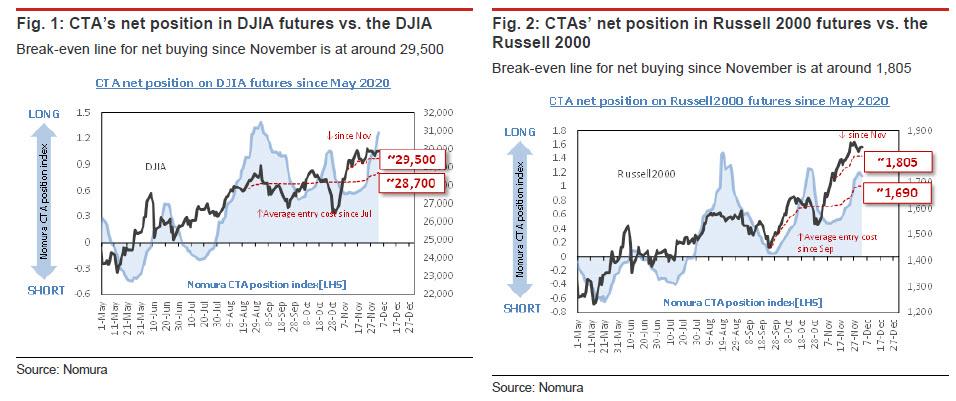

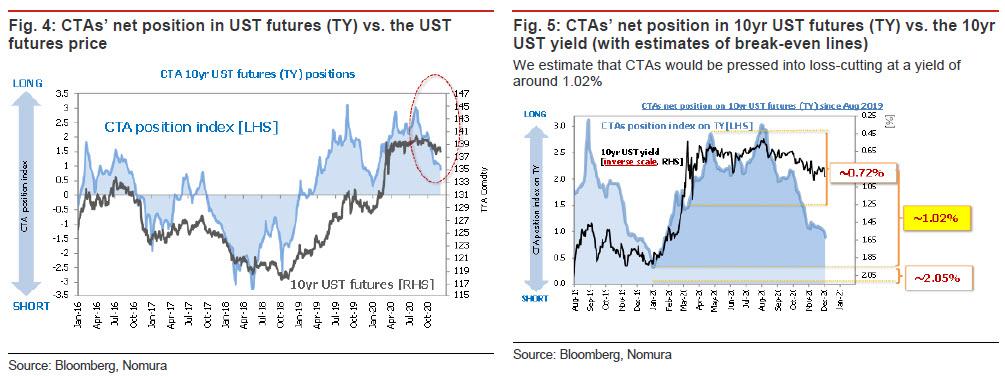

As Nomura quant Masanari Takada writes when commenting on yesterday’s spike in 10Y yield which rose as high as 0.96%, “CTAs have resumed preemptive exits from long positions in UST futures.” Noting that at the same time as momentum-chasing CTAs have been gradually adding to their exposure in DJIA and Russell 2000 futures …

… CTAs are being drawn back into exiting long positions in 10yr UST futures (TY). As 10yr yields bounced back up to around 0.95% this week, “CTAs, who had been waiting on the sidelines, have again been pressed into action” with the Nomura quant estimating that CTAs have already liquidated about 65% of the long TY positions they held at the peak in August, and with a key trigger line at around 1.02% on the near horizon, CTAs are looking increasingly likely to have to exit the entirety of their aggregate net long TY position.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.