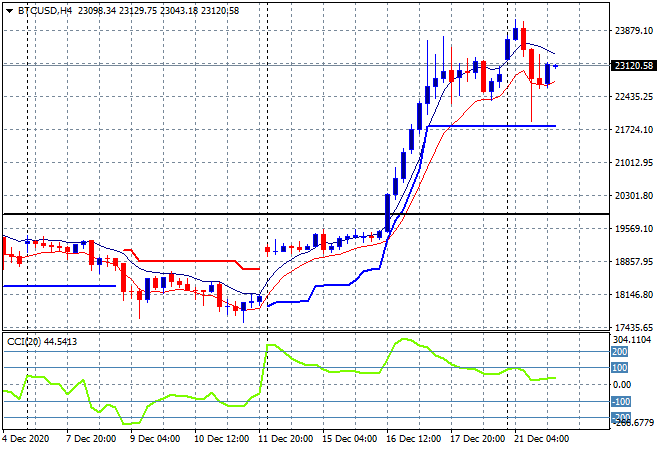

Big round trip’s in prices across many risk markets overnight due to concerns over a new strain of COVID-19, leading to a leap in volatility that is sure to continue here in Asia. Despite a new round of stimulus from Congress, Wall Street is not convinced and remains lacking in confidence, as does Europe as London goes into lockdown and travel grinds to a halt. Commodities continue to be bid – especially iron ore – while Bitcoin had a wobble through the $23000 level as it looked close to breaking below very short term support only a couple thousand dollars lower (sic):

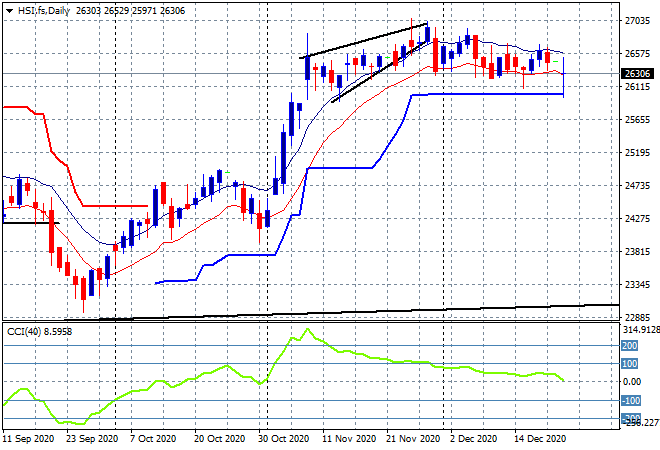

Looking at share markets in Asia from yesterday’s starting session where the Shanghai Composite was the standout, advancing nearly 0.8% to close at 3420 points while in Hong Kong the Hang Seng Index slumped at the close after dog paddling through a scratch session, finishing nearly 0.7% lower at 26306 points The daily chart is moving from a sideways jaunt to something a bit more ominous as momentum stalls, with the lack of any new daily highs pushing sentiment lower. I’m continuing to watch ATR daily support at the 26000 point level:

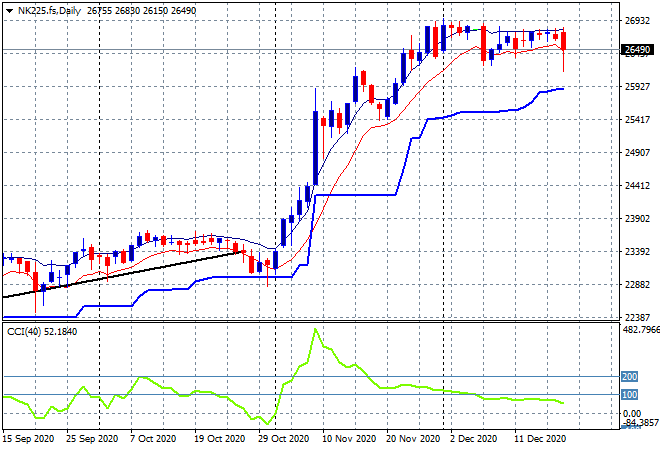

Japanese stock markets remained in stall mode with a mild selloff on the Nikkei 225, closing 0.2% lower to 26714 points. Futures were volatile, following last night’s big roundtrips, suggesting more downside on the way on the open. The daily chart remains poised in a very boring sideways pattern, as resistance at 27000 points still proves too tough to beat. I’m continuing to watch the low moving average at the 26400 point area as a potential breakdown looms:

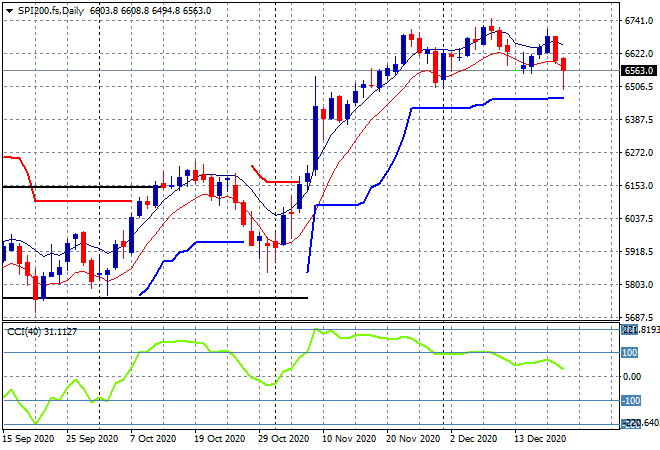

The ASX200 also tread water and did almost nothing yesterday, down about 0.1% to 6669 points, keeping well clear of the 6700 point level after its poor finish last week. SPI futures indicate a 20 point drop on the open, with even more downside warranted following the Sydney COVID breakout. I’m watching strong daily support at or just below the 6500 level that must hold going into year end:

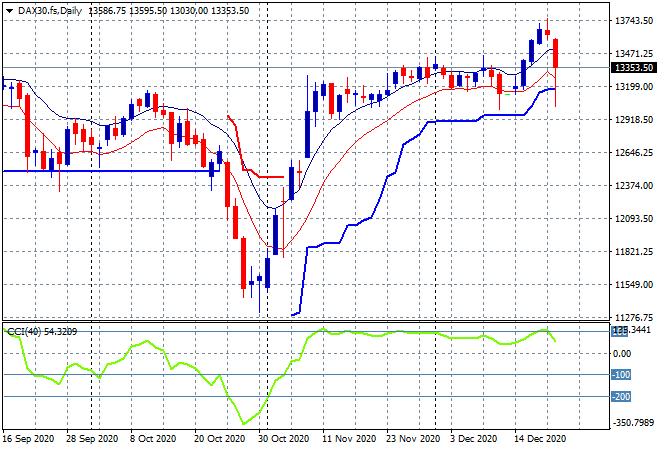

European markets were again united, but this time with some big selloffs across the continent and in the UK as COVID concerns finally ramp up. A lot of the downside has recovered in post close futures, with the German DAX nominally closing 2.8% lower at 13246 points, but has recovered nearly half that in futures. The nascent breakout has been thwarted for now, with this increase in volatility during a low volume period not unsurprising, but concerning if prices close below ATR support at the 13000 point level proper:

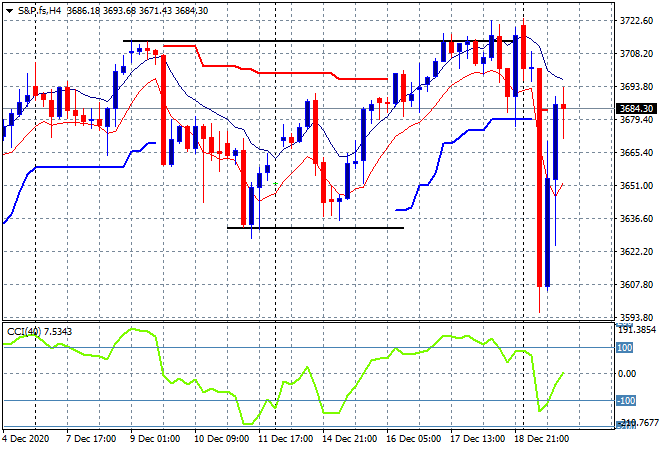

Wall Street had some big roundtrips as a cursory look at the four hourly S&P chart below shows. The headline results were the NASDAQ down only 0.1% while the S&P500 fell only 0.3% lower at 3694 points, but unable to hold above the 3700 points barrier. The four hourly chart shows the volatility quite well (Tesla joining the main bourse not helping) and a very quick roundtrip to 3600 points as the stimulus measures were underwhelming as expected. If the market cannot clear 3700-3710 before Xmas we are in for more downside:

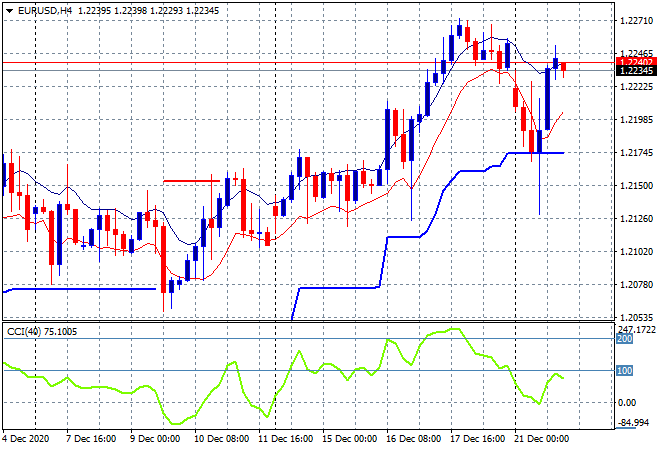

Currency markets are also seeing increased volatility as traders re-assess their end of year crystal balls with Euro in particular having a wild ride. The union currency dropped right through short term support at the 1.2170 level, almost crossing below the 1.21 handle before zooming back up towards its Friday night trading range to be back above the 1.22 level again. Momentum readings are nominally positive but the inability to beat last week’s session high maybe telling in the volatility going forward:

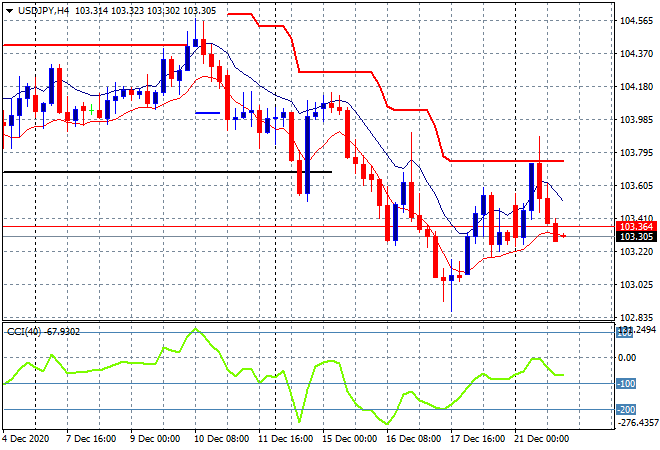

The USDJPY pair had a similar but not same magnitude ride, lifting up towards overhead resistance before heading back down to the 103.30 level, still below weekly support at the 103.60 area (solid black horizontal line below). Momentum remains negative and price is back again below the low moving average so I expect more downside today as deflationary pressures mount:

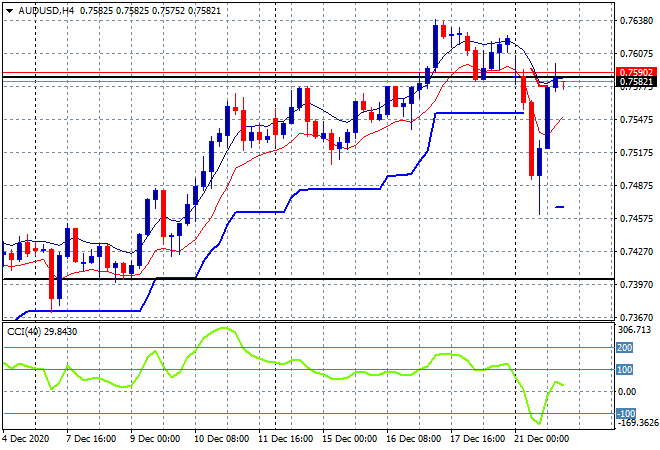

The Australian dollar had a lovely trip thank you very much, heading down to the mid 74s before back on deck just below the 76 handle and on the current yearly high. Its hard to make predictions, especially about the future, but the short term does look a bit toppy for Aussie, even though iron ore prices are not stopping anytime soon. I’m watching the 75.40 level for signs of a short term retracement here that could spread into something more meaningful:

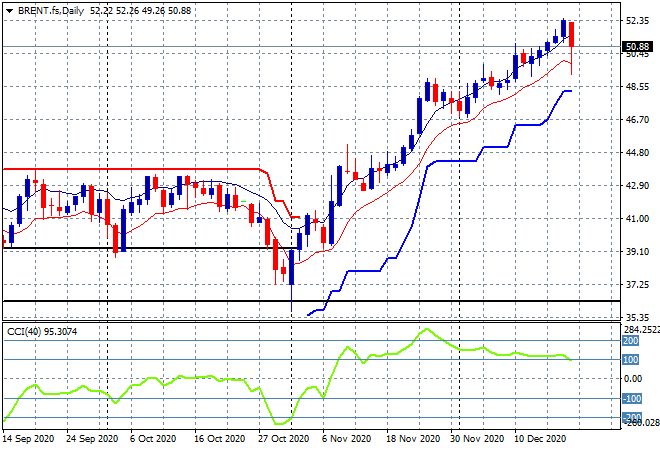

Oil prices suffered a similar fate to risk currencies with a mild roundtrip, with Brent crude down through the $50USD per barrel level before coming back to close just below $51 in what does yet look like a topping action. Momentum remains nicely overbought and with the $54-56 region not that far away we could see it breached before year end:

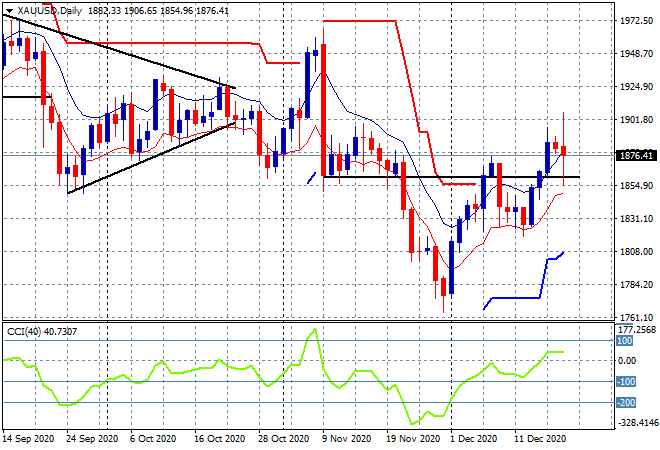

Gold also had an interesting night, but zooming out to the daily chart, it finished pretty much where it started at above its early December highs just below the $1880USD per ounce level. Looking at the daily chart, a powerful inverse head and shoulders bullish pattern is forming with the potential to breach the $1930 level in the new year if daily momentum is maintained:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!