DXY was a little firmer last night:

The Australian dollar breakout collapsed:

Gold firmed as oil fell:

Base metals were mixed as copper enters blowoff:

Miners were hit:

EM stocks too:

Junk is fine:

Treasuries bid:

Stocks eased:

Westpac has the wrap:

Event Wrap

US pending home sales rose 1.0% in October, beating expectations of a 1.1% fall. The Dallas Fed manufacturing survey weakened from 19.8 to 12.0 (vs 14.3 expected). The Chicago PMI survey fell from 61.1 to 58.2 (vs 59.0 expected).

Event Outlook

Australia: The CoreLogic home value index will be buoyed by Melbourne’s reopening – Westpac is looking for a 0.6% rise in November. The ABS will then release “Weekly Payroll Jobs and Wages” for the week ended Nov 14; a timely indicator, but it failed to capture October’s big employment gain. Supported by the HomeBuilder scheme and the broader reopening, Westpac expects that October dwelling approvals will retrace 3% but hold onto much of September’s outsized increase. Q3 net exports are set to detract 1.7ppts from GDP, a result of surging imports as supply lines are restored and the economy reopens. Although the current account balance has fallen from its record high, it will post its 6th consecutive surplus in Q3 (WBC f/c: $6.5bn). To round out the partial data, Q3 public demand should see a sizeable 1.2% increase.

Turning to monetary policy, The RBA is set to remain in “watch and wait mode” and is unlikely to announce any additional moves at its December meeting (WBC f/c: 0.10%). The Board will affirm that is prepared to do more if needed.

Finally, the November update of the AiG PMI will be published.

China: The November Caixin manufacturing PMI should remain robust (market f/c: 53.5); the official index currently sits at a 3-year high.

Asia: November Nikkei manufacturing PMIs will be released for Malaysia, Indonesia, South Korea, Taiwan, and India.

Euro Area: Another anaemic read in the November CPI should prompt ECB action at the December meeting (market f/c: -0.3%).

US: The ISM manufacturing index is set to pull back from its two-year high (market f/c: 58.0). Construction spending should post a 0.8% increase, with strong residential construction outweighing weaker non-res. Finally Chair Powell (02:00 AEDT), Brainard (04:00 AEDT), Daly (05:15 AEDT) and Evans (07:00 AEDT)will speak.

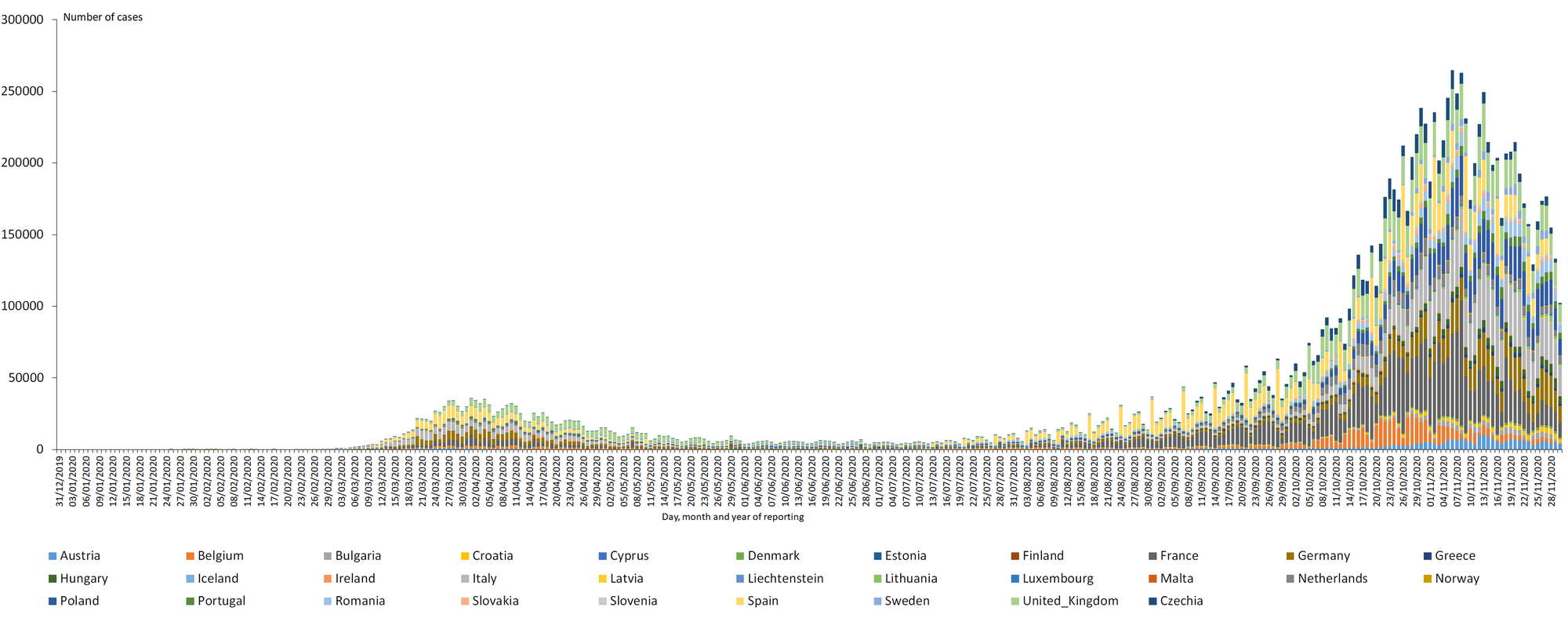

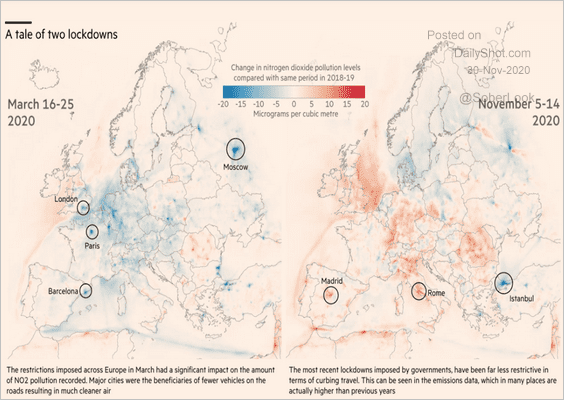

Atlantic economies are through the worst of the virus. Europe is winning:

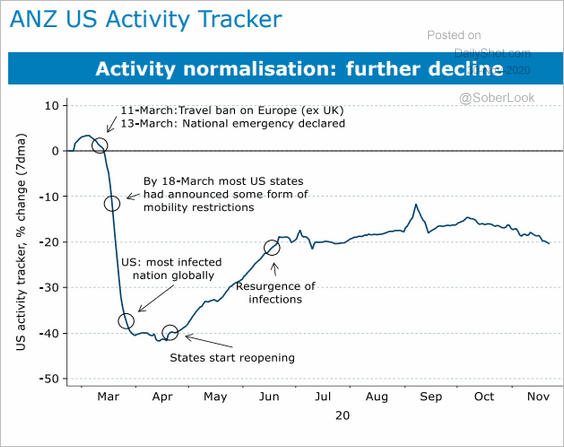

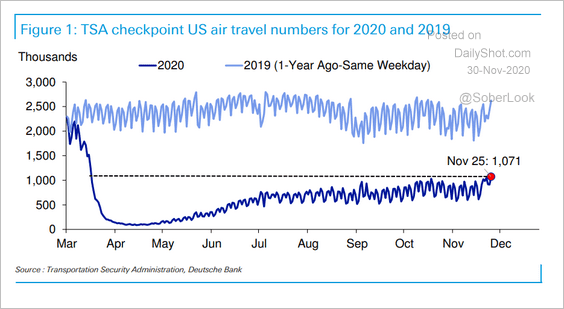

The US appears to be as well though Thanksgiving is still an asterisk:

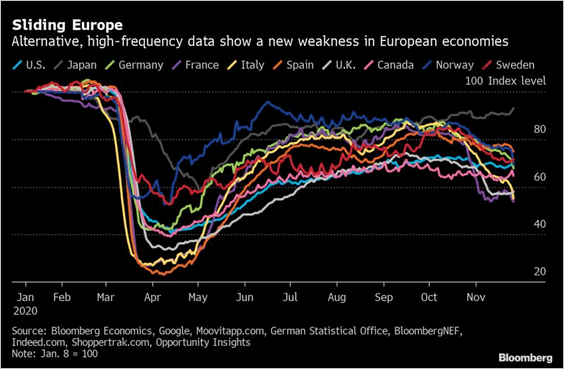

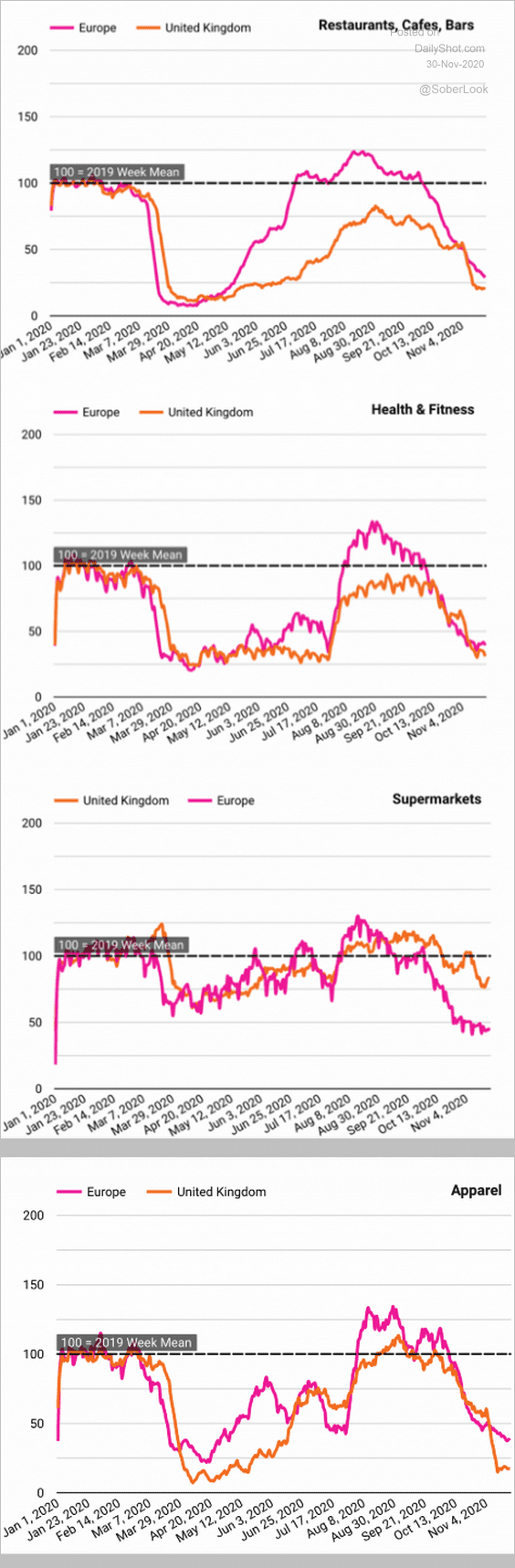

Economically, the damage is done. In Europe:

Though it is nowhere near as bad as the first lockdown, based largely around services which will rebound fast:

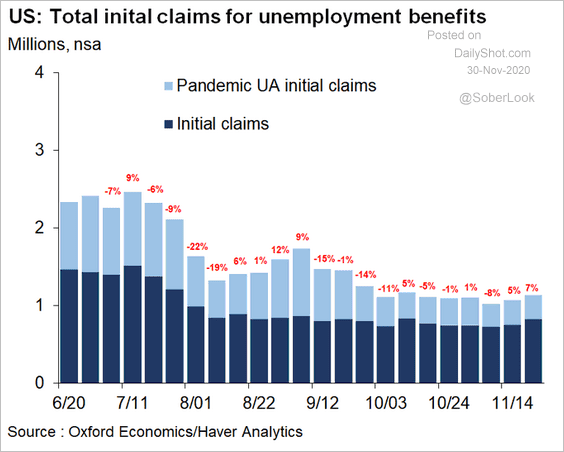

Likewise the US:

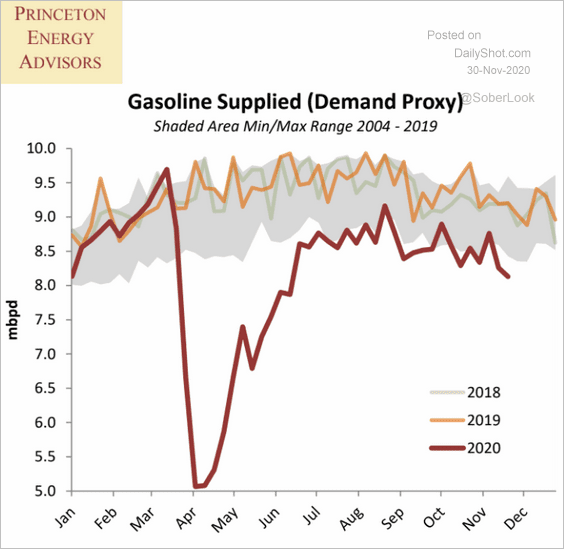

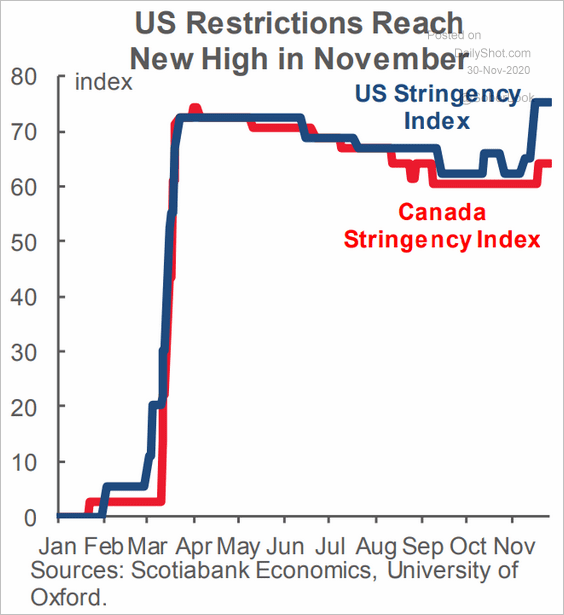

With enough lockdowns now to get it through:

With vaccines rolling out as early as next week, we are passed the worst of COVID-19 at last.

Markets are weighing the damage done versus the rebound outlook day-by-day oscillating between safe-haven bonds and tech versus cyclical value plays and curve steepening. The Australian dollar is simply a proxy for that struggle.

I expect the latter to win out in due course.